India’s lending ecosystem continued its rapid expansion into March 2025, fueled by over $21 billion in liquidity support from the RBI to boost credit growth. However, this surge has been marred by a significant spike in loan-related frauds, with ₹21,367 crore reported in just the first half of FY25, an eightfold increase year-on-year. Most of these frauds were concentrated in the advances category, exposing critical gaps in borrower verification.

As lenders race to scale, robust income validation has become essential to ensure compliant, secure, and sustainable lending operations.

No longer a mere checkbox on the compliance sheet, income validation is now central to credit risk management, regulatory alignment, and customer trust. Traditional verification methods viz., paper-based and manual processes often fall short in today’s digital landscape.

| In contrast, API-powered income verification solutions, such as those from Rise With Protean, are redefining how financial institutions onboard borrowers efficiently and securely. |

Income Validation: The Backbone of Lending

At its core, income validation allows lenders to make informed decisions.

It helps answer key questions such as:

‘Can this borrower repay the loan?’,

‘What is their real disposable income?’,

or

‘Are the documents genuine?’

Income validation drives the following:

1. Reduced Loan Defaults

There is a need to verify actual income levels and cash flows. With income validation, lenders can filter out ineligible borrowers early, drastically reducing default rates and Non Performing Asset (NPA) risks.

2. Right-sized Loan Offers

With accurate income insights, financial institutions can tailor loan amounts, EMI terms, and interest rates, aligning credit with the borrower’s real repayment capacity.

3. Regulatory Compliance

The RBI mandates thorough customer due diligence, especially for regulated entities such as Non Banking Finance Companies (NBFCs) and digital lenders. Proper income verification not only reduces the risk of bad loans but also ensures audit readiness and shields lenders from regulatory penalties.

| Let us learn about PAN for income validation here. |

A Closer Look At Traditional Income Verification Methods

Depending on the borrower type, lenders can assess a mix of documents:

- Salaried borrowers: Salary slips, bank statements, Form 16, and ITRs.

- Self-employed/SMEs: Income tax returns, audited financials, business incorporation certificates.

- Universal metrics: Debt-to-income ratio, CIBIL scores, outstanding liabilities.

| When verified thoroughly, these inputs create a detailed borrower profile, enabling smarter risk assessment. |

However, manual validation of these documents is riddled with challenges.

The Risks of Inadequate Income Validation

Without automated and accurate income verification, lenders might face several operational and financial risks. These are as follows:

a. Increased Loan Defaults

Incomplete or falsified income details result in poor credit decisions. Borrowers who lack the ability to repay eventually default, triggering losses and increasing NPA burdens.

b. Operational Delays

Manual scrutiny of bank statements or Form 16s not only increases turnaround time but also frustrates borrowers, leading to application drop-offs.

c. Fraud Risks

Document forgery, identity fraud, and synthetic borrowers are difficult to detect without digital systems. Fraudsters exploit paper-based systems and create loopholes in verification pipelines.

d. Regulatory Exposure

Non-compliance with RBI’s KYC and income verification guidelines can trigger audits, fines, or worse, reputational loss in an increasingly competitive lending market.

