It is a late afternoon at the college campus café. Raj and Meera, both MBA finance majors, are sipping cold coffee after their Investment Management lecture. Their laptops are open, not for assignments this time, but to review their NPS dashboards on the Protean eGov Technologies Ltd. portal.

Meera: Raj, everyone’s talking about this Multiple Scheme Framework in NPS lately. My dashboard even shows a new section about “MSF-eligible contributions.” Do you know what that means?

Raj: Oh yes! The Multiple Scheme Framework (MSF) is the latest initiative by the Pension Fund Regulatory Development Authority (PFRDA), officially introduced in 2025. It allows subscribers like us, in the non-government category, to invest in multiple schemes under one PRAN. It’s a big step towards flexibility in the NPS ecosystem.

Meera: Sounds exciting. But what about all my older contributions from 2018 till now? Can those be moved into the MSF structure, or is MSF only for new contributions?

Raj: Great question! That’s exactly what many investors are wondering. Let’s break it down.

MSF’s Rulebook on Legacy Funds

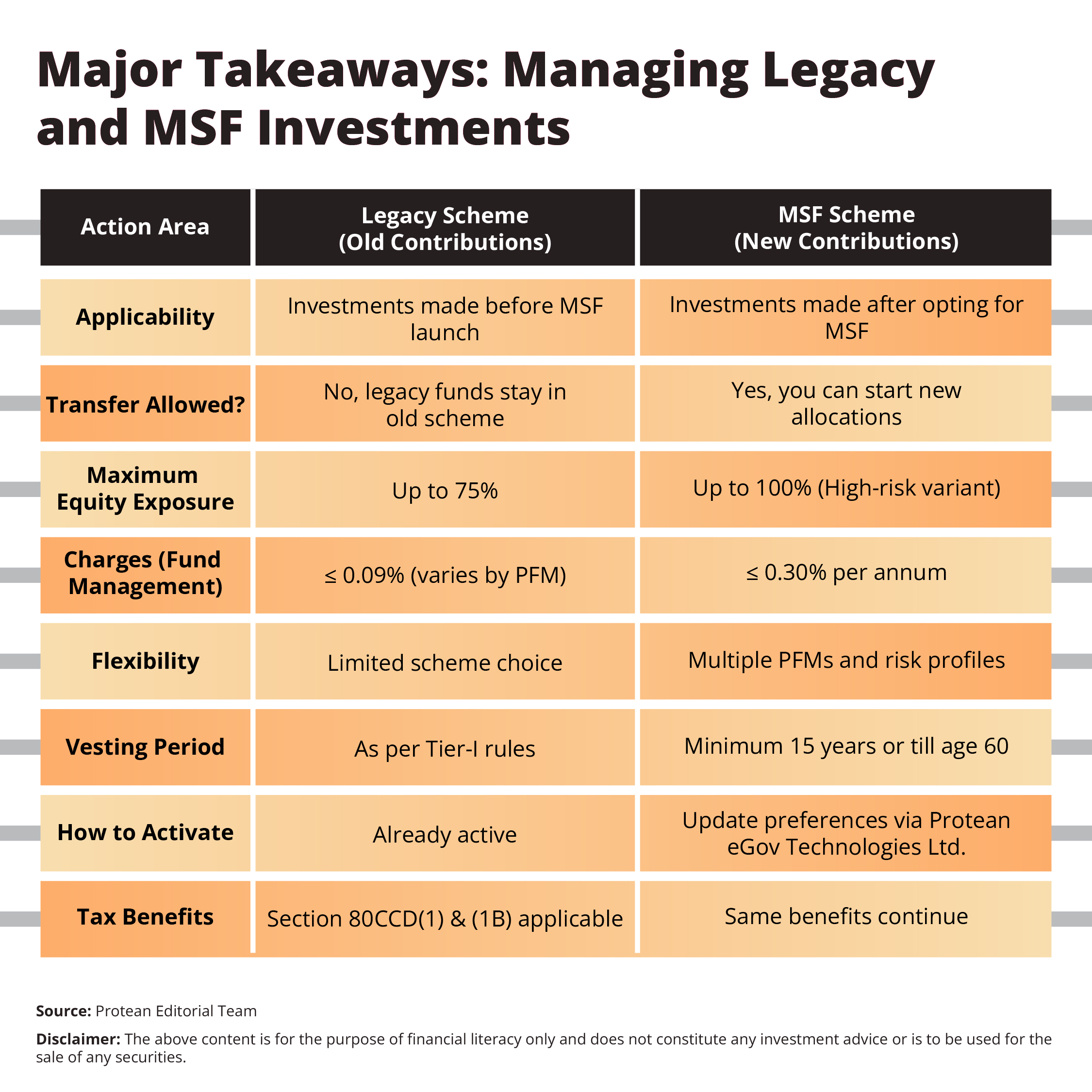

Raj: According to the latest updates on the Protean eGov Technologies Ltd. platform and PFRDA’s notification, all your earlier NPS contributions, the ones made before the MSF launch are classified as legacy funds. These funds stay invested in the existing “common scheme structure” under your chosen Pension Fund Manager (PFM).

Meera: So, they don’t get automatically transferred to MSF?

