The National Pension System (NPS) is one of the most widely used retirement savings plans in India. It is known for its dual benefits: creating a long-term retirement corpus and offering tax incentives. However, with the introduction of the new tax regime, some aspects of investing in NPS have changed. Many investors now want to understand how withdrawals are treated, what limits apply, and how taxation is calculated.

This article explains the NPS withdrawal rules under the new regime, covering lump sum payouts, annuity requirements, and deferment options.

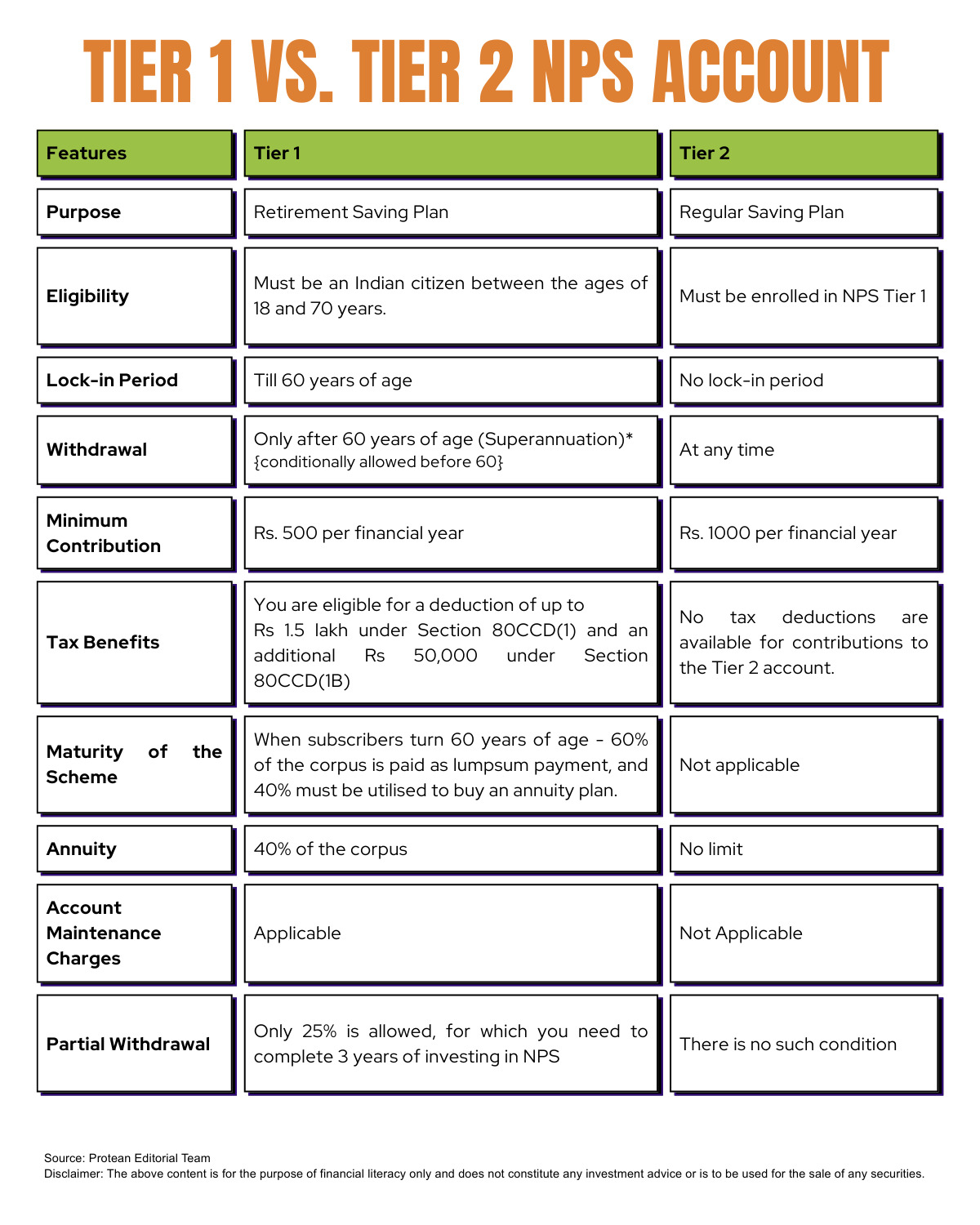

What are the Types of NPS Accounts?

NPS provides two account structures, each with different rules:

- Tier-I Account (mandatory)

- Default retirement account.

- Contributions build the retirement corpus.

- Withdrawals are subject to strict conditions.

