Is the Multiple Scheme Framework (MSF) an evolution of the National Pension System (NPS)?

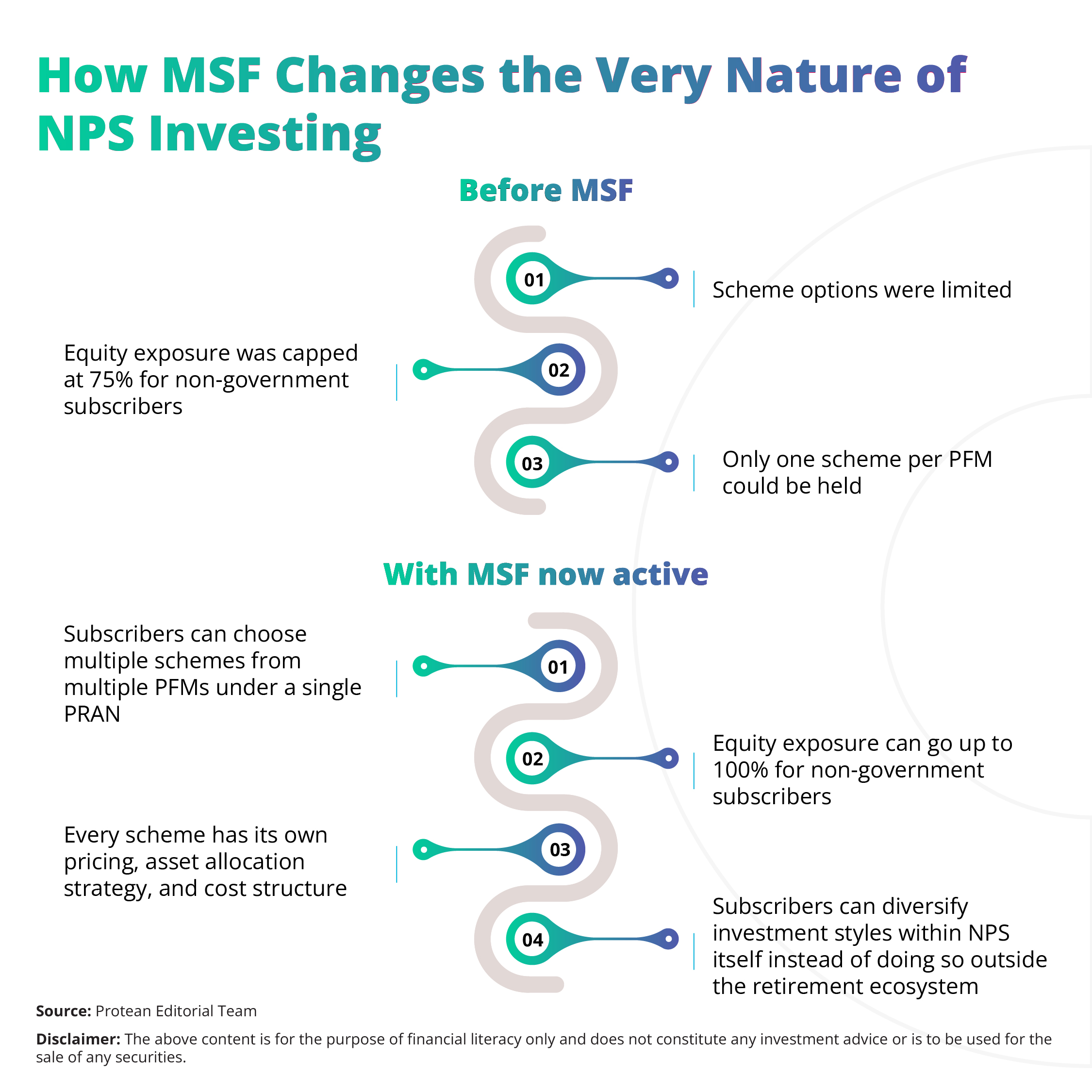

Yes, the NPS scheme has evolved over the years. Its most recent leap has absolutely been the introduction of the MSF. Earlier, subscribers could invest in a limited and predefined set of schemes with equity investment caps.

The MSF has offered a broader choice to the subscribers. It has also added greater control, and sharper strategic flexibility in NPS investing. MSF is a game-changing upgrade for subscribers who understand NPS and want more personalised wealth-building opportunities.

With MSF, NPS now offers scheme diversification, Pension Fund Manager (PFM) flexibility, and allocation preferences adaptable to every risk appetite.

The Identity and Structure: PRAN and Account Tiers

To understand how MSF integrates into the NPS structure, it is important to revisit the core elements:

1. Permanent Retirement Account Number (PRAN)

Every subscriber is issued a PRAN, which functions as the universal identity across employer changes, PFMs, schemes, and contribution history. All investment and retirement decisions under NPS, whether under older schemes or MSF, are tracked under the same PRAN. This consistency makes NPS portable, transparent, and easy to maintain across working years.