Raj: Exactly. According to Protean eGov Technologies Ltd., the legacy contributions remain where they are. The MSF framework applies only to future contributions or newly chosen schemes. This ensures continuity and protects long-term compounding on past investments.

Meera: Makes sense. Basically, PFRDA wants to give us more flexibility going forward without disturbing what’s already working.

Raj: Right. Under the MSF, each PFM can now offer multiple schemes with varying risk profiles such as Aggressive, Moderate, or Conservative, allowing equity allocations up to 100% in some schemes. So, you can design your new NPS strategy while your legacy investments continue in the background.

Managing the Entire Corpus

Meera: Okay, but how do I look at my total NPS wealth now? Legacy and new MSF investments, won’t that get confusing?

Raj: Not at all. Think of it like having two compartments in the same locker.

Meera: (smiling) A pension locker?

Raj: Exactly! One compartment holds your legacy corpus. It is the steady base that’s been compounding for years. The other holds your MSF corpus, where your new contributions go into flexible, diversified schemes.

Meera: So, both stay under my Protean PRAN, right?

Raj: Yes. Protean’s dashboard will display both portions separately, giving you a complete view of your retirement wealth. And because your PRAN remains the same, your tax benefits, withdrawal rules, and annuity options stay intact.

Meera: That’s convenient.

Raj: Totally. Plus, MSF introduces a new level of customisation. For instance, younger investors can now opt for up to 100% equity allocation in certain MSF variants, something that wasn’t allowed earlier.

Meera: It means, MSF can enable strategic diversification within the same pension structure.

Raj: Exactly! And even with this flexibility, the cost advantage remains. MSF schemes are capped at just 0.30% per annum in fund management charges. So, you are still investing in one of India’s most cost-efficient retirement tools.

How to Strategise the Switch

Meera: Alright, Raj. Now tell me how I can actually start this MSF journey.

Raj: Easy! Let’s call it the five-step MSF strategy.

Review your existing holdings

Log in to your Protean eGov Technologies Ltd. account and download your Transaction Statement. You can check the fund manager, scheme type, and allocation for your existing corpus. That’s your legacy base.

Explore MSF options

Each PFM offers multiple risk profiles i.e., High-risk (up to 100% equity), Moderate (balanced), and Conservative (debt-oriented, if offered). You can study their performance trends and risk ratings before choosing.

Decide how to allocate new contributions

You can continue investing in your legacy scheme or start routing future contributions to the MSF variant of your choice. For example, if you are 30 yrs old, you might go 80% into the Aggressive MSF scheme and 20% into Moderate.

Update preferences via Protean’s portal

On your Protean dashboard, you can use the “Scheme Preference Change” option. Select the MSF variant and confirm your percentage allocation. The change applies to all future contributions while keeping older investments untouched.

Review annually

Your MSF account will evolve with markets. Once a year, you can check if your equity-debt balance still aligns with your goals.

Meera: That’s so systematic! Basically, I can continue my existing NPS investment and use MSF to tailor my new contributions more actively.

Raj: Exactly. It’s like you’re building a two-layer retirement plan, a steady base and flexible top-up, both under one account.

Meera: Nice analogy.

Conclusion

Meera: You know, Raj, MSF, has widened the investment scope.

Raj: Absolutely. PFRDA has evolved NPS from a default retirement option to a more strategic financial instrument. Now, you can align your pension portfolio with your age, risk appetite, and long-term goals.

Meera: And the best part is that my old contributions continue compounding in the legacy schemes while I use MSF to capture new opportunities with fresh investments.

Raj: That is the power of evolution within structure. Stability from legacy schemes and flexibility through MSF, the perfect combination for retirement planning in a changing economy.

Meera: Guess I am updating my NPS preferences tonight, as I understand MSF now. My key takeaways are:

Major Takeaways: Managing Legacy and MSF Investments

Raj: And do not forget to always think long-term. The best pension is the one that grows with you. And, to sum it up: your NPS journey through Protean just got a major upgrade. You are not replacing your old investments, you’re enhancing them.

Meera: A balanced blend of tradition and innovation is good for financial planning.

Raj: Exactly! With MSF, your NPS is no longer just a pension, however, it’s your personalised retirement portfolio.

Frequently Asked Questions

Q1: Can I transfer my old NPS contributions to the MSF structure?

No. As per PFRDA guidelines, existing (legacy) contributions remain under the common scheme. MSF applies to new contributions only.

Q2: Can I have both legacy and MSF schemes under the same PRAN?

Yes. Your PRAN remains the same. You can continue your legacy scheme and direct future contributions into one or more MSF schemes.

Q3: Are MSF schemes costlier?

Not significantly. The fund management fee is capped at 0.30% per annum which is still much lower than most mutual funds or ULIPs.

Q4: Who is eligible for MSF?

MSF is available for non-government (All Citizen and Corporate) subscribers under the NPS. Government sector employees are not covered yet.

Q5: Can I switch between MSF schemes easily?

Switching between different MSF schemes is allowed only after the vesting period of 15 years or at normal exit. However, you can switch from an MSF scheme to a common (legacy) scheme during the vesting period if needed.