Confused among various tax saving investments?

Here’s a hack for making the most out of your tax benefits from investing!

Check NPS! The most looked after investment that can help you combine retirement planning with tax benefits.

Let us learn more about NPS contribution, and its efficiency among other retirement planning and tax saving investments.

Tax Saving Sections in India

The Indian Income Tax Act has several sections for taxpayers to reduce their liability legally. Let us look at them in detail:

Section 80C

Under the Old Tax Regime, Section 80C is the go-to destination for most taxpayers looking to save on taxes. Here, you can get a maximum deduction of ₹1.5 lakh from your taxable income for specified investments and expenses. The popular instruments covered under this section include the following:

- Employee Provident Fund (EPF)

- Life Insurance Premiums

- Public Provident Fund (PPF)

- Equity-Linked Savings Schemes (ELSS)

- Principal repayment of home loans

- Tuition fees for children

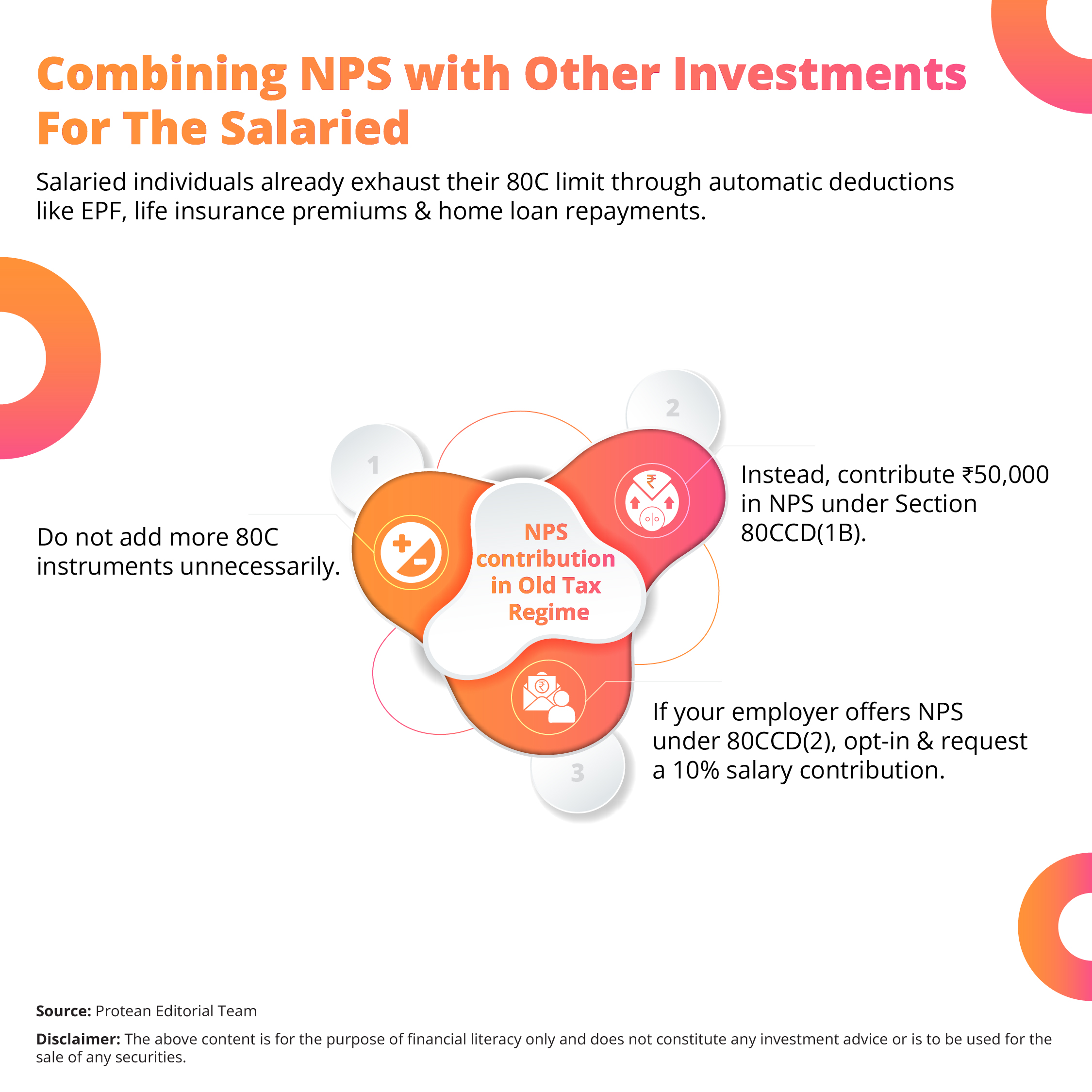

However, the ₹1.5 lakh cap can fill up quickly. This is especially true for salaried individuals with mandatory EPF deductions. Here’s where NPS can help!

