The National Pension System (NPS) is a voluntary, long-term retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It is designed to provide financial security to individuals post-retirement while offering substantial tax benefits. Over the years, NPS has emerged as an effective tool for both corporates and employees, allowing them to optimise tax liabilities and build wealth in a disciplined manner.

| Don’t wait until the last minute for NPS registration! Register now and start investing with NPS as you save taxes |

Given the introduction of the New Tax Regime, its impact on NPS contributions and benefits can be assessed in the following manner:

1. Tax Benefits for Corporates and Employees Under Old & New Tax Regimes

One of the major advantages of NPS is its tax efficiency. Both employers and employees can claim tax benefits under different sections of the Income Tax Act, 1961.

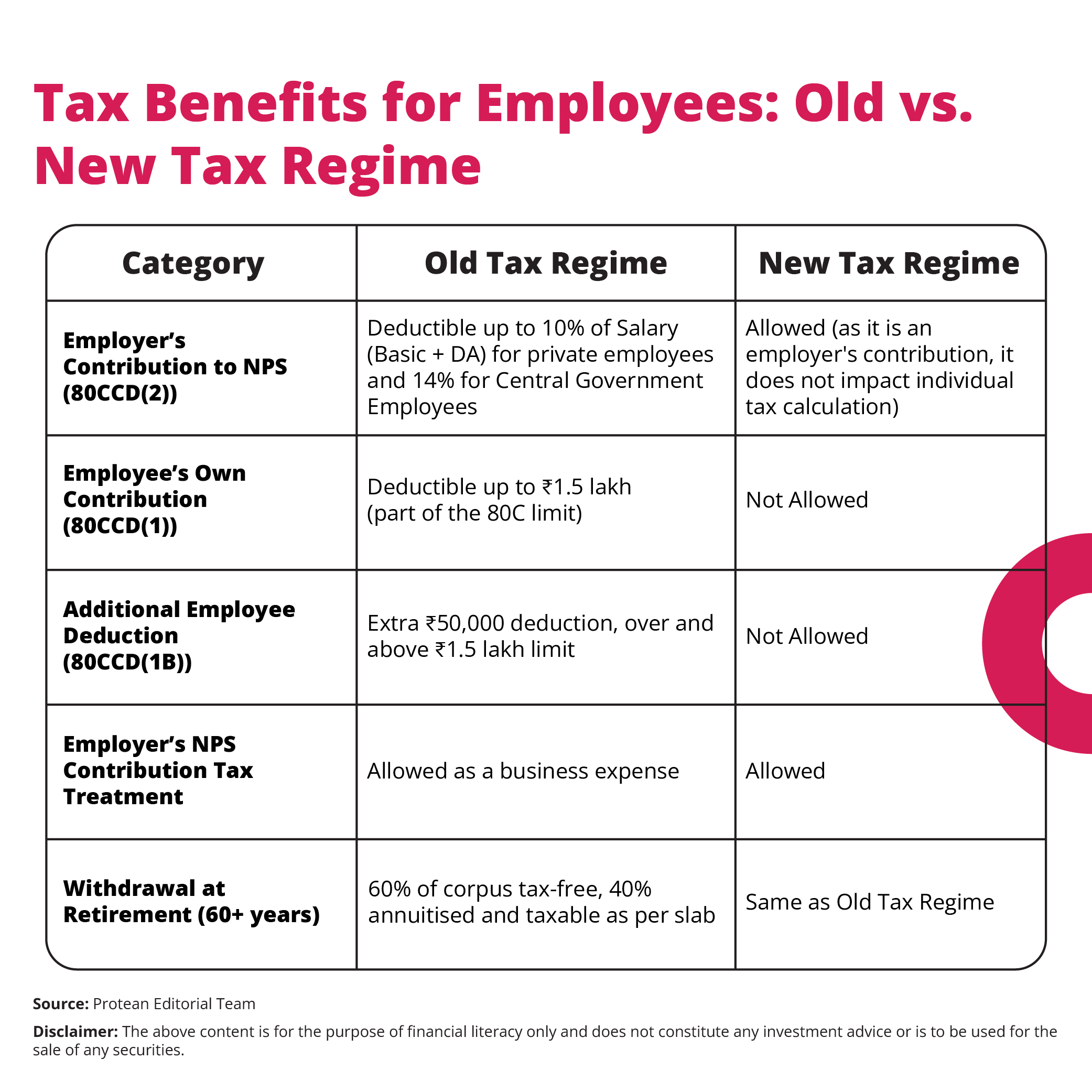

(A) Tax Benefits for Employers

- Employer’s Contribution as a Business Expense

- Under Section 36(1)(iv)(a), corporate entities can claim their contributions to NPS as a business expense, reducing their taxable income.

- The permissible limit is 10% of an employee’s salary (Basic + DA) for private-sector companies and 14% of Central Government employees.

- Reduced Corporate Tax Liability

- By structuring employee benefits through NPS rather than taxable bonuses, employers can optimise their financial planning while ensuring greater employee retention.

- CSR and Employee Welfare

- Contributions to NPS align with corporate employee welfare policies and indirectly contribute to Corporate Social Responsibility (CSR) goals.

(B) Tax Benefits for Employees: Old vs. New Tax Regime

| Did you know that you can secure your child’s retirement with NPS Vatsalya? Read about it here. |

2. NPS as a Tool for Wealth Creation

NPS offers structured retirement planning with market-linked growth. The investment is managed by PFRDA-regulated pension fund managers who allocate funds across different asset classes:

- Equity (E): The equity allocation has the potential of higher risk and higher return.

- Corporate Bonds (C): The allocation towards corporate bonds has potential for providing moderate returns with lower risk.

- Government Securities (G): Choice of government securities allocates the funds towards stable and low-risk investments.

- Alternative Assets (A): NPS allocation also provides opportunity Limited exposure to REITs and infrastructure funds is possible.

