It might not seem like much, but ₹10,000 can be the cornerstone of a secure financial future. Yes, it can be possible with NPS investment and the NPS tax benefit.

The National Pension System (NPS) can offer a structured, efficient, and tax-smart way to build your retirement corpus.

So, whether you are a first-time investor or someone looking to put a small windfall to productive use, investing ₹10,000 in NPS for long-term financial security can be your long-term financial planning master-stroke.

| Click here to know more about NPS accounts and contributions. |

Power of Starting Now

Time in the market can be far more valuable than trying to time the market, hence staying invested can be an important investment strategy. Starting early can give your money more time to grow. Thus, starting NPS with ₹10000 can begin compounding returns immediately.

A one-time NPS investment strategy of ₹ 10,000 can lay a foundation for securing retirement with small investment portions. Compound interest ensures that every rupee starts earning returns, which in turn earn more returns. This snowball effect can become powerful over the years, especially if you start in your 20s or 30s.

Opening Your NPS Investment Account and Investing

Opening an NPS account is now simpler than ever, thanks to seamless digital infrastructure. As of May 15, 2025, here's how you can begin:

- Visit the official NSDL-NPS portal.

- Choose between Aadhaar-based or PAN-based registration.

- Fill in your details and upload scanned copies of KYC documents.

- Select your NPS investment strategy (Active or Auto) and nominee.

- Pay ₹10,000 as a contribution to the Tier-I account via net banking, UPI, or debit card.

Once registered, you will receive a Permanent Retirement Account Number (PRAN). Your PRAN is your unique identifier for all NPS transactions.

Choosing NPS Active vs. Auto Choice for Your ₹10,000

You can choose one of these two options for starting NPS with ₹10000:

1. Active Choice

This option can allow you to decide your own allocation across the four asset classes:

- Equity (E) – Potentially high returns; suitable for young investors.

- Corporate Bonds (C) – Moderate returns with relatively lower risk.

- Government Bonds (G) – Lower returns, but very safe.

- Alternative Investment Funds (A) – Higher risk, less liquidity.

If you are in your 20s or 30s and can take some risk for better returns, you will be able to consider allocating up to 75% in Equity (E) to leverage long-term market growth.

2. Auto Choice

This Lifecycle Fund would automatically adjust your asset allocation based on your age. It starts with a higher equity allocation and gradually becomes more conservative as you approach retirement.

It can be better if you prefer a well-balanced, age-appropriate approach to NPS investment.

You can consider factors like your risk appetite for choosing between the two NPS investments.

How ₹10,000 Can Grow Over Decades

Here’s how starting NPS with ₹10,000 today can shape your future.

Let us consider that:

- You’re 25 years old.

- You invest ₹10,000 in NPS Tier-I.

- An average annual return of 9% (possible with higher equity allocation).

