With the launch of the Multiple Scheme Framework (MSF) under the National Pension System (NPS), non-government subscribers now have the flexibility to choose schemes with up to 100% equity allocation.

This landmark enhancement elevates the NPS scheme into a stronger, growth-oriented retirement investment avenue, giving subscribers the freedom to pursue higher long-term wealth creation.

Let us find ways of selecting a better 100% equity scheme under MSF, based on your risk appetite, investment horizon, and long-term financial goals.

Defining Your Risk Profile

Before allocating funds into a 100% equity MSF scheme, it is important to assess your risk appetite and long-term horizon.

If you are young (in your 20s or 30s), and have decades before retirement, you may have the opportunity to tolerate market volatility for expected long-term growth. On the other hand, if you are nearing retirement or prefer stability, full equity exposure might feel too volatile.

Beyond age, reflect on your financial responsibilities, dependents, other investments, and household cash flows.

If you have a stable income and manageable liabilities, aggressive equity allocation could build a substantial retirement corpus.

Conversely, if you anticipate large expenses or already have significant equity investments, a more balanced or moderate approach could be wiser. The 100% equity option under MSF is a powerful tool, but like any tool, it works best when aligned with a clear understanding of your personal risk tolerance and financial goals.

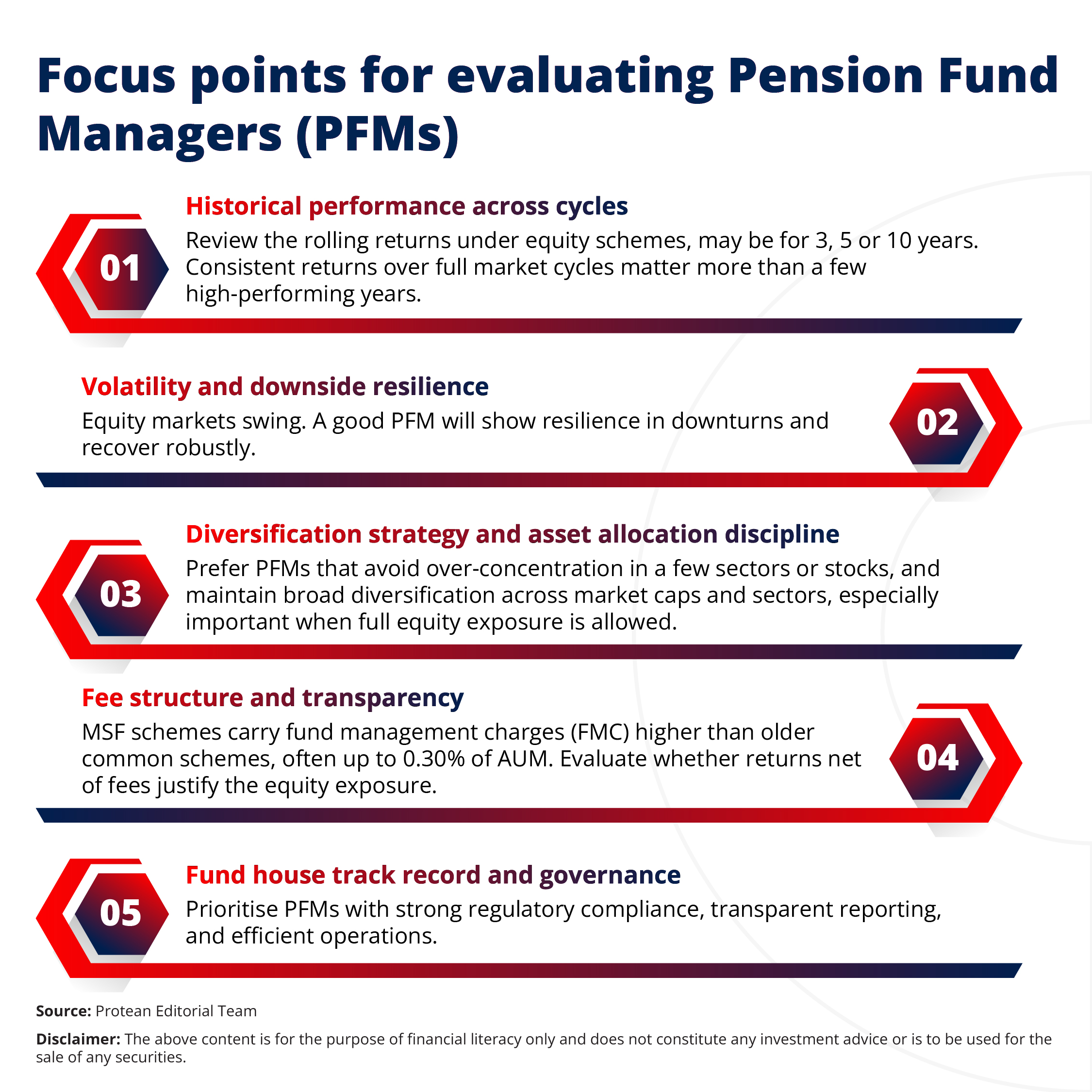

Analysing Pension Fund Managers

Under MSF, you choose not only the equity allocation but also the fund manager who will manage your contributions. This choice can significantly affect long-term returns, as different managers adopt different investment philosophies, stock-picking strategies, and risk management practices.

