The National Pension System (NPS) has undergone considerable regulatory transformations in nearly two decades. The latest amendments (in late 2025) have made NPS withdrawal rules, NPS exit rules, and investment flexibility far more attractive for modern investors.

Three core changes have redefined how retirement savings are accumulated and accessed.

- A shift from the traditional “60:40” annuity requirement to an “80:20” structure

- Introduction of a MSF (Multiple Scheme Framework) with up to 100% equity exposure

- Extension of the maximum exit age to 85.

The cumulative effect of these reforms has positioned NPS as a dynamic long-term investment vehicle suitable for diversified portfolios.

The 100% Equity Shift

The asset allocation reforms under the MSF is one of the most talked about ones.

Earlier, non-government subscribers’ equity exposure was capped at 75%. This was applicable even under the active choice option. This had limited the returns potential for younger investors with long investment horizons, despite adding stability to NPS investing.

With the introduction of MSF, eligible subscribers can invest up to 100% in equity through fresh contributions. Under this framework, schemes are offered in clearly defined risk categories such as high, moderate, and conservative.

Thus, investors can align their retirement savings with their individual risk appetite and market expectations.

Existing Common Schemes in NPS continue with the 75% equity cap. But the new framework provides an additional growth-focused option. The MSF schemes are structured under the subscriber’s PAN. Thus, investors can access multiple pension fund managers within a single retirement account.

Overall, this reform has brought NPS closer to growth-oriented investment strategies.

