It’s a universal aspiration to have a financially secure, comfortable and worry-free life post-retirement.

But there is a long way to this goal that can involve regular investing and strong financial planning.

So, how can we make a smart move towards it?

In India, the National Pension System (NPS) has emerged as a dedicated retirement savings vehicle.

Let us learn more about NPS investment, the inherent NPS growth potential and benefits.

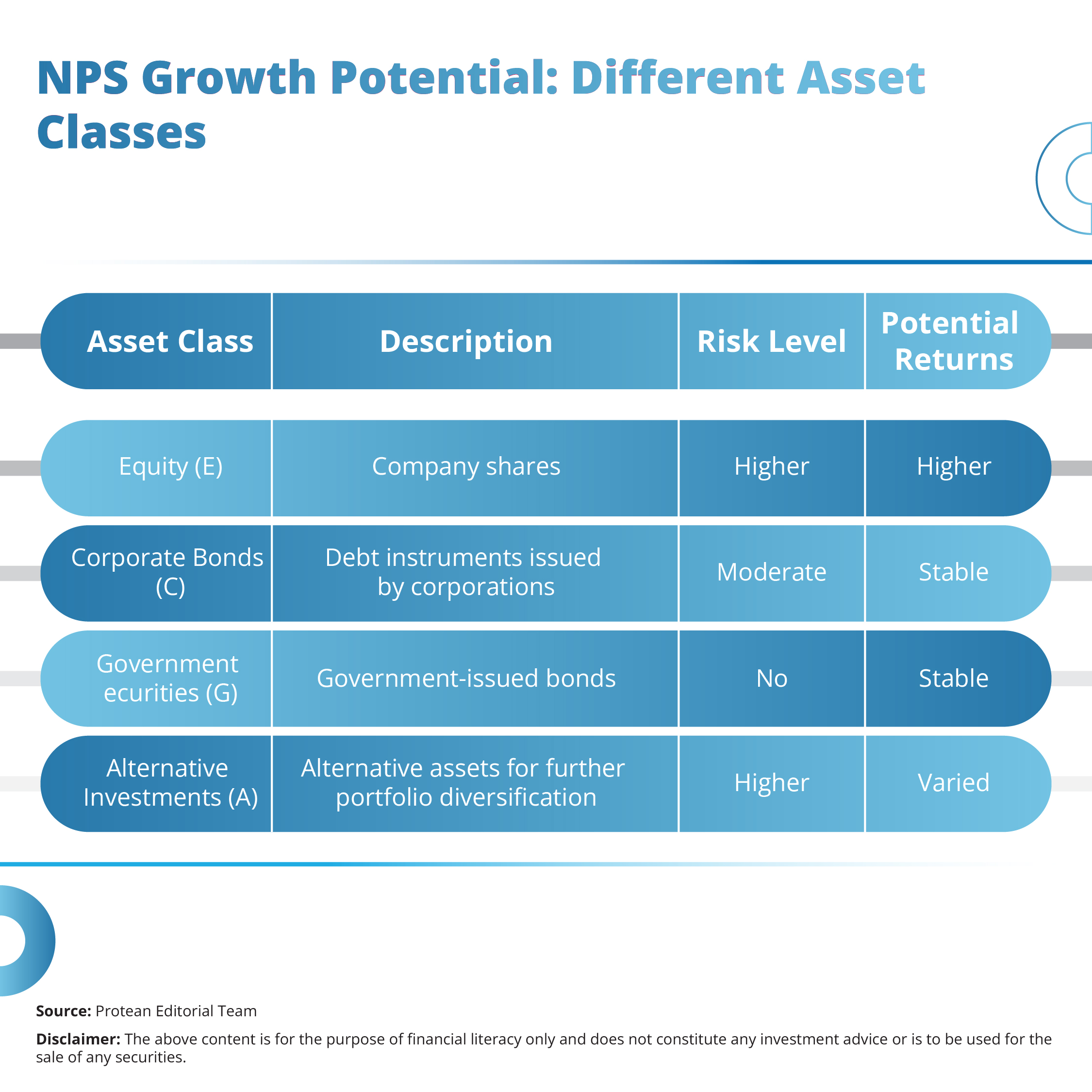

NPS Growth potential

At its core, the NPS investment strategy is intricately linked to market performance across diverse asset classes. This market linkage forms the very foundation of its growth potential.

