Retirement is an inevitable financial goal! We all have to retire from stress-ful professional lives, hoping that life post-retirement would help us pursue our dreams and live with financial security.

But is this possible? Yes, the National Pension System (NPS) can be a powerful and versatile tool specifically designed to help individuals realise financial goals in their post-work years.

Let us learn more about NPS benefits and how they can help in making your post-retirement life financially worry-free.

| Click on this link to learn about NPS registration and contribution. |

Scenario 1: A Steady Stream - NPS Annuity Options in India

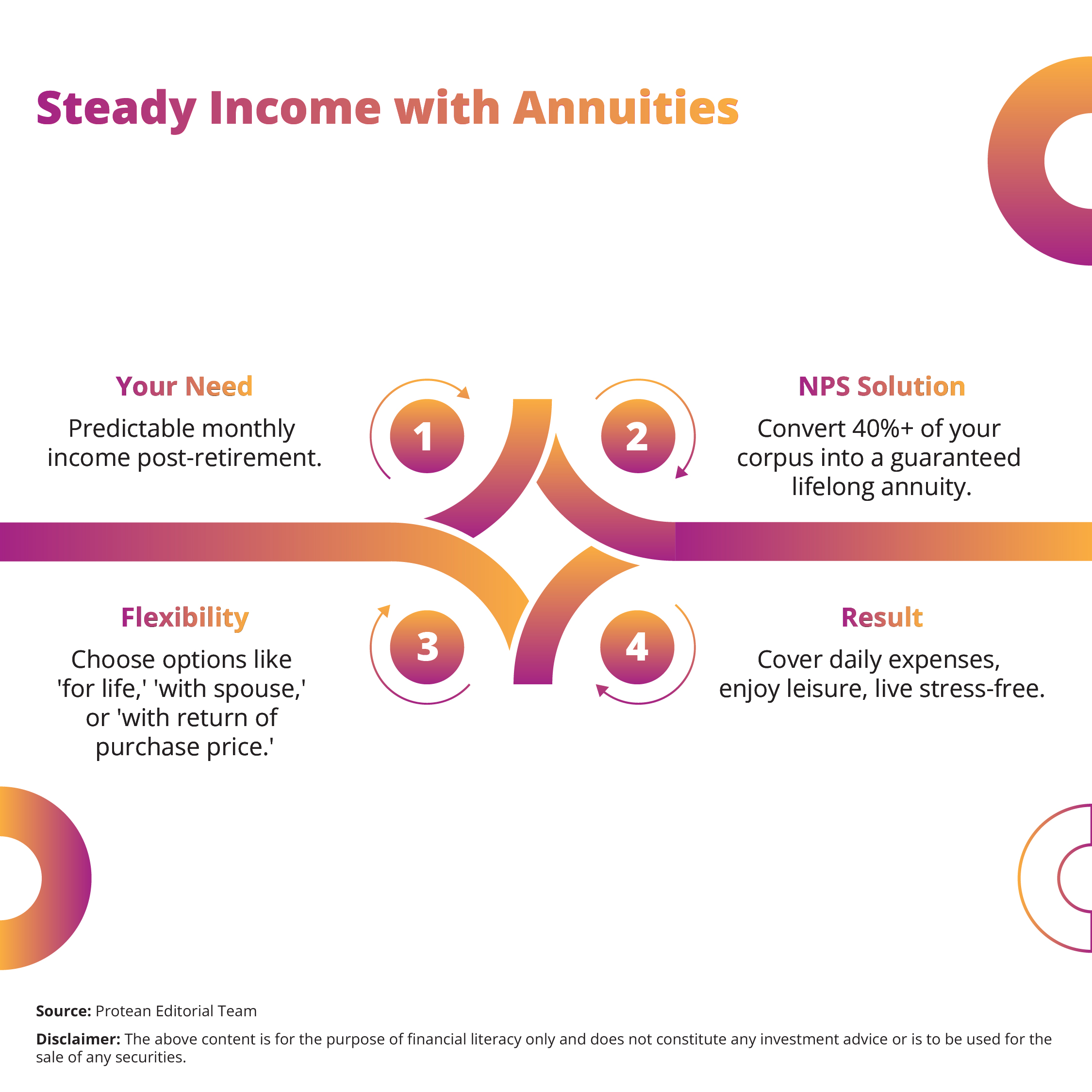

For a worry-free retirement, you need a predictable and consistent income stream. This regular inflow can allow you to cover recurring expenses, maintain your lifestyle, and enjoy your golden years without the constant stress of managing day-to-day finances.