| Before you start your NPS application, ensure that you have a PAN. Apply for PAN here. |

Participants can choose between:

- Active Choice: Self-determined asset allocation.

- Auto Choice: Age-based asset allocation (higher equity exposure in early years, shifting to lower risk near retirement).

| Know about the process and benefits of NPS? Already a subscriber? Click on this link now to invest in NPS for the financial year. |

(A) Power of Compounding and Low-Cost Structure

- NPS is one of the lowest-cost retirement investment options, with fund management fees ranging from 0.01% to 0.09%.

- Since investments are locked in until 60 years of age, the power of compounding ensures significant corpus growth.

(B) Withdrawal and Exit Flexibility

- At Retirement (60 Years & Above):

- 60% of the accumulated corpus is tax-free.

- 40% must be used to buy an annuity, which is taxable as per the employee’s income tax slab.

- Partial Withdrawals Before Retirement:

- Allowed up to 25% of own contributions for specified needs (medical treatment, home purchase, children’s education) after three years.

- These withdrawals are tax-free.

| NPS reached millions and millions more in 2024! Know about all NPS achievements in 2024 here. |

Case Study: NeoTech Solutions and NPS Implementation

Company: NeoTech Solutions Pvt. Ltd.

NeoTech Solutions, a Mumbai-based IT services company, wanted to optimise tax savings while enhancing employee welfare. Before implementing NPS, employees used to receive performance bonuses, which were fully taxable. To create a more tax-efficient system, NeoTech introduced NPS contributions.

Scenario 1: Without NPS

- Annual salary: ₹12,00,000

Performance bonus: Fully taxable

- Employees had no structured retirement savings beyond EPF and PPF.

Scenario 2: With NPS Integration

Case 1: Employee A (Old Tax Regime - Utilising NPS Deductions)

Employee A has opted for the Old Tax Regime, which allows for various deductions under the Income Tax Act, including contributions to the National Pension System (NPS). Here’s a detailed breakdown of how these deductions impact her taxable income and tax savings:

Employee's Own NPS Contribution:

i. Employee A contributes ₹1,50,000 towards their NPS account, which qualifies for a deduction under Section 80CCD(1).

ii. The deduction is subject to the overall limit of ₹1,50,000 under Section 80C.

