The NPS has followed a singular philosophy for a decade.

- It has one subscriber, one active portfolio.

- You choose between equity, debt and alternative assets

- Select a Pension Fund Manager (PFM)

Thus, your entire retirement corpus would follow that single path. This was an effective "one-size-fits-all" approach, but now you can even separate your capital into different buckets for different financial goals.

The Multiple Scheme Framework (MSF) has completely transformed this structure. With MSF, you can hold multiple investment schemes simultaneously under a single Permanent Retirement Account Number (PRAN).

Thus, you can build a diversified fleet of portfolios: one for stability, one for aggressive growth, and another for moderate returns. You can do all of this within the same NPS account ecosystem.

Here’s how to leverage this powerful feature to build a strong multiple NPS account portfolio and optimise your wealth creation potential.

Understanding the NPS Multiple Scheme Framework

The Multiple Scheme Framework is a regulatory upgrade. With this, non-government subscribers can invest in more than one scheme at the same time.

In the past, if you wanted to change your strategy, you had to switch your entire corpus. Now, with MSF you can "add" new schemes without disturbing your existing investments.

You can consider your PRAN as a master folder. With the MSF, your single PRAN can hold multiple files (schemes). Each scheme has its own distinct asset allocation and risk profile, offered by Pension Fund Managers (PFMs).

Also, each scheme can operate like a separate NPS account internally, complete with its own Net Asset Value (NAV) and performance tracking. Thus, you can get the precision of a mutual fund portfolio with the low-cost and tax-efficient benefits of the NPS.

