8:32 a.m. Churchgate local was its usual mix of chatter, rushing bags, and folded newspapers. Amid the crowd, Riya, a financial planner, balanced her coffee and opened her laptop, which displayed a blog post on Multiple Scheme Framework (MSF) on Protean eGov Technologies Ltd. website. Next to her sat Aarav, a young professional scrolling through investment blogs.

“Is that NPS?” he asked curiously.

Riya smiled. “Yes. I’m reading about this latest development in the pension stream, viz., the Multiple Scheme Framework (MSF). It is changing how investors manage their NPS portfolios.”

Aarav nodded. “I also read it in a news article. Can we actually move between those schemes? And what about tax benefits?”

Riya laughed. “Perfect questions for this ride. Let’s make your morning a finance lesson.”

Breaking Down the MSF: Flexibility, Risk, and the Equity Option

“Earlier,” Riya began, “each Pension Fund Manager (PFM) under the National Pension System (NPS) could offer just one scheme per asset class, one equity, one government bond, one corporate debt fund. It was simple, but not flexible.”

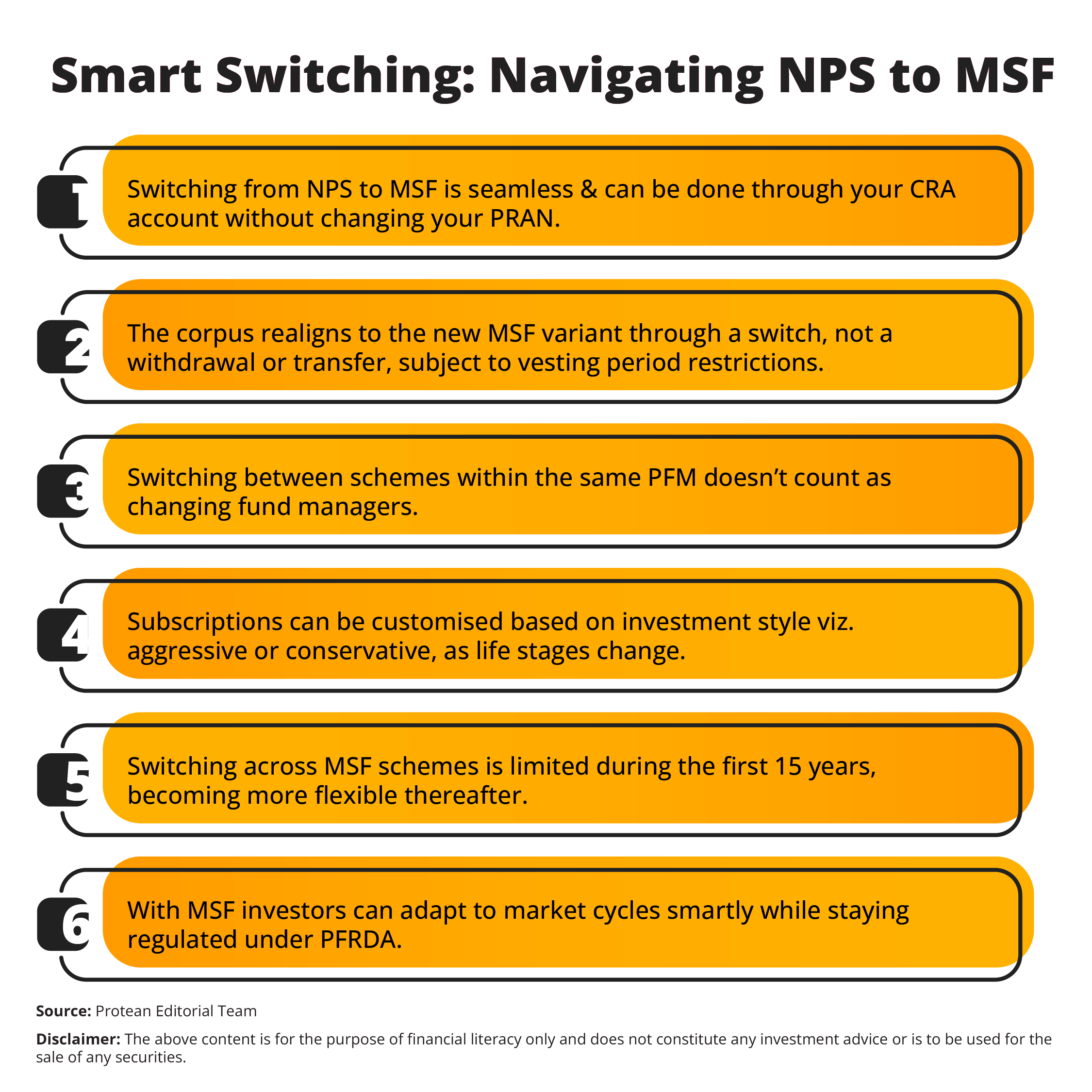

She continued, “Now, after the PFRDA circular on Multiple Scheme Framework, PFMs can offer multiple variants under each asset class, commonly including Aggressive, Moderate, and Conservative options. This means within your existing PRAN, you can choose your desired risk level without switching your PFM or account.”