Moreover, since MSF permits holding multiple schemes, even from different PFMs under the same PRAN, you could diversify across more than one PFM. This spreads manager-specific risk and allows you to blend styles for optimal growth or stability.

Scheme Structure and Fee Analysis Under MSF

With the MSF in place, the structure of NPS has undergone a fundamental shift. The old “common schemes,” which restricted equity allocation to a maximum of 75%, remain available. But now PFMs can launch new “MSF schemes,” including high-risk variants offering up to 100% equity allocation for new contributions.

When choosing a 100% equity MSF scheme, examine these structural and cost-related factors carefully:

- Equity allocation cap: Confirm that the variant you choose indeed offers full (100%) equity exposure. For high-growth seekers, this unlocks maximum potential.

- Risk variant type: Most PFMs offer both high-risk (100% equity) and moderate-risk variants (blend of equity and fixed-income). Choose based on your comfort with volatility and long-term goals.

- Fund management charges (FMC): MSF schemes typically charge up to 0.30% of AUM, higher than older schemes. While modest, over decades this difference can erode returns.

- Possibility to hold multiple schemes: MSF allows you to hold more than one scheme under the same PRAN, enabling a mix of aggressive equity and conservative or moderate schemes for risk diversification.

- Transparency and reporting frequency: Ensure the scheme offers regular fund statements, asset-allocation disclosures, and transparent rebalancing policies. These help you track performance, understand risk, and make timely adjustments.

- Exit and vesting terms: Under MSF, the minimum vesting period is 15 years, or until age 60, whichever is earlier. Existing funds in common schemes cannot be auto-migrated to MSF, only new contributions go into the new schemes.

You ensure that your 100% equity selection under MSF by carefully analysing these factors. It is not just about chasing returns, but securing growth with full knowledge of costs, structure, and risk.

Optimising Contributions under the New Rules

With flexibility under MSF, you can adopt a strategic contribution strategy that aligns with your life stage and risk appetite:

- Front-load contributions early in your career: If you are young, allocate a major portion of your contributions to the high-equity MSF scheme. Over decades, equity’s compounding potential can significantly grow your retirement corpus.

- Use staggered (systematic) investments: Instead of lump-sum, contribute regularly (monthly or quarterly) to benefit from rupee cost averaging. This reduces the impact of market volatility over time.

- Split contributions across schemes if needed: You can blend high-equity MSF with a conservative scheme (e.g., debt or balanced) under the same PRAN to manage risk while participating in growth.

- Reassess periodically and rebalance: As you age or your risk tolerance changes, you may shift future contributions toward more conservative or balanced schemes. This helps preserve gains and protect capital.

- Leverage long-term horizon and tax advantages: Since NPS remains a regulated retirement product, disciplined long-term investing under MSF can combine equity growth with tax benefits, making it an efficient retirement savings vehicle.

Conclusion

The MSF represents a landmark upgrade for NPS, giving non-government subscribers a choice, flexibility, and control they never had before. With 100% equity schemes available, an NPS scheme can now rival traditional wealth-building instruments while retaining its retirement-first mandate. But this power demands prudence.

You can build a strong retirement corpus by matching scheme choice to your risk profile, evaluating pension fund managers carefully, reviewing scheme structure and costs, and following disciplined contribution strategies. MSF hands you the steering wheel, your discipline and strategic choices decide the destination.

Frequently Asked Questions

Q1: Who can opt for 100% equity under MSF?

Any non-government NPS subscriber, including private sector and self-employed individuals, can choose a 100% equity scheme under MSF.

Q2: Can I move my existing NPS funds into the new 100% equity MSF scheme?

No, only new contributions can go into MSF schemes and old balances cannot be shifted automatically.

Q3: Are fees higher under MSF compared to old NPS schemes?

Yes, MSF schemes charge slightly higher fund management fees, usually up to around 0.30% of AUM.

Q4: Is 100% equity suitable for all ages?

No, it can be better for younger investors with a long horizon more than those nearing retirement or uncomfortable with volatility.

Q5: Can I spread my NPS contributions across multiple schemes under MSF?

Yes, MSF allows you to invest in multiple schemes under a single PRAN for better diversification and flexibility.