Let us imagine a young professional, Rohit, who joined the workforce five years ago. He opened his National Pension System (NPS) account, dutifully contributed every month, and let his retirement savings grow steadily. But recently, he heard about the newly launched Multiple Scheme Framework (MSF) under NPS, completely transforming how he could design his retirement portfolio.

Far from simply parking all his savings in one scheme, MSF gives him the flexibility to allocate across multiple schemes and go beyond the one-size-fits-all model.

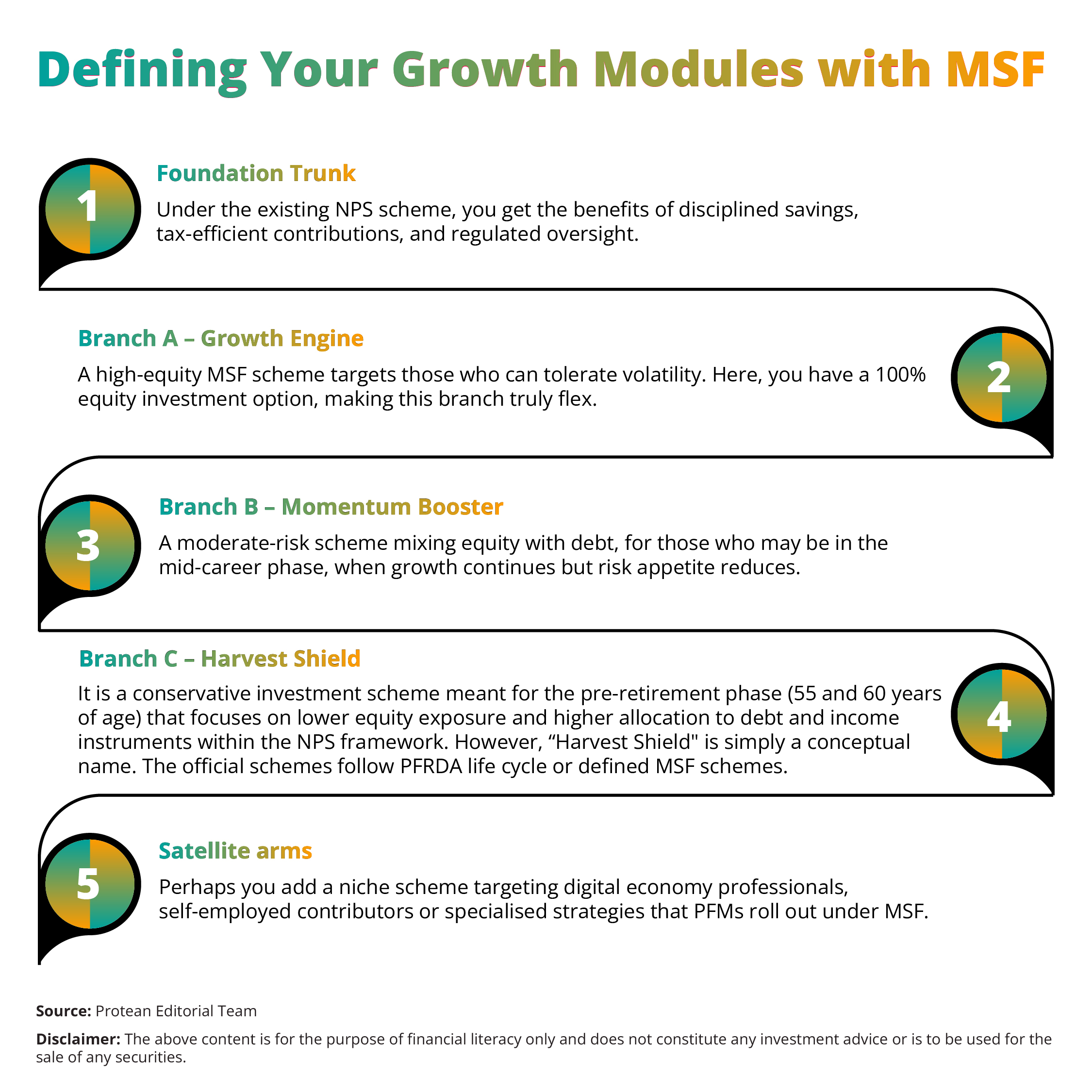

Here is how you may select multiple Pension Fund Managers (PFMs) under MSF, and structure a smart, diversified NPS portfolio like Rohit.

How MSF Redefines Your NPS Scheme

Traditionally, under NPS in the private/non-government sector, a subscriber was limited to one scheme in each Tier under one PFM, but with the introduction of MSF, the landscape has shifted.

Under MSF, you can do the following:

- Use a single Permanent Retirement Account Number (PRAN) as a unified identifier across Central Record-keeping Agencies (CRAs) such as Protean eGov Technologies Ltd.

- Hold multiple schemes under one PRAN, either across different PFMs or within the same PFM, depending on the scheme design.

- Benefit from customised scheme options designed for various investor segments, including corporate employees, self-employed individuals, and gig-economy workers.

- Access up to 100% equity allocation in select high-risk variants, offering enhanced growth potential.

- Enjoy a low-cost structure, with charges capped at 0.30% of assets under management (AUM) annually, along with incentives for PFMs managing larger subscriber bases.