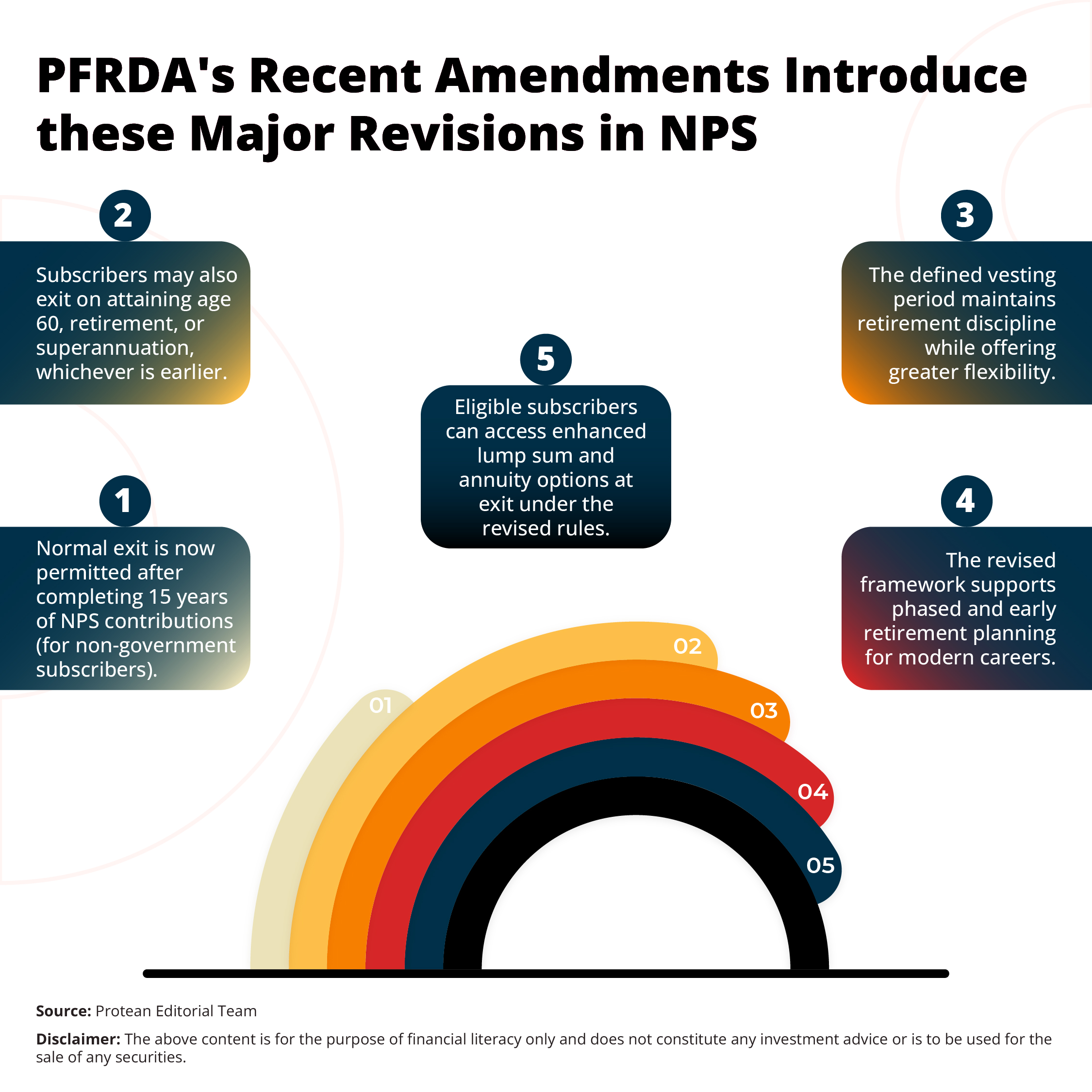

New NPS Withdrawal Rules

Earlier, NPS withdrawal rules were structured to ensure a balance between immediate access to savings and long-term pension security.

For non-government subscribers, a maximum 60% of the accumulated pension wealth could be withdrawn at exit. The remaining 40% had to be mandatorily utilised for purchasing an annuity to provide regular retirement income.

There are certain provisions of the amended regulations for eligible non-government subscribers.

- Non-government subscribers with corpus over ₹12 lakh can withdraw up to 80% at normal exit, with at least 20% annuitised. For ₹8-12 lakh corpus, up to ₹6 lakh lump sum withdrawal is allowed, with remainder via annuity or systematic withdrawals over 6 years minimum.

- Total pension wealth up to ₹8 lakh are permitted full withdrawal without annuity purchase.

- Investors can have four withdrawals before the age of 60 at prescribed intervals.

These changes have added greater flexibility while retaining the pension-oriented character of NPS.

Exit Age Extended to 85

The amendment has extended the maximum NPS exit age from 70/75 years to 85 years for both non-government and government subscribers.

With this extension, subscribers can remain invested for a longer time. They also have the potential to enhance their retirement corpus to a much larger extent before withdrawal or annuitisation.

From a retirement planning perspective, this extension provides several benefits.

- Extended Compounding Time - Longer time within the market can enhance returns. This is especially applicable for equity-oriented MSF schemes.

- Flexibility at Older Ages - Subscribers who do not need immediate retirement funds can defer exit. Thus, they can benefit from continued growth or structured withdrawals tailored to longevity needs.

Now, NPS can effectively accommodate a broader range of retirement timelines, recognising that individuals may choose flexible exit points based on personal and market conditions.

NPS Exit Rules: Early Retirement is Finally a Reality

NPS exit provisions continue to encourage long-term retirement savings while offering improved flexibility.

Conclusion

The 2025 reforms to the NPS framework represent a dynamic shift in how retirement planning is structured in India. NPS withdrawal rules have been eased, while 100% equity investment options have been introduced separately through the Multiple Scheme Framework. The PFRDA has thus made NPS more flexible, growth-oriented, and aligned with modern financial goals.

Investors, especially in the non-government sector can benefit from these changes that provide a blend of retirement discipline and investment freedom. These changes have enhanced NPS’s appeal as a comprehensive retirement solution that can now compete with other long-term products such as mutual funds and provident funds.

Frequently Asked Questions (FAQs)

Q1. What is the new equity allocation rule in NPS?

Under the Multiple Scheme Framework (MSF), subscribers can choose schemes with up to 100 per cent equity exposure in the high-risk variant. This offers a higher equity exposure compared to the previous 75% cap in Common Schemes.

Q2. What do the new withdrawal rules allow?

Non-government NPS subscribers can withdraw up to 80 per cent of their corpus at exit, while the remaining 20 per cent must be used to buy an annuity, and those with savings up to ₹8 lakh can withdraw the full amount as a lump sum.

Q3. Can I exit NPS early?

Yes. Normal exit is possible after 15 years of contributions or at age 60, without mandatory wait until 60 in all cases.

Q4. How does the exit age change benefit me?

The maximum age to remain invested has increased to 85 years, allowing for extended compounding and flexible retirement planning.

Q5. Do these changes apply to government employees?

Yes, though government subscribers continue to have a 60:40 withdrawal-to-annuity structure, other enhancements like the extended exit age also apply.