The annuity component of your NPS investment precisely addresses this need.

Upon reaching 60 years of age (or earlier, depending on specific withdrawal rules), NPS has mandates that you use at least 40% of your accumulated corpus to purchase an annuity from a Pension Fund Regulatory and Development Authority (PFRDA) empaneled Annuity Service Provider (ASP).

This purchase would convert a portion of your lump sum into a guaranteed periodic payment for the rest of your life, or for a specified period, depending on the chosen annuity type.

There are several available NPS annuity options in India. Here are a few common ones:

- Annuity for life with return of purchase price provides regular payments throughout your lifetime, and upon your demise, the original corpus amount (purchase price) returns to your nominee, providing NPS nominee benefit.

- Annuity for life provides regular payments for your entire life, but the payments stop upon your demise, and the corpus is not returned.

- Annuity for life with 100% annuity to spouse offers regular payments throughout your lifetime. Upon your demise, your spouse receives 100% of the annuity payments for their lifetime.

- Annuity for a guaranteed period (e.g., 5, 10, 15, or 20 years) and then for life provides payments for a fixed period, regardless of whether you are alive or not. If you survive beyond the guaranteed period, payments continue for your lifetime. If you pass away within the guaranteed period, the remaining payments for that period go to your nominee.

A larger NPS investment corpus might naturally translate into a higher annuity amount. This structure can allow you to plan your monthly budget with confidence, ensuring essential expenses are covered and you can pursue leisure activities without financial strain.

