NPS Vatsalya: Have you heard about this scheme for your child’s retirement planning?

Let us find out about it in detail.

In a significant move towards strengthening long-term financial planning for the youth, the Union Budget 2024 introduced NPS Vatsalya.

The NPS Vatsalya scheme is a unique retirement-cum-investment scheme designed specifically for minors. NPS Vatsalya merges the strengths of the National Pension System (NPS) with the growing demand for early-stage investment instruments.

With India's growing emphasis on financial inclusion and intergenerational wealth planning, this scheme can serve as a foundational pillar for parents. It can be particularly beneficial for parents who are aiming to build a secure future for their children through consistent, tax-efficient savings.

Here is all you need to know about:

- NPS Vatsalya scheme features

- NPS Vatsalya benefits

- NPS Vatsalya scheme eligibility and more.

What is NPS Vatsalya?

The NPS Vatsalya scheme is a pension scheme under the National Pension System.

Here are the main points of the NPS Vatsalya scheme:

- This scheme is designed specifically for minors.

- It can allow parents or legal guardians to open and manage a contributory account on behalf of children below 18 years of age.

- It can encourage early financial discipline and long-term corpus building.

- NPS Vatsalya is regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

- The scheme can offer market-linked returns through investments in equity, corporate debt, and government securities.

- This scheme is managed by registered pension fund managers.