You can direct your contributions into the following four primary asset classes:

The exposure to equity, in particular, can be crucial for NPS returns over the long term. Therefore, the earlier you start, the more time you can have for compounding.

NPS has two distinct investment choices to manage this asset allocation:

- With Active Choice you can actively decide the percentage of your contribution to each asset class. Until the age of 50, you can allocate up to 75% of your funds to equity. Thus, your portfolio can aggressively grow in your younger years.

- With Auto Choice (Lifecycle Funds) you can automatically adjust your asset allocation based on your age, gradually reducing equity exposure and increasing debt allocation as you near retirement.

| Click here to register for an NPS subscription now. |

Power of Low Costs: Maximising Returns Over Time

A standout feature of NPS investment that directly can contribute to its long-term growth potential is its remarkably low cost structure.

When a smaller portion of your investment is deducted as management fees, a larger portion remains invested. This can allow more capital to compound over decades. This compounding effect, amplified by lower costs, significantly boosts your overall wealth creation. A comparison of the NPS investment performance versus other traditional investment avenues often highlights this distinct cost advantage, demonstrating how seemingly small differences in expense ratios can lead to substantial variations in your final corpus over a 20 or 30-year investment horizon. This cost efficiency truly underscores the power of maximizing NPS returns.

| Click here to register for Tier-i and Tier-II NPS accounts. |

Tax Benefits and Growth in NPS

You can claim the following tax deductions for your Tier-I NPS investment:

- Section 80CCD(1B): An exclusive additional deduction of up to ₹50,000 for NPS contributions is available. This is over and above the Section 80C limit. This specific benefit makes NPS particularly attractive for tax planning.

- Section 80CCD(2): For salaried employees, employer contributions to NPS are also deductible, up to 10% of their basic salary plus dearness allowance.

Furthermore, at the time of retirement, up to 60% of your lump sum withdrawal is tax-free, and the remaining portion used to purchase an annuity is also tax-exempt.

Power of Compounding in NPS

Let us look at an example to understand compounding in NPS investment:

- You start contributing ₹5,000 per month to NPS at age 25.

- Your investment grows at an average annual rate of 10%

- Your corpus by age 60 would be significantly larger than if you started the same contribution at age 35.

- The difference lies in the additional 10 years of compounding that the former investment benefits from.

Compounding makes time your most valuable ally in maximising NPS investment performance.

| Want to maximise your NPS investment benefits? Check this blog now! |

Strategic Choices: Active vs. Auto

Optimising your NPS asset allocation for growth can require a strategic decision between the Active Choice and Auto Choice.

- Investors with a higher risk appetite, a good understanding of financial markets, and the willingness to periodically review their portfolio can potentially enhance their long-term growth by actively allocating a larger portion to equity (up to 75% until age 50) under the Active Choice.

- Conversely, the Auto Choice (Lifecycle Funds) can provide a more hands-off and disciplined approach. It can automatically adjust equity exposure downwards as you age, gradually shifting towards less volatile debt instruments.

| Take your first step towards post-retirement financial security, start investing in NPS now. |

Role of Fund Managers

You have the flexibility to choose from multiple Pension Fund Managers (PFMs). Each PFM has its own investment philosophy and track record. Investors can consider the historical NPS fund manager performance, their investment strategies, and their consistency when making their selection.

NPS vs. Other Long-Term Growth Options

For evaluating NPS vs other long-term investments like Public Provident Fund (PPF) or diversified equity mutual funds, we can compare their features.

Investing in NPS can uniquely combine market-linked returns across diverse asset classes, remarkably low fund management charges, and comprehensive tax incentives at various stages.

| Learn about NPS milestones here. |

Conclusion

NPS can offer advantages like:

- Market-linked returns across diversified asset classes

- Exceptionally low costs

- Attractive tax benefits

- Powerful effect of compounding

- Wealth-building

You can truly harness the NPS investment for a substantial retirement corpus, by understanding its features, making informed choices about asset allocation, and considering fund manager performance. Take informed NPS investment decisions,

| read our blogs here. |