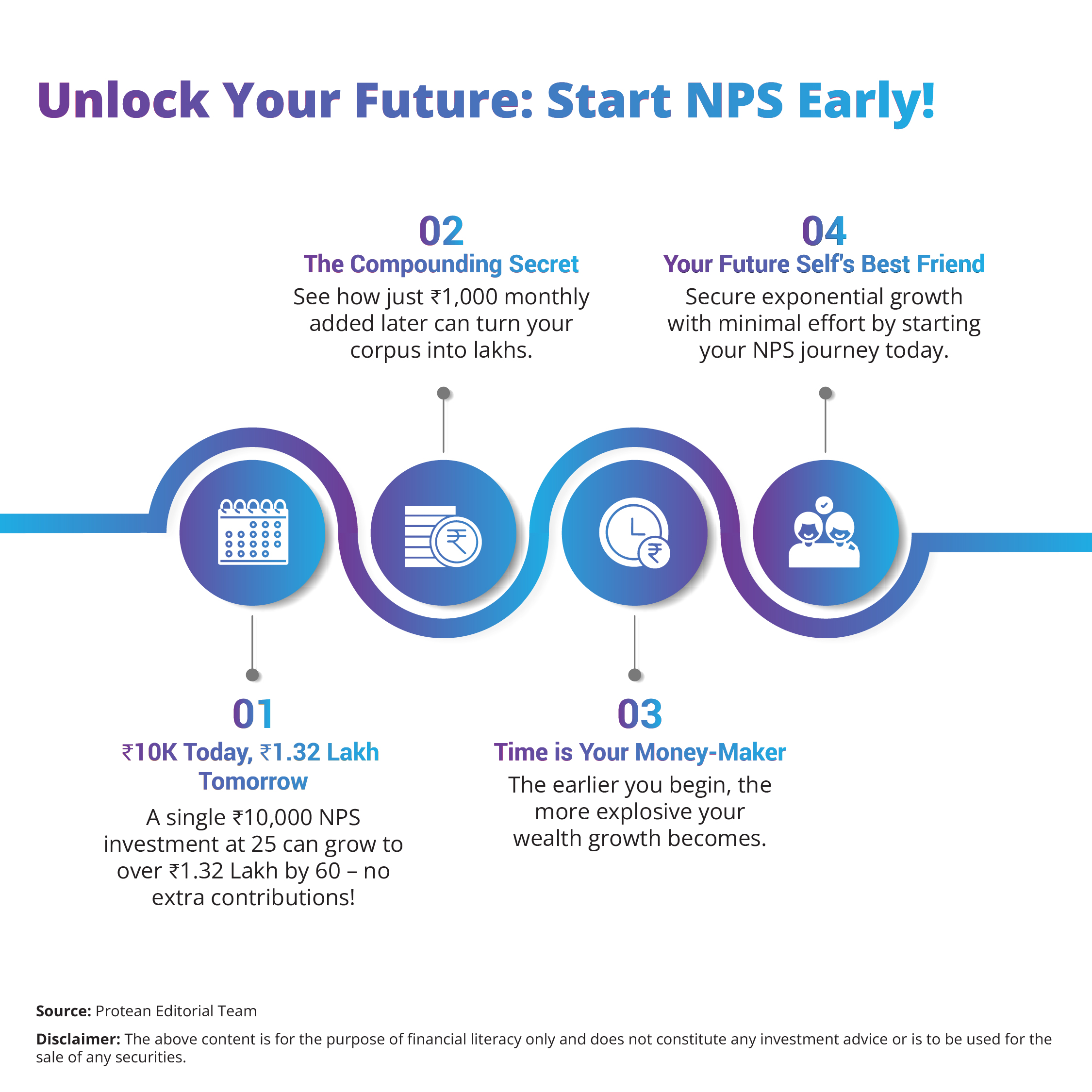

By the time you turn 60, your ₹10,000 would grow to over ₹1,32,000, without any additional contributions.

Now imagine if you add just ₹1,000 monthly from the next year. Your retirement corpus can balloon to several lakhs. This is the power of compounding, where time does most of the work. The earlier you begin, the more exponential the growth.

| For better understanding, you can use the NPS Calculator. |

Enhancing Your ₹10,000 Investment

One of the most compelling NPS investment benefits is its Tier-I NPS tax benefits (under old tax regime):

- Under Section 80C, contributions up to ₹1.5 lakh are deductible.

- An additional ₹50,000 deduction is available exclusively under Section 80CCD(1B) for NPS.

This means your ₹10,000 investment could reduce your taxable income, helping you save more. For someone in the 30% tax bracket, that’s an immediate tax saving of up to ₹3,000 – effectively reducing your investment cost to ₹7,000 while still compounding the full ₹10,000 for retirement.

₹10,000 as a Stepping Stone

You can think of ₹10,000 as a gateway investment that demonstrates the value of planning early. As your income grows, consider setting up monthly contributions, or topping up your NPS investment each year.

The best way to invest ₹10,000 in NPS is to treat it not as a one-off, but as a first chapter in a long-term commitment to financial independence.

| Moreover, NPS Vatsalya is another beneficial product of the NPS suitable for securing your child’s future and saving your tax. |

Conclusion: Secure Your Future, One Step at a Time – Starting with ₹10,000 in NPS

You do not need lakhs to begin your retirement journey. With just ₹10,000, you can start building a nest egg through the National Pension System, unlocking NPS tax benefits, long-term growth, and financial peace of mind.

Make the move today. Empower your future self by investing wisely now.

Take the First Step Now:

· Open Your NPS Account: https://npstrust.org.in/

· Learn More about NPS Features