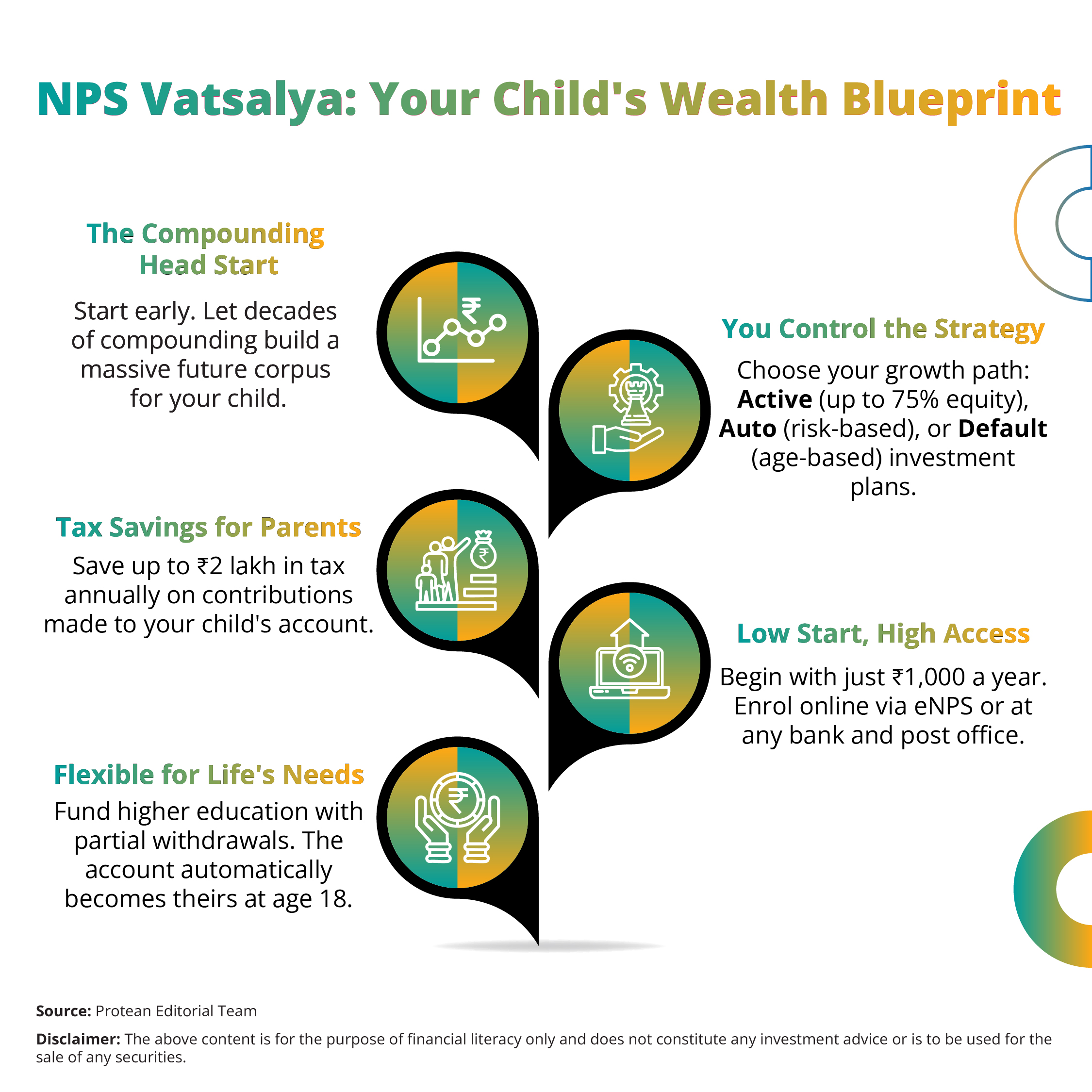

Once the child turns 18, the NPS Vatsalya account is seamlessly converted into a standard NPS Tier-I account, allowing the individual to independently manage their retirement savings.

NPS Vatsalya Scheme Eligibility: Who is Eligible for NPS Vatsalya?

The eligibility criteria for the NPS Vatsalya scheme are clearly outlined to promote inclusivity while ensuring strict compliance with Know Your Customer (KYC) norms. The scheme is available to Indian citizens, Non-Resident Indians (NRIs), and Overseas Citizens of India (OCIs) who are below 18 years of age at the time of account opening.

The account needs to be opened and managed by a parent or legal guardian on behalf of the minor, with full adherence to KYC requirements. These can include the submission of PAN or Aadhaar, proof of relationship, and age proof of the child.

Additionally, nomination is mandatory, with the minor as the primary beneficiary and the guardian serving as the initial account operator until the child reaches adulthood. Each account is uniquely linked to a Permanent Retirement Account Number (PRAN) issued in the minor’s name, which remains valid for life. This can facilitate a smooth transition to full ownership once the child turns 18.

To enhance accessibility, the Pension Fund Regulatory and Development Authority (PFRDA) has enabled account opening through various Points of Presence (PoPs) such as banks, India Post offices, and digital platforms, making it easier for parents to enroll their children in the scheme.

| Learn more about NPS Vatsalya eligibility here. |

Main Features and NPS Vatsalya Benefits

NPS Vatsalya can offer a compelling package of features that can combine investment flexibility with long-term wealth generation. Let us look at the major NPS Vatsalya features:

- Minimum Annual Contribution: The scheme has a compulsory minimum annual contribution of ₹1,000. Thus it can be affordable for most households. Also, there is no upper limit on contributions. This can encourage higher investments based on the financial capacity of the parents or guardians.

- Investment Options: NPS Vatsalya has three investment modes to offer.

These NPS Vatsalya investment modes are as follows:

- Default Scheme: Age-based asset allocation with auto-declining equity exposure.

- Auto Choice: Automated lifecycle fund management based on risk profile.

- Active Choice: Allows the guardian to choose allocation between equity (max 75%), corporate bonds, and government securities.

- PRAN Issued in Minor’s Name: The child is allotted a Permanent Retirement Account Number (PRAN), ensuring individual ownership from inception.

- Account Transition at Age 18: On attaining majority, the NPS Vatsalya account is converted into a regular Tier-I NPS account, allowing the now-adult to take over contributions and investment decisions.

- Flexible Contributions: Contributions can be made monthly, quarterly, or annually, offering flexibility to suit cash flows of families.

- Accessibility: Account opening and contributions are facilitated through Protein eGov (through its official eNPS website), banks, designated NBFCs and India Post. Thus the NPS Vatsalya investment has become widely accessible.

- Portability and Online Monitoring: Subscribers can monitor investments and switch fund managers online through the CRA (Central Recordkeeping Agency) system.

These features together make NPS Vatsalya a strong early-stage financial product with long-term benefits.

Furthermore, there are numerous NPS Vatsalya benefits that can enhance the financial well-being of the next generation in your family. Let us look at them in detail:

- Early Start for Retirement Corpus: The NPS Vatsalya scheme can leverage the power of compounding over 30 to 40 years, potentially resulting in a substantial retirement corpus. They can do this by beginning investments during childhood.

