Radhika sat at her favourite café in Mumbai, going through her NPS statement. In eight years of disciplined investing under the National Pension System (NPS), her savings had grown well. But she wondered, “Can I make my corpus grow faster without leaving NPS?”

While reading about new updates, she discovered the Multiple Scheme Framework (MSF), introduced by the Pension Fund Regulatory and Development Authority (PFRDA).

She realised that her Permanent Retirement Account Number (PRAN), the 12-digit number linked to her NPS account, was not just a record of savings. It was now a gateway to invest smarter and grow faster within the NPS.

Here is what Radhika learnt about the Multiple Scheme Framework (MSF):

MSF Revolution: What It Means for Your Growth

Radhika learned that, until recently, NPS subscribers were limited to one scheme per asset class per pension fund manager (PFM). Starting 1 October 2025, PFRDA has allowed non-government sector subscribers to hold multiple schemes under a single PRAN, each managed by the same or different Pension Fund Managers (PFMs).

She realised that this is the essence of the Multiple Scheme Framework (MSF) which is a structural shift that empowers NPS subscribers to get the benefit of diversification.

She also understood that MSF enables subscribers to invest in schemes with up to 100% equity exposure, compared to the earlier 75% limit. This change has been made to:

- Give young investors more flexibility and better long-term growth options.

- Keep the same safety, tax benefits, and structure of NPS.

- Provide more freedom to build a portfolio with multiple fund choices and wider asset exposure.

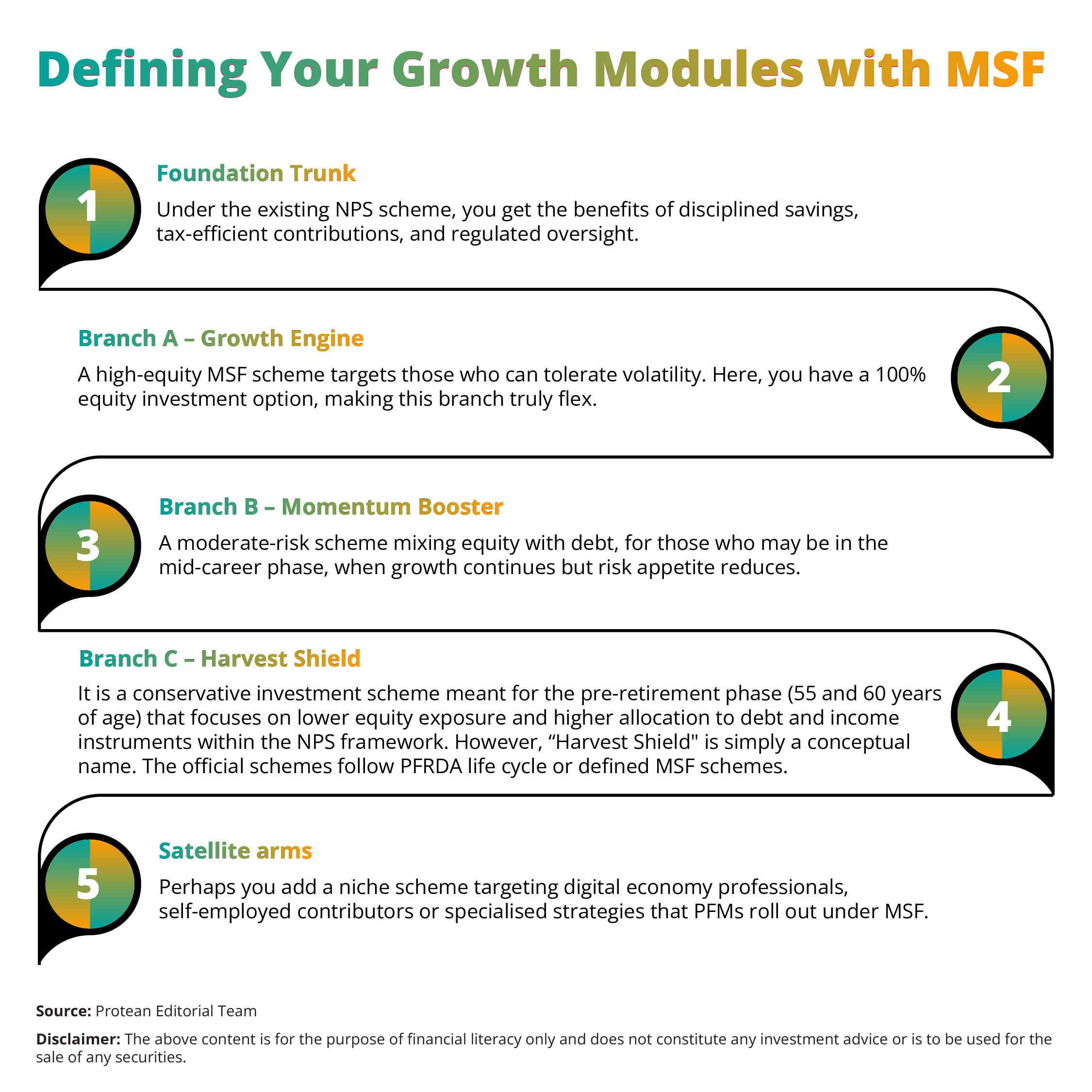

Defining Your Growth Modules

Radhika imagined her corpus as a tree. Its roots are firmly in the NPS structure; its branches made up of modular growth arms viz., the MSF. She found out which of the following growth modules you need:

These “modules” don’t replace NPS, they live within your PRAN, providing a multi-layered yet unified retirement architecture.