Evaluating the Pension Fund Managers

Now that MSF lets you pick across PFMs and schemes, how do you decide which Pension Fund Manager(s) to include? Here’s a checklist that Rohit uses and you can adapt:

Track record and scheme lineage

Although MSF introduces new schemes, look at how the PFM has performed in the legacy “common schemes” under NPS.

Scheme design under MSF

Check what kinds of schemes the PFM is launching:

- Does it offer a “high-risk” variant (up to 100% equity) as well as a “moderate-risk” version?

- What asset-class tilts are there?

- Are there schemes tailored to your stage (young professional vs near-retirement)?

- How clearly are schemes described?

Under MSF the PFRDA expects each scheme to carry a “scheme essentials” document and risk-o-meter disclosure.

Fee structure and incentives

Although the cap is 0.30% for MSF schemes, some PFMs may offer lower fees. Also examine whether there are any additional charges for switching between schemes and review the incentive structures of the PFMs, as these may influence service quality and performance.

Operational readiness & service

Since MSF is new (from Oct 1 2025) and requires CRA/PoP/Fund system upgrades, pick PFMs that demonstrate solid operational capabilities, good customer service and flexibility for switches or contributions.

Compatibility with your personal goals

Rohit evaluated whether to pursue aggressive growth or maintain a balanced mix of debt and equity. Likewise, investors should choose PFMs whose schemes match their risk profile and investment goal.

Portfolio-mix across PFMs

It may be wise to select multiple PFMs, combining high-equity and conservative schemes to balance risk. The MSF framework enables such diversification across managers and investment styles.

The Practical Allocation: From Theory to PRAN

Following are the steps Rohit follows from decision to implementation under the MSF framework:

Review existing NPS holdings

Rohit already holds a standard NPS common scheme under PFM X. Under MSF, he can continue contributing to this scheme or allocate future contributions to newly introduced MSF schemes. Switching from existing schemes is subject to PFRDA guidelines, and subscribers are advised to review them carefully.

Select PFMs and schemes

Rohit evaluates the scheme documents of PFM A and PFM B.

- PFM A’s High Growth Equity (MSF) scheme allows up to 100% equity exposure, suitable for his long investment horizon.

- PFM B’s Moderate Balanced (MSF) scheme combines equity, corporate bonds, and government securities for greater stability.

He allocates 60% of his fresh contributions to PFM A, 30% to PFM B, and retains 10% in his existing common scheme for continuity.

Update instructions with CRA/PoP

Using his PRAN, Rohit logs into his CRA portal (or approaches his PoP) to specify the allocation, 60% to PFM A, 30% to PFM B, and 10% to his existing scheme. Since MSF enables multiple schemes under one PRAN, this allocation is seamlessly executed through the CRA’s upgraded system.

Onboard new schemes and contribution flow

Effective 1 October 2025, contributions under MSF are directed by PFRDA to the selected schemes in the chosen proportions. MSF operates within the NPS framework, ensuring continued eligibility for tax benefits under Section 80CCD while providing greater flexibility and diversification.

Record and monitor allocations

Rohit maintains a record of his allocations, scheme start dates, benchmarks, and fee structures. This helps him track performance, maintain transparency, and review progress towards his long-term retirement goals.

Once implemented, contributions flow accordingly, and each supporting scheme appears in his NPS dashboard via CRA.

Periodic Monitoring and Rebalancing of Portfolio

Selecting your PFMs and schemes is a big step, however it’s only the beginning. For the next 10-15 years Rohit must monitor and rebalance:

Periodic review (annually or semi-annually)

Investors should periodically assess whether PFMs are performing in line with their benchmarks, verify if asset allocation remains consistent with their risk profile, and review any changes or disclosures in the fee structure under the MSF framework.

Life-stage assessment

As Rohit moves from age 30 towards 40, his risk capacity may change. He might gradually reduce high-equity exposure and increase stable schemes. MSF gives this flexibility: he can shift future contributions or even switch the scheme (within rules). Note: switching between MSF schemes is restricted until after 15 years of vesting or normal exit. However, switching to a common scheme is allowed.

Check for regulatory communications

Since MSF is new, PFMs and CRAs must comply with disclosures, risk-o-meter labels, and tabulated scheme documents. Regulators may issue updates or improvements. Staying informed ensures your portfolio stays compliant and optimal.

Rebalancing contributions vs corpus

If one scheme grows faster than others (e.g., high-equity scheme returns far exceed balanced scheme), the portfolio may tilt more heavily into equity than intended. Rebalancing may mean reducing or pausing those contributions and increasing ones into more conservative schemes. While NPS has a long-term horizon, risk control remains crucial.

Maintain the pension mindset

Even with the availability of high-equity options under MSF, investors should remember that the primary objective of NPS is to build a sustainable retirement corpus, with a portion eventually annuitised to provide regular income. Monitoring and rebalancing should therefore focus on long-term pension goals rather than short-term returns, using MSF as a strategic tool aligned with one’s retirement horizon.

Conclusion

The Multiple Scheme Framework marks a significant advancement in the NPS ecosystem, offering investors greater flexibility and control over their retirement savings. It enables subscribers to select multiple PFMs, align schemes with their risk appetite, and build a well-diversified portfolio while retaining the tax advantages and pension focus of NPS. With discipline and consistency, the MSF can serve as a powerful tool for long-term financial security.