| Learn more about NPS investment exit options here. |

Scenario 2: Choosing Flexibility – Partial Withdrawals

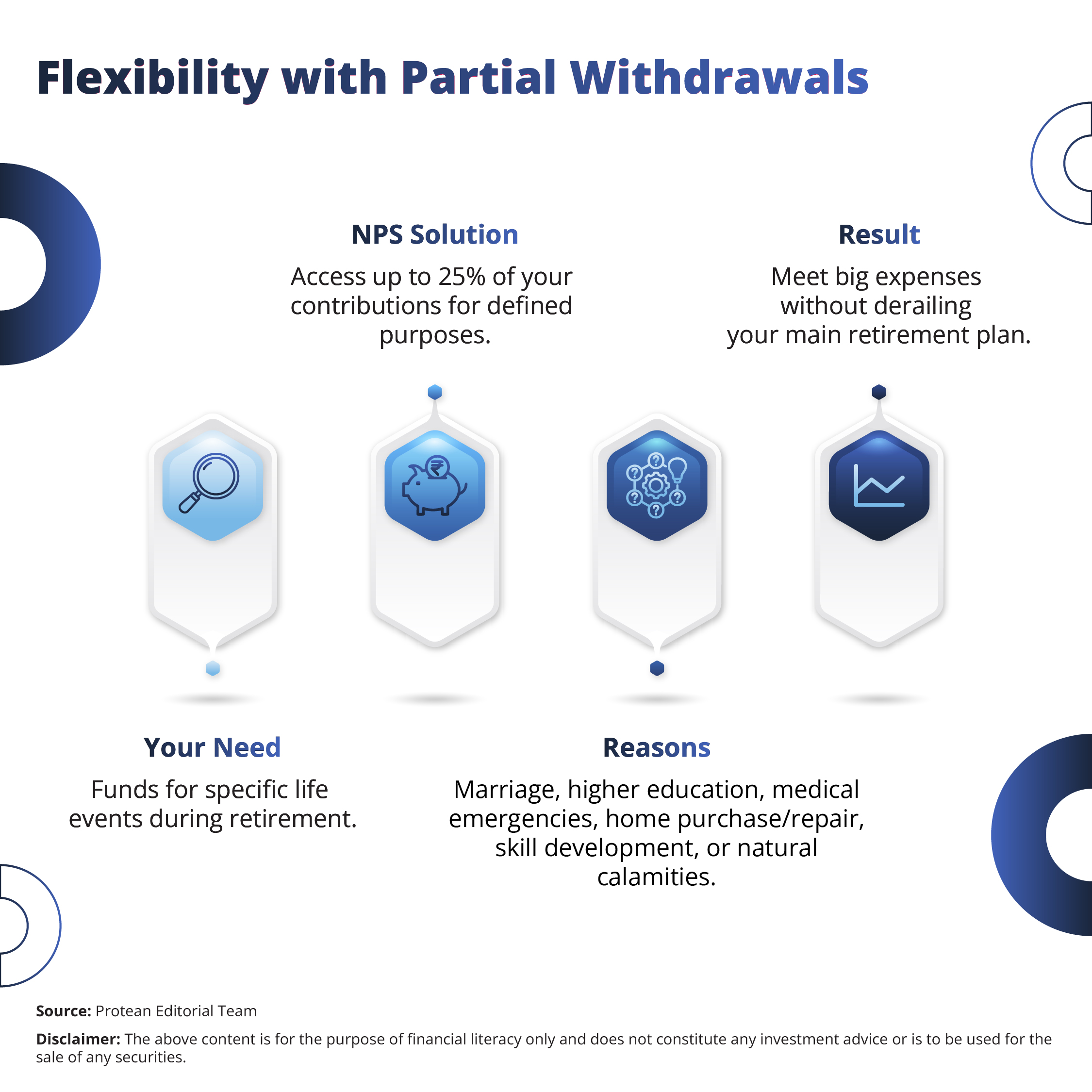

While the primary NPS benefit is a strong retirement corpus. The National Pension System structure acknowledges that certain life events might require access to funds even before full retirement or during the post-retirement phase. This is where the facility of NPS partial withdrawal becomes invaluable, offering crucial flexibility.

Under current PFRDA regulations in India, subscribers can initiate partial withdrawals from their Tier-I account for specific, pre-defined purposes. These withdrawals are strictly event-based, ensuring that the core retirement corpus remains protected while allowing access for genuine needs. You must have completed minimum years of NPS subscription to qualify for a partial withdrawal.

Permitted NPS withdrawal scenarios as of May 2025 include the following:

- Marriage: Your own wedding or for the wedding of your children (including legally adopted children).

- Higher Education: To finance your children's higher education (including legally adopted children).

- Medical Expenses: In times of critical illness, NPS withdrawals for medical treatment for yourself, your spouse, children, or dependent parents. The PFRDA has defined critical illnesses with a list for this purpose.

- Home Purchase/Repair: For the purchase or construction of your first residential property. This option applies only if you do not already own residential property (either solely or jointly). Funds can also be used for major structural renovation or repair of your own home.

- Skill Development or Self-Employment: To support career transitions and entrepreneurship. Withdrawals can fund certified skill development programs or initial business set-up costs.

- Natural Calamities: To address expenses incurred due to significant natural disasters, providing support during unforeseen emergencies.

The NPS withdrawal limit as per NPS partial withdrawal rules is up to 25% of your own contributions (excluding any employer contributions) as on the date of application. Furthermore, you can make only three such partial withdrawals during the entire tenure of your NPS Tier-I account.

Click on this link for NPS withdrawal FAQs.