Building the Modular Portfolio

Radhika also saw her job profile as an example and learned how a modular portfolio works.

Radhika is a marketing professional. She earns Rs.10,000 per month to her NPS. Under the MSF:

- As a part of the core allocation, she keeps 40% in her existing NPS scheme for stable growth and continuity.

- Further, for growth allocation, she adds (40%) in a new MSF high-equity scheme offered by her Pension Fund Manager, tapping into long-term market returns.

- In addition, as a diversified cushion, she invests 20% in a moderate MSF scheme (equity + debt), ensuring her portfolio isn’t overly exposed to volatility.

Each scheme under MSF follows clear regulatory guardrails, ensuring transparency, asset segregation, and defined risk profiles.

Radhika may combine different MSF schemes within NPS. With this, she may build her self-balancing growth machine, aligned with her financial goals.

Diversification within one account (across fund managers, asset classes, and strategies), age-aligned flexibility (gradually shifting from high equity to conservative debt), ease of monitoring (with unified PRAN access and CRA dashboards) and long-term compounding are some of the important benefits of this modularity.

Executing the Strategy and Fund Flow

Radhika can follow these steps of executing strategy of the modularity:

- Log into CRA dashboard: Under MSF, her PRAN remains the same, and she can view multiple scheme holdings across CRAs via PAN-based consolidation.

- Choose scheme allotments: Using the CRA interface, she may allocate new contributions into selected schemes. For example: 40% into a high-equity scheme, 40% in default Active Choice, 20% in a moderate scheme.

- 3. Systematic contribution & monitoring: Radhika may set reminders for monthly/quarterly contributions through CRA or personal financial tools, while systematically contributing as per her plan.

- Rebalance at milestone ages: At milestone ages like 45 and 55, she may rebalance by reallocating future contributions across schemes. Under MSF, switching between different schemes is permissible only after completing a minimum 15-year vesting period or upon retirement; however, switching to common schemes is allowed anytime.

- Exit planning: When she is near retirement, she can plan harvest by choosing annuity or lump-sum exit as per NPS rules.

Through this journey, Radhika learnt that she is not just depositing money into “the NPS scheme” and forgetting it; she is steering a growth engine, using MSF to tune the strategy, while staying anchored in the safety and simplicity of NPS.

Conclusion

When Radhika left the café, notebook closed but mind alive with possibilities, she realised the story of her retirement savings had just turned a new page. The NPS scheme still remained her trusted vehicle, built on discipline, regulatory strength and long-term focus. Thanks to the Multiple Scheme Framework (MSF), she could diversify more effectively and align her investments to different stages of her life.

Like Radhika, whether you’re 25 or 45, MSF offers you flexibility and opportunity to select growth when your horizon is long, tone down risk when you approach retirement, and stay within the NPS ecosystem that you already understand and trust. The journey is not about choosing between NPS and other options, but about using NPS alongside MSF to invest your corpus wisely while maintaining pension discipline.

Frequently Asked Questions

Q1: What is the multiple scheme framework (MSF)?

MSF is a regulatory reform under the NPS for non-government subscribers that allows you to hold multiple schemes under a single PRAN (Permanent Retirement Account Number). Pension fund managers can offer differentiated schemes for various risk profiles and groups.

Q2: Does MSF replace the NPS scheme?

No, MSF doesn’t replace the NPS scheme. The NPS scheme remains the foundational platform and its Tier-I account, tax benefits, regulatory oversight stay intact. MSF simply overlays it, allowing you to choose among multiple schemes (within NPS) for more customisation.

Q3: How much equity exposure is allowed under MSF?

Under MSF, non-government NPS subscribers can access high-risk variants of schemes with equity exposure up to 100%. This is a major shift from the earlier effective cap.

Q4: Can I switch between schemes under MSF whenever I want?

Switching between MSF schemes is permitted but subject to a minimum vesting period of 15 years or retirement age, whichever is earlier. During the vesting period, switching among MSF schemes is limited, but after vesting, freer switching is allowed.

Q5: Is this only for new NPS subscribers?

No, MSF is designed to apply to existing subscribers (non-government sector) of NPS too. You should verify with your CRA about how to migrate or allocate under MSF.

Q6: What should I be cautious about?

While MSF opens growth potential, higher equity means higher volatility. Use the modules to align with your life stage and risk appetite. Also keep costs, switching rules, and scheme mandates in mind.