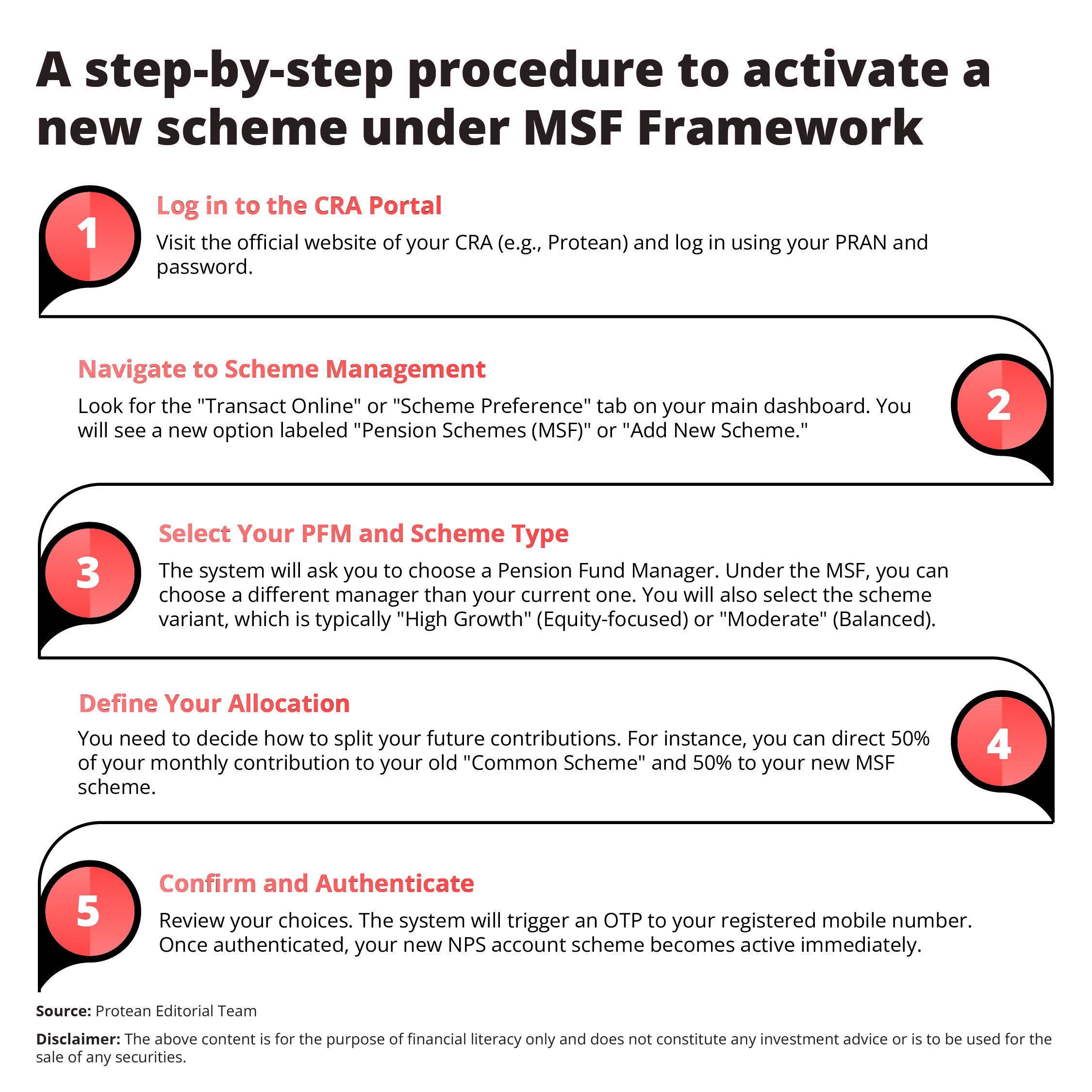

How to Set-up Multiple Schemes with One PRAN

A multiple NPS account portfolio can be set-up using a digital-first process. You do not need to fill out physical forms if you are already an active subscriber. You can manage the entire process through your Central Recordkeeping Agency (CRA) portal, such as Protean eGov Technologies Ltd.

If you are a new investor, you can choose this structure right when you open an NPS account for the first time by selecting multiple schemes during registration.

Strategic Benefits of Portfolio Diversification

The primary advantage of the Multiple Scheme Framework is the ability to tailor your investments to specific financial objectives. It has transformed NPS into a comprehensive wealth-management tool.

1. The "Core and Satellite" Strategy

Now, you can split your NPS investments into two distinct buckets. Firstly, you can maintain a "Core" portfolio in a standard, moderate-risk scheme (like the Auto Choice or a balanced Active Choice) to ensure the safety of your primary retirement corpus. Simultaneously, you can open a "Satellite" scheme under the MSF that is aggressive and high-risk. This satellite portfolio can target higher returns. It can do this without exposing your entire life savings to market volatility.

2. Access to 100% Equity

One of the most important features of the Multiple Scheme Framework is the introduction of high-risk variants. This variation allows up to 100% allocation to equity.

So, if you are a young investor with a high risk appetite, you can use the MSF to create a specific NPS account scheme dedicated entirely to equity. Thus, you can capture maximum market upside during your early earning years.

3. Manager Diversification

With MSF, under your single NPS account/PRAN, you can have one scheme managed by one PFM for equity performance and another by a different PFM for debt stability.

MSF - Important Considerations and Limitations

The Multiple Scheme Framework offers immense freedom. However, it is not without its rules. The PFRDA has implemented specific guardrails to ensure financial discipline.

- Vesting Period: New schemes opened under the MSF can come with a mandatory "vesting" or lock-in period, often set at 15 years or until the age of 60.

- Switching Restrictions: You cannot freely switch funds between two MSF schemes during the vesting period. However, you are generally allowed to switch from a new MSF scheme back to the traditional "Common Scheme" if needed.

- Higher Costs: Schemes under the MSF may have a slightly higher expense ratio cap (up to 0.30%) compared to the legacy schemes. You need to factor this in when building your portfolio.

- Eligibility: Currently, the Multiple Scheme Framework is available mainly to non-government sector subscribers including 'All Citizen' and 'Corporate' sectors. Government employees generally follow different rules and may have limited applicability of MSF, often restricted to Tier II accounts.

Conclusion

The Multiple Scheme Framework transforms the NPS into a dynamic, multi-faceted investment platform. With this, you can build a multiple NPS account structure that mirrors your unique financial personality.

You can also balance safety with aggression, and stability with growth, all under the umbrella of a single PRAN. So, if you have yet to open an NPS account, you can start with a PRAN and immediately select MSF schemes for a diversified structure to give your retirement planning a head start.

For existing subscribers, the MSF can be a fresh opportunity to optimise your portfolio without losing the benefits of your vintage investments.

Frequently Asked Questions

Q1: Can I open a second PRAN to get a multiple NPS account?

No. An individual can hold only one PRAN. The Multiple Scheme Framework allows you to hold multiple schemes within that single PRAN, effectively acting as multiple portfolios. You strictly cannot have two separate PRAN cards.

Q2: Is the 100% equity option available to everyone under MSF?

The 100% equity option is specific to the "High Growth" schemes launched under the MSF. It is available to non-government subscribers. You must actively select a high-risk MSF scheme to avail of this, as standard schemes still cap equity at 75%.

Q3: Does opening a second scheme increase my annual maintenance charges?

You do not pay a separate account opening fee, but each scheme under the multiple NPS account structure has its own fund management charges. You will pay these charges on the Assets Under Management (AUM) held in each specific scheme.

Q4: Can I use the MSF for my Tier II account?

Yes. The Multiple Scheme Framework is available for both Tier I and Tier II accounts. This allows you to use your Tier II account (which has no lock-in) for shorter-term goals with diversified strategies, functioning very much like a flexible mutual fund portfolio.