- NPS Vatsalya Tax Benefits: Contributions to NPS Vatsalya qualify for tax deductions under Section 80C (up to ₹1.5 lakh) and an additional ₹50,000 under Section 80CCD(1B). These deductions are available to the contributing parent or guardian.

- Partial Withdrawals: After three years of account opening, partial withdrawals of up to 25% of contributions are allowed for critical needs such as education, serious illness, disability, or higher studies of the minor.

- Security in Event of Death: In case of the guardian’s death, the alternate guardian can take over. If the minor passes away, the accumulated corpus is paid to the legal heir or nominee.

The NPS Vatsalya scheme has thus combined the features of:

- Flexibility

- Security

- Tax efficiency

These features can make NPS Vatsalya a powerful tool for future-focused financial planning.

How to Open an NPS Vatsalya Account

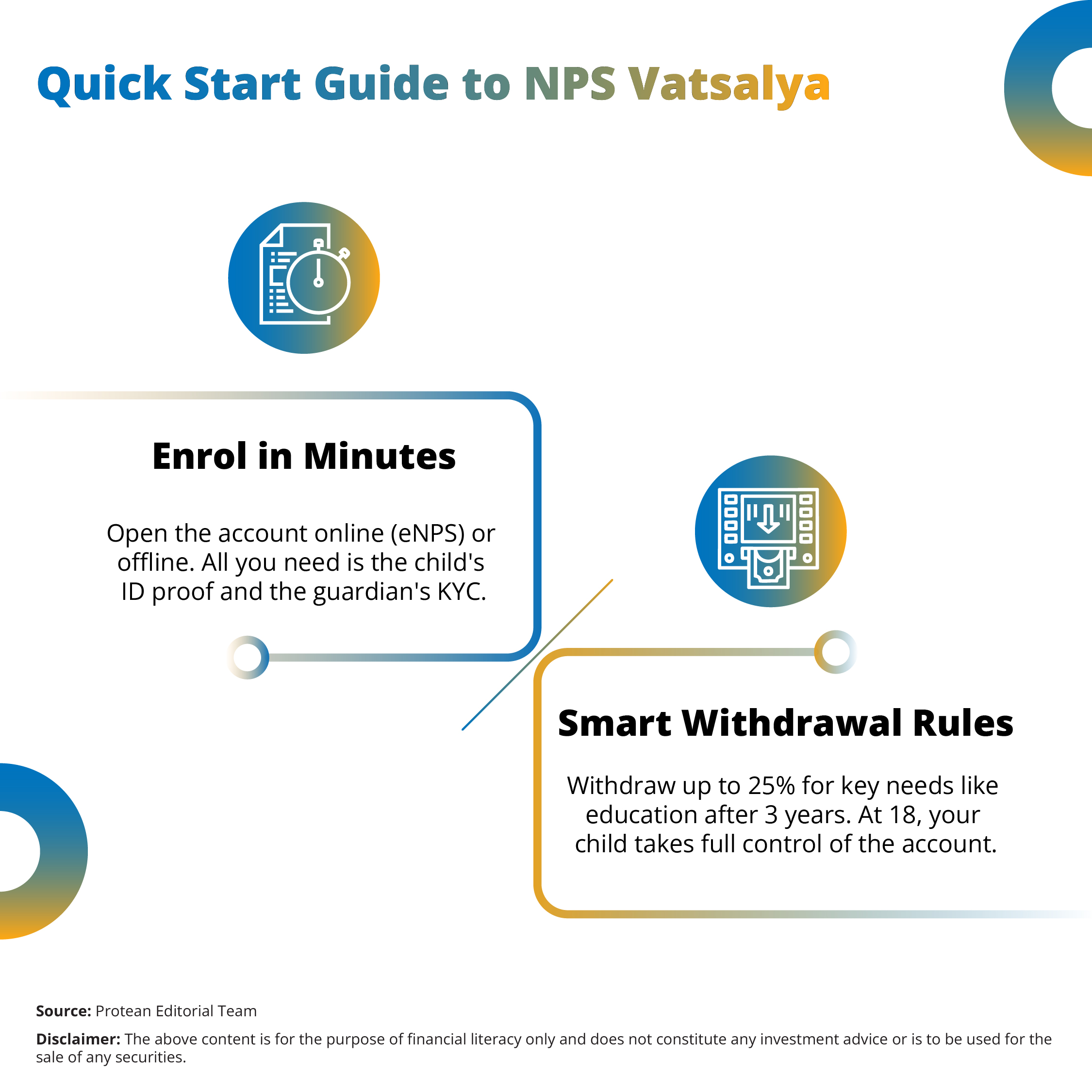

Opening an NPS Vatsalya account is a simple process, whether online or offline.