Scenario 3: NPS Lump sum Withdrawal for Healthcare

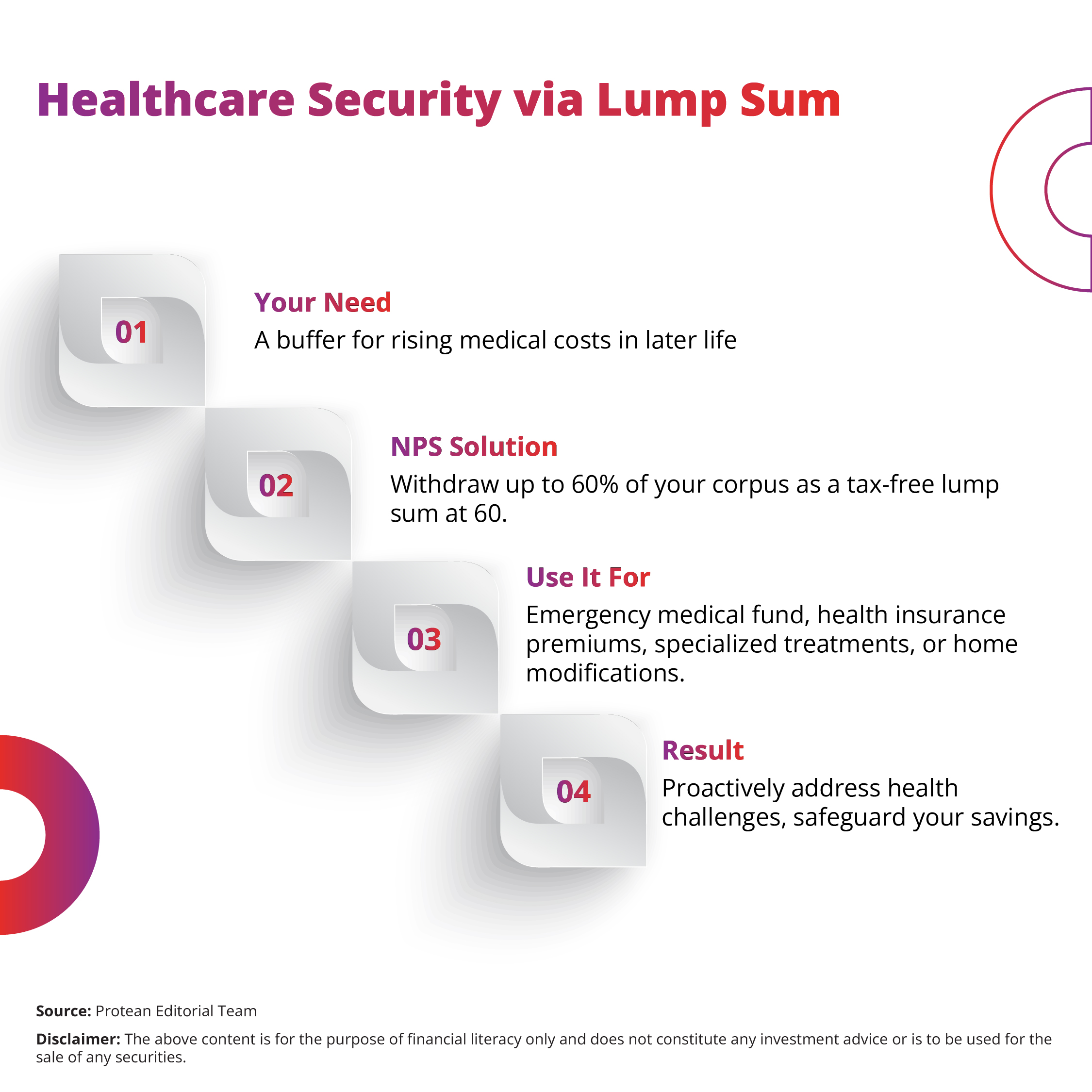

Healthcare expenses often present one of the most significant financial challenges in retirement. As individuals age, the likelihood of requiring medical attention increases, and treatment costs, especially for critical illnesses or long-term care, can be substantial. A well-planned NPS investment strategy can play a pivotal role in mitigating these concerns, ensuring that healthcare needs do not become a source of financial tension.

At the time of regular retirement (typically age 60), NPS subscribers can withdraw up to 60% of their accumulated corpus as a tax-free lump sum. This lump sum can provide a significant buffer that can be strategically allocated for various post-retirement needs, including building an emergency fund specifically for healthcare contingencies.

| Calculate your total maturity amount and NPS returns beforehand by simply navigating to the NPS Prosperity Planner. |

While NPS benefits do not have an exclusive "medical withdrawal" option for regular, ongoing expenses in retirement, the lump sum flexibility at maturity proves crucial. You can earmark a portion of this tax-free lump sum for the following reasons:

- Establishing a dedicated medical emergency fund can cover out-of-pocket expenses, deductibles, or treatments not fully covered by health insurance.