2. Two Tiers of NPS architecture

Tier-I is the primary retirement account. It requires mandatory contributions for those enrolled through an employer and is designed for long-term accumulation. It carries withdrawal restrictions and retirement-linked tax benefits.

Tier-II, on the other hand is an optional, open-ended investment account with no withdrawal restrictions. It works more like a low-cost, flexible investment wallet but without contribution tax incentives.

Subscribers can hold multiple schemes simultaneously with MSF under a single PRAN. These schemes can come from one or multiple PFMs, providing diversification even within NPS.

This structure keeps things flexible. Meaning, subscribers who prefer a simple setup can continue easily, while those who want more control and customisation also have that option.

Investment Philosophy: Choice and Allocation Models

Traditionally, the investment philosophy of NPS has revolved around choosing a PFM and selecting an asset allocation across four asset classes.

- Equity (E)

- Corporate debt (C)

- Government securities (G)

- Alternative investment funds (A)

Even with that structure, the room for customisation was limited because investment options were few and equity caps were fixed.

Under MSF, this philosophy has been reimagined. Now, subscribers can make decisions across these three independent dimensions:

1. Choice of PFM

Investors are no longer restricted to one PFM across all investments. Investors may:

- Use one PFM for aggressive allocations

- Use another for conservative or debt-heavy schemes

- Distribute contributions across several PFMs to reduce dependence on one investment style

2. Choice of Scheme

Each PFM offers a list of MSF schemes, each with a clear investment mandate. Investors may choose schemes that differ in:

- Equity allocation level (up to 100% for non-government subscribers)

- Risk tolerance (high, moderate, or conservative structures)

- Market philosophy (large-cap bias, diversified, or blended equity approaches)

3. Choice of Allocation Model

Investors can decide how their contributions are distributed across selected schemes. Two models exist:

- Active Choice — where you allocate contributions manually to the asset classes or MSF schemes of your preference.

- Auto Choice (Life Cycle Funds) — where allocation adjusts automatically with age, reducing risk exposure as retirement approaches.

For advanced investors, the MSF design allows strategic allocation across schemes and PFMs, such as:

- Using a high-risk 100% equity scheme in the early career phase

- Allocating to corporate debt or government securities as retirement nears

- Continuously blending styles to minimise market risk from any one PFM or investment strategy

This multilayered investment philosophy brings NPS closer to portfolio-management systems used in professional wealth advisory.

For subscribers who previously felt that NPS lacked modern investment agility, MSF eliminates that limitation. It gives freedom without compromising on transparency, governance, and cost control.

MSF Maturity and Using of Accumulated Assets

At maturity, normally at the age of 60 years, NPS balances accumulate into the retirement corpus. The MSF flexibility influences this corpus during accumulation but does not change the core decumulation rules, which remain:

- Up to 60% of the maturity corpus can be withdrawn as a lump sum and remains tax-free under current rules.

- The remaining minimum 40% must be used to purchase an annuity, ensuring retirement income continuity.

- Partial withdrawals from Tier-I are allowed only in specific cases such as higher education, illness, and home purchase.

- Tier-II funds can be withdrawn anytime.

Subscribers approaching retirement can use MSF strategically in the final decade, gradually raising exposure to debt or balanced schemes to preserve gains while retaining growth potential. MSF does not only help in wealth creation. Finally, it supports wealth preservation through planned risk reduction as retirement approaches.

Conclusion

NPS was once viewed as a conservative savings plan. Today, because of the Multiple Scheme Framework, it is equally a retirement investment engine.

Subscribers control their PFMs, choose their schemes, decide their allocation models, and diversify not only across asset classes but across investment philosophies. This flexibility does not sacrifice affordability, NPS remains one of the lowest-cost investment products in India.

So, for individuals who want control, transparency, and long-term growth potential under a disciplined retirement structure, MSF makes NPS a powerful, future-ready solution. The more thoughtfully subscribers use this flexibility, the more meaningful the retirement outcomes become.

Frequently Asked Questions (FAQs)

Q1: Is MSF available to all NPS subscribers?

Yes, all subscribers can use MSF, but the 100% equity allocation is available only to non-government subscribers.

Q2: Can I hold multiple PFMs at the same time under MSF?

Yes, you can allocate contributions to schemes from different PFMs simultaneously under the same PRAN.

Q3: Are existing NPS balances automatically shifted to MSF schemes?

No, MSF applies only to new contributions; earlier balances remain in the previous scheme unless switched manually.

Q4: Do MSF schemes have higher fees?

MSF fund management charges are slightly higher than the earlier common scheme structure, though NPS continues to be low cost overall.

Q5: Does MSF reduce risk for investors?

It does not reduce market risk directly, but it provides tools like multiple schemes and PFMs. This can allow subscribers to manage risk more intelligently.

Q6: Can MSF help build a larger corpus compared to older NPS rules?

Potentially yes, especially for long-term investors using higher equity allocations thoughtfully and consistently.