Section 80CCD

The NPS has three distinct tax deduction routes under Section 80CCD:

- 80CCD(1): Employee/self-contribution falls under the overall ₹1.5 lakh limit of Section 80C.

- 80CCD(1B): Additional self-contribution up to ₹50,000 extra deduction, over and above the 80C limit.

- 80CCD(2): Employer’s contribution available to salaried individuals, with no monetary cap, but limited to 10% of salary (basic + DA) which is 14% in case of the Central Government Employees.

Learn more about optimising tax benefits with NPS here.

Role of NPS in Tax-Saving

NPS can offer tax benefits outside this limitation of ₹1.5 lakh. These are as follows:

Advantage 1: The ₹50,000 Bonus under 80CCD(1B)

You can invest an additional ₹50,000 as an NPS contribution. This is only for tax benefit, over and above the ₹1.5 lakh limit of 80C. This can effectively raise your total tax-saving potential to ₹2 lakh per year.

For someone in the 30% tax bracket, this can mean an additional saving of ₹15,600 per year (including cess), a benefit often overlooked.

Advantage 2: Employer Contribution under 80CCD(2)

Salaried individuals can maximise tax deductions further if their employer contributes to their NPS account. Under Section 80CCD(2), this contribution up to 10% of the employees (14% for Central Government employees) basic salary plus DA, is fully deductible from taxable income and does not interfere with 80C or 80CCD(1B) deductions.

High-income earners can save substantial tax through this route, especially in companies that have introduced corporate NPS as part of employee benefits.

Beyond tax, NPS does serve as a disciplined retirement planning vehicle.

How to Combine Investments with NPS for Maximum Benefit

Here is how you can combine your NPS tax saving investments with other investment products optimally:

This could unlock unlimited additional deductions without any action on your part.

Thus, a salaried person could save tax on up to ₹2.5 -₹3 lakh, combining 80C, 80CCD(1B), and 80CCD(2).

Note: Under the new tax regime (from FY 2025-26), this deduction is not available; only employer contributions under 80CCD(2) are allowed.

Check this link to learn about retirement planning through NPS contribution.

Self-Employed Individuals

Self-employed professionals and business owners have a different situation. They do not have EPF contributions, so their 80C limit might remain underutilised.

Suggested steps

- Utilise the full ₹1.5 lakh under 80C through ELSS (for equity exposure), life insurance, or PPF (for stable returns).

- Additionally, contribute ₹50,000 to NPS under 80CCD(1B) for bonus deduction (not available under new tax regime).

- Though 80CCD(2) is not applicable to the self-employed, the combination of 80C and 80CCD(1B) still offers a powerful ₹2 lakh deduction potential.

Prioritisation & Allocation Strategy

To maximise both tax benefits and investment returns, you can consider this order of allocation:

- Employer NPS Contribution (salaried): Auto deduction under 80CCD(2) to maximise up to 10% of salary.

- ₹1.5 lakh under Section 80C: Starting with mandatory deductions (like EPF), then adding PPF, ELSS, or home loan principal repayment to fill the gap.

- ₹50,000 under Section 80CCD(1B): Voluntary NPS contribution to claim exclusive benefit.

Avoiding Overlapping Benefits

A common mistake is to invest heavily in overlapping products without realising they share the same deduction limits.

Here’s an example:

- Investing in PPF, ELSS, and life insurance while already hitting ₹1.5 lakh in EPF.

- Missing out on the exclusive ₹50,000 80CCD(1B) benefit by not contributing to NPS.

Holistic tax planning means viewing these sections as interconnected gears, not separate levers.

Conclusion

For tax planning, the difference between saving tax and maximising tax efficiency lies in integration.

Whether you are a salaried employee with EPF deductions or a self-employed professional looking for tax relief, NPS can offer a unique value proposition, dual benefits of immediate tax reduction and future financial security.

Finally, strategic tax planning is not about choosing one instrument over another. Instead, it is about orchestrating your investments to build both wealth and peace of mind.

Optimise your tax benefits with NPS investing now! Click here to make your contribution.