- Purchasing comprehensive health insurance can help you use the lump sum to pay premiums for robust health insurance policies that provide extensive coverage in later years.

- Funding specialised treatments for specific critical illness arising after retirement, and your insurance coverage is insufficient, a portion of your lump sum can bridge the gap.

- Home modifications funds can be used for necessary home modifications to accommodate age-related mobility issues or health conditions, enhancing comfort and safety.

Furthermore, as discussed in the partial withdrawal scenario, current NPS benefits do permit partial withdrawals for critical illnesses even before full retirement, providing an important safety net. While this applies to pre-retirement, the presence of such a provision underscores NPS's recognition of unforeseen medical needs. The ability to access a substantial tax-free lump sum at retirement specifically for healthcare planning provides immense peace of mind. It ensures that a major unpredictable expense area in retirement is proactively addressed, safeguarding your savings and allowing for a more truly tension-free retirement.

| Already started your NPS registration process? Complete pending registration by clicking on this link. |

Scenario 4: NPS Nominee Benefits

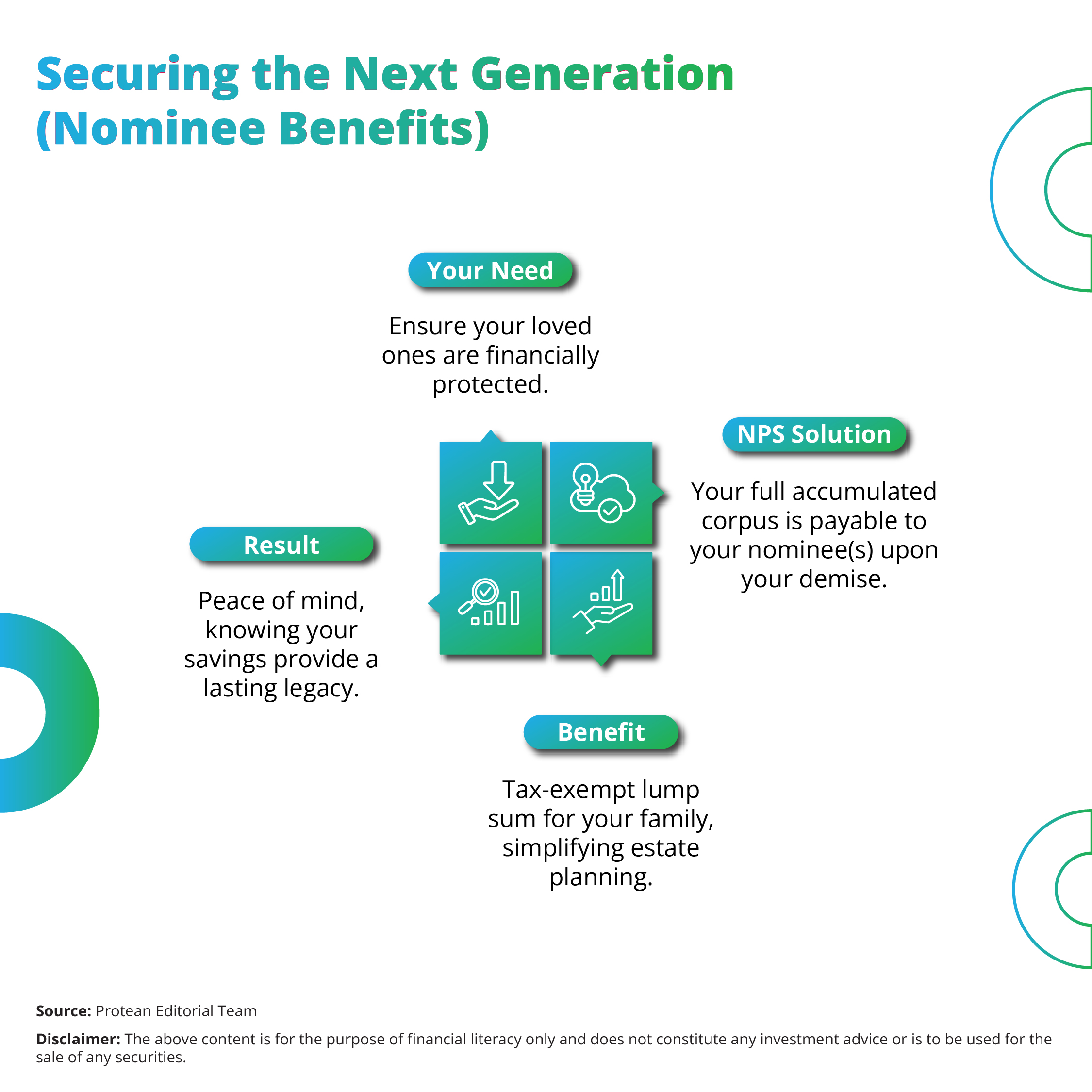

A comprehensive retirement plan can extend beyond your own financial security. It can also consider the well-being of your loved ones. The National Pension System can provide clear provisions for nominees. This can ensure that the accumulated NPS investment corpus is handled seamlessly upon the demise of the subscriber, offering crucial financial security to the next generation.

Upon the unfortunate demise of an NPS subscriber, the entire accumulated corpus is payable to the nominee(s) or legal heir(s) registered with the NPS account. Thus, your diligent savings efforts translate into a tangible benefit for your family during a difficult time with this payout. The nominee can typically withdraw the entire accumulated corpus as a lump sum. This lump sum is generally tax-exempt in the hands of the nominee.

For claiming NPS benefits, the nominee has to submit a withdrawal request to the associated Point of Presence (POP) or directly to the Central Recordkeeping Agency (CRA). The need to send this along with necessary documents such as the subscriber's death certificate, KYC documents of the nominee, and other prescribed forms.

Having the NPS investment automatically designated for your nominee(s) can simplify estate planning compared to other assets that might require probate or lengthy legal processes. This can ensure quick access to funds for your loved ones, allowing them to manage immediate financial needs and future planning without unnecessary complications. This aspect of NPS can provide immense peace of mind, knowing that your long-term savings will effectively support your family even in your absence. It plays a solidifying role in securing not just your future, but also the financial stability of those you cherish.