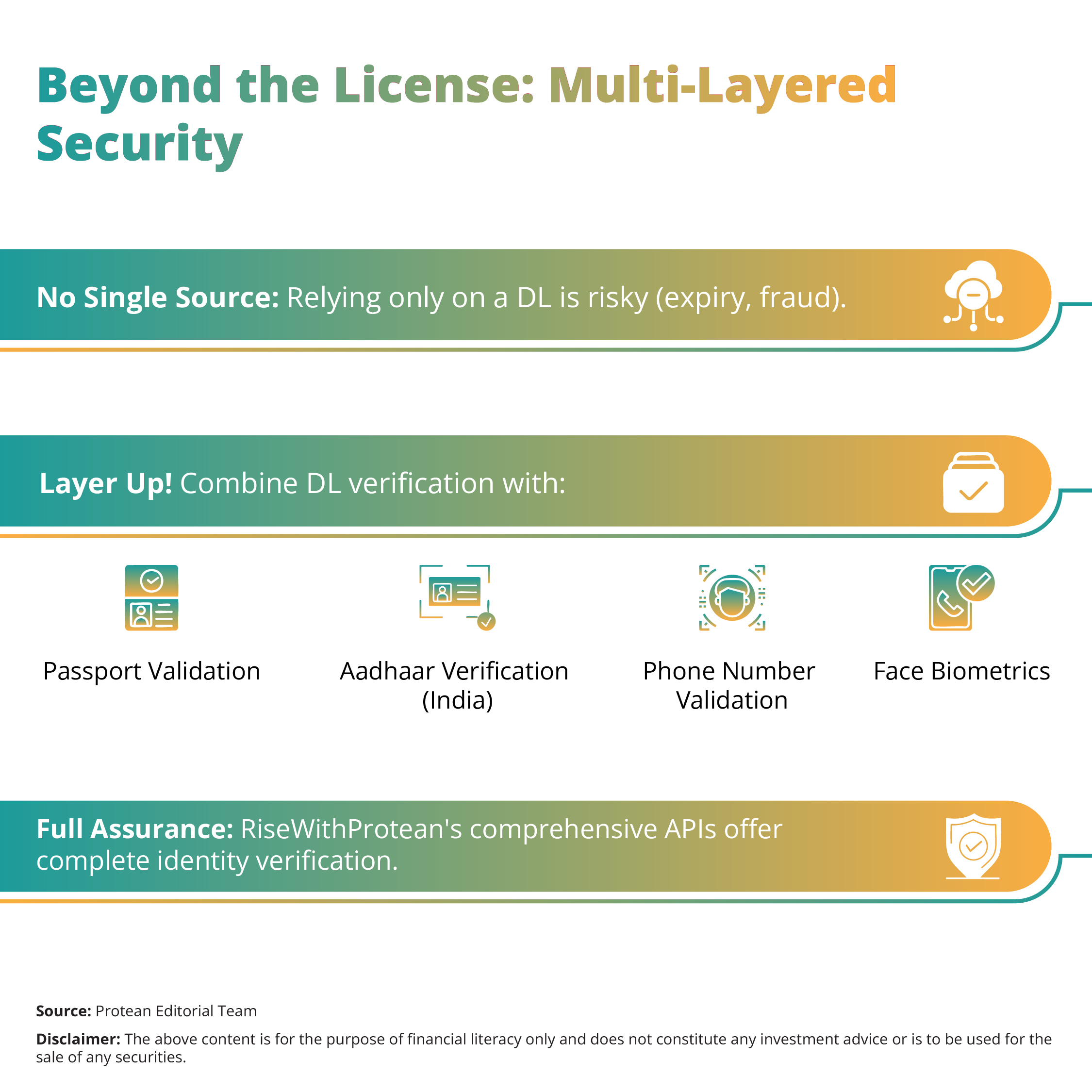

How AI & APIs Transform Income Verification

| Digital lenders and banks are now pivoting to AI-powered APIs for real-time income validation. These solutions streamline onboarding, improve accuracy, and embed trust into the lending process. |

Following are the Major Advantages of Digital Income Verification:

- AI-OCR Automation: Extract and analyse salary slips, bank statements, or ITRs with intelligent character recognition for faster processing.

- Trusted Data Sources: APIs integrate seamlessly with government-authorized platforms like Account Aggregators, Income Tax Department APIs, or GSTN, enabling direct income validation.

- Fraud Detection: Face match algorithms, behavioral analytics, and document signature checks flag inconsistencies in real-time.

- Customer Experience: Reduce onboarding time from days to minutes with faster approvals and fewer document touchpoints.

- Data Compliance: Solutions like those from RiseWithProtean ensure data localization, explicit consent capture, and DPDP compliance.

RiseWithProtean’s Income Validation APIs: Scalable, Secure, Smart

The Income Validation API suite by RiseWithProtean is purpose-built for today’s digital lenders and BFSI stakeholders.

The following features set it apart:

- Plug-and-play API suite for easy integration with loan origination systems.

- AI-powered OCR for high-accuracy extraction and parsing of financial documents.

- Real-time validation through secure links with Income Tax, GST, and banking data sources.

- Compliance-first architecture aligned with RBI and DPDP regulations.

- Analytics-ready insights for better underwriting and monitoring.

| Whether it is a digital NBFC onboarding gig workers, or a bank offering business loans to MSMEs, Protean’s APIs are designed to deliver fast, fraud-proof, and compliant lending journeys. |

Best Practices for Lenders

To harness the full potential of income validation in lending, institutions should adopt the following practices:

- Adopt API-based digital verification tools: Avoid manual delays and inaccuracies.

- Prioritise data security: Ensure end-to-end encryption, data localization, and compliance with the Digital Personal Data Protection (DPDP) Act.

- Educate borrowers: Simplify the onboarding journey with guides on document submission and consent processes.

- Use real-time dashboards: Monitor income trends, flag anomalies, and fine-tune credit scoring models with live analytics.

Conclusion: Income Validation is Non-Negotiable

In India’s fast-evolving credit market, income validation is no longer a backend function. It is the backbone of safe, scalable, and compliant lending. From reducing fraud to enhancing underwriting, its benefits are multifold.

| Modern tools like the RiseWithProtean Income Validation APIs enable lenders to embrace this transformation ensuring faster decisions, lower risks, and higher trust. |