- At retirement, a pension is paid through an Annuity Service Provider (ASP).

- Tier-II Account (optional)

- Functions more like a savings account.

- Flexible withdrawals allowed.

- No additional tax benefits.

- Requires an active Tier-I account for activation.

In both accounts, investors can gain exposure to equity, corporate bonds, government securities, and alternative investment funds. While Tier-I limits equity exposure to 75%, Tier-II allows up to 100% allocation.

| Also Read: NPS Wealth Planning |

Understanding the One-Way Transfer Rule

NPS follows a one-way switch mechanism. Investors can move funds from Tier-II to Tier-I, but not the other way round. Direct transfers from Tier-I to a bank account are allowed only under withdrawal conditions.

What are the Tax Benefits in the National Pension System?

Tax treatment differs between the old and new regimes:

- Under the Old Tax Regime (OTR), subscribers can claim additional deductions of up to ₹50,000 per year under section 80CCD (1B).

- Under the New Tax Regime (NTR), personal contributions to NPS are not eligible for tax deduction. However, if an employer contributes, employees can still claim deductions under section 80CCD (2) up to 14 per cent of basic salary.

This distinction makes employer-driven contributions more significant under NTR.

| Also Read: NPS for Employees |

NPS Withdrawal Rules and Conditions

Subscribers cannot access the entire balance freely at retirement. Withdrawals are regulated to ensure a portion of the funds is used for pension income.

- Typically, 60 per cent of the corpus can be withdrawn as a lump sum.

- The remaining 40 per cent must be used to purchase an annuity plan that guarantees a pension.

- If the corpus is small (below a threshold), the annuity requirement can be waived, and the entire amount may be withdrawn.

What are the Types of Withdrawals?

NPS allows three kinds of withdrawals depending on the situation:

1. Partial Withdrawal

- Allowed after 3 years of account opening.

- Maximum 25 per cent of personal contributions.

- Only three partial withdrawals are permitted during the entire tenure.

- Reasons include higher education, marriage, medical needs, property purchase, or starting a business.

- A gap of 5 years is required between withdrawals (An exception is made for medical emergencies, where the gap may not hold.)

Example: If an investor contributed ₹2,50,000 over five years, only 25 per cent of that contribution, ₹62,500, can be withdrawn, regardless of the total corpus value.

2. Premature Withdrawal

- Permitted if the account is closed before age 60.

- Allowed only after 5 years of account opening.

- In such cases, only 20 per cent can be withdrawn as a lump sum, while 80 per cent must go towards annuity purchase.

- If the corpus is below a specified threshold, the annuity is optional.

3. Withdrawal on Death of Subscriber

- If a private sector subscriber dies, the entire corpus becomes payable to the nominee or legal heir.

- They may choose to receive it as a lump sum or opt for an annuity, though an annuity is not mandatory.

- For government employees, dependents must purchase an annuity with the balance.

Option to Defer Payments

Subscribers can postpone their withdrawal instead of taking the entire lump sum at retirement.

- The 60 per cent withdrawable portion can be taken in instalments.

- Pension purchase (40 per cent annuity) can also be deferred.

- The deferment can extend investment until the age of 75.

This option is helpful for those who wish to stay invested longer and continue earning market-linked returns.

| Also Read: Calculate Your NPS |

Conclusion

The NPS withdrawal rules under the new tax regime highlight the importance of balancing immediate financial needs with future pension income. While tax benefits are less under NTR, the scheme continues to be a valuable retirement planning tool due to its disciplined structure, flexible withdrawal options, and guaranteed annuity component.

For Indian investors, understanding these rules is the key to making informed decisions about contributions, retirement age planning, and long-term income stability.

Frequently Asked Questions

Q1: How much can I withdraw from my NPS corpus at retirement?

Up to 60% can be taken as a lump sum, while 40% must be used to buy an annuity.

Q2: Can I withdraw before 60 years of age?

Yes, but only after 5 years of account opening. In such cases, 20% is allowed as a lump sum, and 80% must go into an annuity.

Q3: What are the rules for partial withdrawals?

You can make up to three partial withdrawals in your lifetime, each limited to 25% of your own contributions, and with a gap of 5 years between them.

Q4: What happens to the NPS corpus in case of the death of the subscriber?

For private sector subscribers, the entire balance is paid to the nominee or heir. For government subscribers, dependents must use the funds to buy an annuity.

Q5: Can withdrawals be deferred beyond retirement age?

Yes, subscribers can defer lump sum withdrawal and pension purchase until age 75, either partially or fully.