Online Process via eNPS:

- Visit https://enps.nsdl.com. Or click here.

- Select the NPS Vatsalya option under “Registration.”

- Enter details of the minor and guardian.

- Upload KYC documents: Aadhaar/PAN, birth certificate etc., and proof of relationship (Proof of relationship is only needed, if the guardian is not the natural parent but a legal guardian).

- Choose the investment option and Pension Fund Manager (PFM).

- Make the initial contribution (minimum ₹1,000).

- Submit the e-signature or OTP-based Aadhaar authentication.

Offline Process via Point of Presence (PoP):

- Visit a registered bank branch, India Post outlet, or PoP service provider.

- Fill out the NPS Vatsalya application form.

- Attach photocopies of the required KYC documents.

- Submit the form along with the initial contribution amount.

Once verified, a PRAN card is issued in the child’s name. This PRAN would remain constant and facilitate investment tracking. At age 18, the child undergoes a KYC refresh and takes control of the account, making it a fully self-managed NPS account.

Learn about how NPS Vatsalya compares with other investment products like mutual funds and PPF here.

NPS Vatsalya Withdrawal and Exit Rules

NPS Vatsalya maintains a structured withdrawal and exit framework similar to the traditional NPS scheme but with certain minor-specific provisions. These are as follows:

Partial Withdrawal

After three years from the date of account opening, up to 25% of the contributions (excluding returns) can be withdrawn. The purpose must fall within approved categories: education, severe illness, disability-related expenses, or marriage (in special cases).

Exit at Age 18

Upon turning 18, the account holder is given the choice to:

- Continue the investment as a regular NPS Tier-I subscriber.

- Or exit the scheme if desired. Exiting before the age of 60 will require at least 80% of the corpus to be annuitized, while the rest can be withdrawn as a lump sum.

Death of Subscriber or Guardian

- If the minor dies, the account is closed, and the accumulated corpus is paid to the guardian or legal heir.

- In the event of the guardian’s demise, an alternate guardian can be appointed after necessary documentation.

These NPS Vatsalya exit and withdrawal rules can ensure that the corpus is preserved for the intended long-term use while offering flexibility in times of need.

Conclusion

NPS Vatsalya is a forward-looking scheme designed to promote structured financial planning for minors.

It can empower the parents to build a secure future for their children through:

- Systematic and flexible investments

- Tax benefits

- Long-term compounding

The NPS Vatsalya scheme is open to Indian citizens, NRIs, and OCIs under 18, the scheme is accessible, affordable, and aligns with goals like retirement or higher education. With guardian-managed accounts and full digital access, it can offer a practical tool for early financial discipline.

As India strengthens its savings culture, NPS Vatsalya can emerge as a valuable option for parents aiming to ensure long-term financial independence for their children. Start your contribution towards your child’s financial security with NPS Vatsalya now!

Frequently Asked Questions

Q1: What is the minimum contribution required for NPS Vatsalya?

In NPS Vatsalya, a minimum of ₹1,000 per year is required. There is no upper limit.

Q2: Can NRIs invest in NPS Vatsalya?

Yes, NRIs and OCIs under 18 years are eligible to invest in the NPS Vatsalya scheme.

Q3: Are there any tax benefits for investing in NPS Vatsalya?

Yes, there are NPS Vatsalya tax benefits available to parents. The parents can claim tax deductions under Section 80C and 80CCD(1B) on their contributions.

Q4: What happens to the NPS Vatsalya account after the child turns 18?

The NPS Vatsalya account is converted into a regular NPS Tier-I account in the child's name.

Q5: Is partial withdrawal allowed before the child turns 18?

Yes, NPS Vatsalya partial withdrawal is allowed after 3 years. A partial withdrawal of up to 25% of contributions is permitted for specified needs like education or health.

Q6: How is the investment managed?

The NPS Vatsalya funds are managed by PFRDA-registered pension fund managers with options for equity and debt exposure.