| Check this link for more information on the NPS nomination facility. |

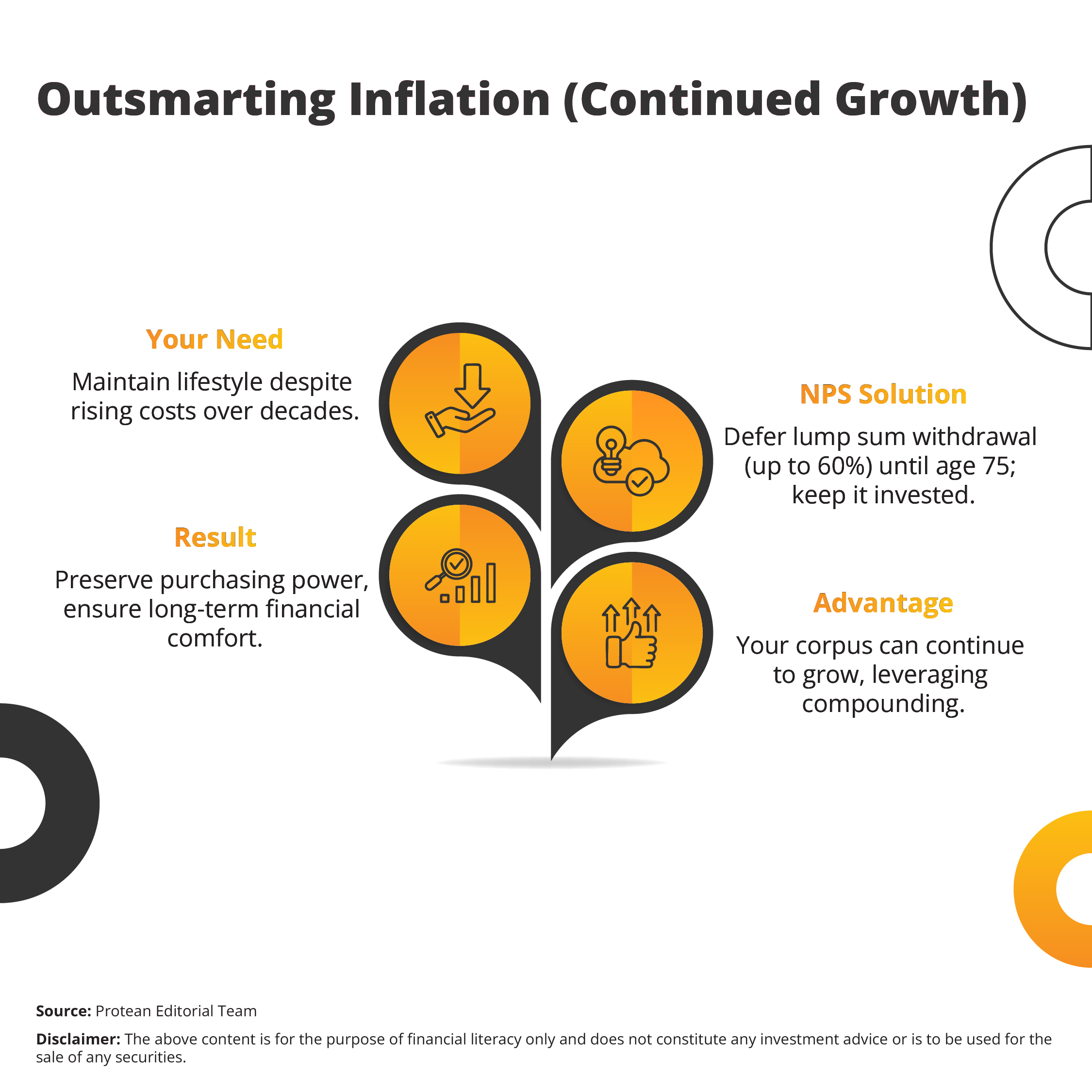

Scenario 5: Combating Inflation and Maintaining Lifestyle – Continued Corpus Growth

Retirement would span many years. During this extended period, inflation can stealthily erode the purchasing power of your accumulated savings. A fixed income or a static lump sum might prove insufficient to maintain your desired lifestyle over two or three decades. A significant NPS benefit lies in its potential for continued corpus growth even after you enter retirement, helping to combat inflation and preserve your purchasing power.

While a portion of your corpus is typically annuitised at retirement, you have the option to defer the withdrawal of the remaining 60% lump sum until age 75. During this deferment period, or even within the investment phase before annuitisation, your un-annuitised corpus remains invested according to your chosen asset allocation. You can choose from various Pension Funds (PFs) and investment options (Equity - E, Corporate Bonds - C, Government Securities - G, and Alternative Assets - A) to manage your risk and return expectations.

This continued investment can allow your funds to potentially grow further, compounding over additional years. This growth can act as a natural hedge against inflation.

For example, if you defer your lump sum withdrawal, and the market performs favorably, your remaining corpus can continue to appreciate. This increased value at the time of final withdrawal provides a larger sum to counter the rising cost of living, helping you maintain your lifestyle and affording you the flexibility to meet unexpected expenses that arise due to inflationary pressures.

This ongoing growth potential is a crucial advantage of NPS investment, distinguishing it from instruments that offer only fixed returns or static lump sums, and thereby contributing significantly to a truly tension-free and financially secure retirement.

| Do you already have an NPS account? Click here to make your contribution. |

Conclusion: NPS - A Comprehensive and Adaptable Retirement Tool

NPS benefits can stand as a comprehensive and adaptable tool that actively supports a tension-free retirement in India. It can offer the following:

- A steady income through its diverse annuity options

- Provide crucial flexibility through partial withdrawals for life's significant events

- Addresses critical healthcare contingencies via lump sum access

- Secures the financial future of loved ones through robust nominee benefits

- Possesses the vital potential for continued corpus growth to combat inflation.

Understanding these multiple facets of NPS investment can empower you to plan your retirement finances strategically. With NPS, you can confidently navigate your golden years with peace of mind, unwavering financial security, and the freedom to truly enjoy the fruits of your lifelong efforts.

| Click here to learn more about NPS features. |