Aarav looked impressed. “So, I could choose a more growth-oriented equity fund or a balanced one under the same manager?”

“Exactly. Suppose you like the SBI Pension Fund. Earlier, you got just one equity option. Now, with MSF, SBI might offer three such as, an Aggressive Equity Scheme with 100% equity exposure, a Balanced Equity Scheme with 75%, and a Conservative version with lower volatility.

You can align your portfolio with your age, goals, and comfort level.”

“That makes NPS much more investor-friendly,” Aarav said.

“It does,” Riya nodded. “NPS was always about long-term retirement wealth. MSF just gives it mutual-fund-like flexibility, while retaining low costs and regulatory protection.”

Switching Between NPS and MSF Schemes

As the train passed Dadar, Aarav asked more questions. “So, if I already have an NPS account, how do I move to MSF?”

Riya explained, “It’s easy. If your PFM offers MSF variants, you can switch through your CRA account. Your PRAN stays the same, and your accumulated corpus simply moves to the new scheme you select. It’s not a withdrawal or transfer, it is just a realignment.”

“Does it count as changing fund managers?” Aarav asked.

“No, it’s within the same PFM. You can change your fund manager once a financial year, but switching between schemes under MSF doesn’t count as that. It has a more granular control, as you’re adjusting your investment style, not your manager.”

Riya added, “The system restricts switching between MSF schemes during the initial 15-year vesting period, allowing switches mainly to common schemes. After this period, subscribers have more flexibility to switch between schemes to align with long-term goals. So, you could start with an aggressive scheme when you’re young, and later move to a conservative variant as you approach retirement.”

Aarav nodded. “That’s smart. No more being stuck in one strategy for decades.”

“Exactly,” Riya said. “Think of it like driving, you can shift gears according to terrain. The MSF makes NPS flexible enough for market cycles, but still disciplined under PFRDA supervision. You get the benefits of personalisation without the risks of speculation.”

Are MSF Schemes Treated Differently Under the IT Act?

The train slowed near Charni Road. Aarav sipped his tea thoughtfully. “Alright, flexibility sounds great. But what about taxes? Are MSF schemes treated differently?”

Riya smiled. “That’s the best part, nothing changes on the tax side. The MSF is not a new product; it’s just an extension of your existing NPS. So, the Income Tax Act benefits remain identical.”

She continued, “You can still claim deductions under Section 80CCD(1), up to ₹1.5 lakh within the Section 80C limit, plus an additional ₹50,000 under Section 80CCD(1B) exclusively for NPS. If you’re a salaried employee, your employer’s contribution up to 10% of salary (14% for central government employees) under Section 80CCD(2) also remains tax-exempt.”

“So, even if I move from my current equity scheme to an MSF Aggressive Equity Scheme, I won't lose tax deductions?” Aarav asked.

“Not at all,” said Riya. “The law recognises contributions to your NPS account, not the internal scheme you pick. Whether you’re in a standard or MSF variant, the tax benefit applies equally.”

“And at retirement?”

“The withdrawal and annuity rules stay exactly the same. At 60, you can withdraw 60% of your NPS corpus as a lump sum which is tax-free, while the remaining 40% must be used to buy an annuity. Partial withdrawals allowed for higher education, marriage, or medical needs are also tax-free within PFRDA’s limits. So, MSF gives you more control, but under the same trusted structure.”

“That’s reassuring,” Aarav said. “Flexibility without losing benefits sounds ideal.”

“Exactly,” Riya said. “PFRDA designed it that way to attract more young investors while keeping NPS’s disciplined retirement focus.”

Conclusion

As the train neared Churchgate, morning sunlight streamed through the windows. Aarav smiled, visibly clearer about his next investment step.

“You’ve changed my view on NPS,” he said. “I used to think it was rigid, like a government savings plan. But with MSF, it feels like a well-built investment platform.”

Riya nodded. “That’s the evolution. The Multiple Scheme Framework has made NPS more responsive to modern investors, however, it currently applies to non-government subscribers only. You can tailor your exposure to equity, corporate debt, or government bonds as per your financial life stage and all while keeping your tax incentives, low cost, and regulatory safety net.”

She added, “And since the transition is handled digitally through CRAs, managing and monitoring your pension portfolio has never been easier. The focus remains on your end goal, building a reliable retirement corpus.”

Aarav packed his bag, smiling. “So, I can start with an aggressive MSF scheme now and shift to conservative later, all inside my same PRAN?”

Riya laughed. “Exactly. Think of it as growing wiser with your money, without ever stepping off the track.”

As they stepped onto the platform, she added, “Retirement planning isn’t about locking your money, it’s about evolving with it. The MSF just gave NPS the flexibility to move with you.”

Aarav nodded. “Well, this train ride was worth more than my last webinar.”

Riya smiled. “That’s Mumbai for you; you never know when you’ll learn how to make your future ride smoother.”