Additional NPS Deduction:

An extra deduction of ₹50,000 is claimed under Section 80CCD(1B).

This deduction is available exclusively for NPS contributions and is over and above the ₹1,50,000 limit of Section 80C.

Employer's NPS Contribution:

The employer contributes 10% of Basic Salary + Dearness Allowance (DA) to Employee A’s NPS account.

This contribution is exempt from tax under Section 80CCD(2), providing additional tax benefits.

Total Taxable Income After Deductions:

After applying the deductions, Employee A’s final taxable income is ₹10,00,000.

Tax Savings Calculation:

Since Employee A falls under the 30% tax slab, the tax saved due to these deductions is:

₹2,00,000 × 30% = ₹60,000.

By leveraging NPS deductions under the Old Tax Regime, Employee A effectively reduces their taxable income and enjoys significant tax savings while also securing their retirement funds.

Case 2: Employee B (New Tax Regime - No NPS Deductions

Under the new tax regime, Employee B does not receive any tax deductions for their own NPS contributions. However, the employer’s contribution remains tax-free.

While the tax is calculated at a lower slab rate, the absence of exemptions makes this regime less beneficial for individuals who would otherwise claim significant deductions under the old regime.

Outcome for NeoTech Solutions

- For Employees: Structured retirement planning and reduced taxable income (Old Regime).

- For the Company: Reduced corporate tax burden and improved employee retention.

Please note that the calculations made above are only for illustrative purposes. Actual calculations may differ based on different other provisions of the tax applicability, exemptions and deductions.

| Learn about individual and company subscription documents and registration here. Register now! |

4. Why Should Corporates Adopt NPS?

(A) Enhancing Employee Retention & Satisfaction

- Acts as a long-term incentive, ensuring financial security.

- Reduces attrition by providing attractive post-retirement benefits.

(B) Tax-Efficient Compensation Planning

- Companies can save on taxes while offering better salary structures.

- Alternative to traditional Employee Provident Fund (EPF) or gratuity.

(C) Competitive Edge in Talent Acquisition

- Offering NPS benefits can make corporate salary packages more attractive.

- Helps attract top-tier talent, especially in industries with high competition.

| Become a corporate subscriber now! Learn about the documents and details here. |

(D) Points to be noted:

- New Tax Regime: Only employer contributions to employee NPS accounts are eligible for tax exemption in the new tax regime.

- Simultaneous Deductions: Employees can claim deductions under both Section 80CCD(1B) and Section 80CCD(2) simultaneously, ensuring that the total deductions do not exceed the specified limits for each section.

- Premature Exit: Employees can use the "Premature exit" facility to withdraw their accumulated corpus, subject to the scheme's terms and conditions.

- Conversion to Corporate NPS: To convert an individual NPS account to a corporate NPS account, employees need to submit Form-ISS-1 to their Point of Presence (PoP) service provider.

| These were the details of NPS as a medium of tax saving and wealth creation. So, what are you waiting for? Open an NPS account with Protean now! |

Conclusion

The National Pension System (NPS) serves as a win-win solution for both corporates and employees, ensuring tax efficiency, long-term wealth creation, and retirement security. While the Old Tax Regime offers significant deductions, the New Tax Regime still allows employer contributions to be tax-free. Businesses can not only reduce tax liabilities but also position themselves as employee-centric organisations that prioritise financial well-being and stability by adopting NPS. Given its low cost, professional fund management, and tax-efficient structure, NPS can be one of the better long-term financial planning tools for corporates in India.

- Story by Bruhadeeswaran R.

Bruhadeeswaran has 15+ years of experience as a content strategist, communication, and editorial professional. Currently, he is leading an innovative content development process, translating complex B2B products into engaging, user-friendly narratives.