As parents or guardians, are you looking for a perfect Children's Day gift? You may consider adding an NPS Vatsalya investment to your checklist. Here’s why.

We might think toys and gadgets are popular, but they offer temporary joy. For a truly lasting and meaningful gift, one can look for an investment that can grow with your child. We can look for something that can provide a foundation for their future. This is where NPS Vatsalya comes in. NPS Vatsalya is a scheme designed to offer long-term financial security for your children under the guidelines of PFRDA.

Let us look at the basics and nitty gritty details of NPS Vatsalya.

What is NPS Vatsalya and What Makes it Unique?

The NPS Vatsalya scheme is a specially designed contribution-based pension scheme exclusively for minors. The PFRDA (Pension Fund Regulatory and Development Authority) regulates this scheme and it operates under the umbrella of the NPS (National Pension System).

This scheme is a forward-thinking initiative aligned with the national vision of building a financially secure and developed India by 2047. The primary objective is to empower children financially and inculcate a habit of saving from a young age. Thus, it is aiming to help create a future pensioned society.

This voluntary scheme is open to any minor Indian citizen. The account is an individual pension account and is opened in the minor's name. It draws its features from the robust NPS Tier-1 structure. However, it is custom tailored for a minor subscriber.

How Does NPS Vatsalya Work?

The NPS Vatsalya scheme is designed for ease of use by guardians/parents. The details are represented below.

Account Opening

The account can be opened by a parent or a legal guardian. However, the account would be in the name of the minor. The minor would always be the sole beneficiary of the NPS Vatsalya account.

Guardian's Role

The guardian would operate the account for the exclusive benefit of the child until the child reaches the age of 18 years.

KYC Requirements

The KYC (Know Your Customer) norms apply to the guardian who opens the account. A copy of the court order is a mandatory document along with their standard KYC (if the legal guardian is court-appointed).

Documentation for the Minor

You need to submit the minor's proof of date of birth. This can be a documents like a birth certificate, school leaving certificate, marksheet from a recognised board, or the minor's passport.

Bank Account

Bank account details of the minor (or a joint account) are not mandatory for opening the account. However the bank account details are required if there is any partial withdrawal or final exit.

Unique PRAN

After successfully completing the registration, a unique PRAN (Permanent Retirement Account Number) is issued in the name of the minor subscriber. This PRAN stays with the account holder (who is currently a minor) for life.

How Do Contributions and Investments in NPS Vatsalya Work?

The NPS Vatsalya contribution structure is highly flexible.

- Initial Contribution - Here, a minimum of ₹1,000 is required to open the account.

- Annual Contribution - At least ₹1,000 needs to be contributed each financial year.

- Maximum Contribution: There is no upper limit on the maximum contribution. This gives you the freedom to invest as per your financial goals for your child.

The parent/guardian can also flexibly choose the investment strategy. Just like the NPS All Citizen Model, you can select the PFM (Pension Fund Manager) and/or decide on the investment mix (between Active Choice and Auto Choice) to align with your risk appetite and long-term goals.

The Unmatched Advantages: NPS Vatsalya Benefits

The NPS Vatsalya benefits are a unique combination of long-term growth, flexibility, and security.

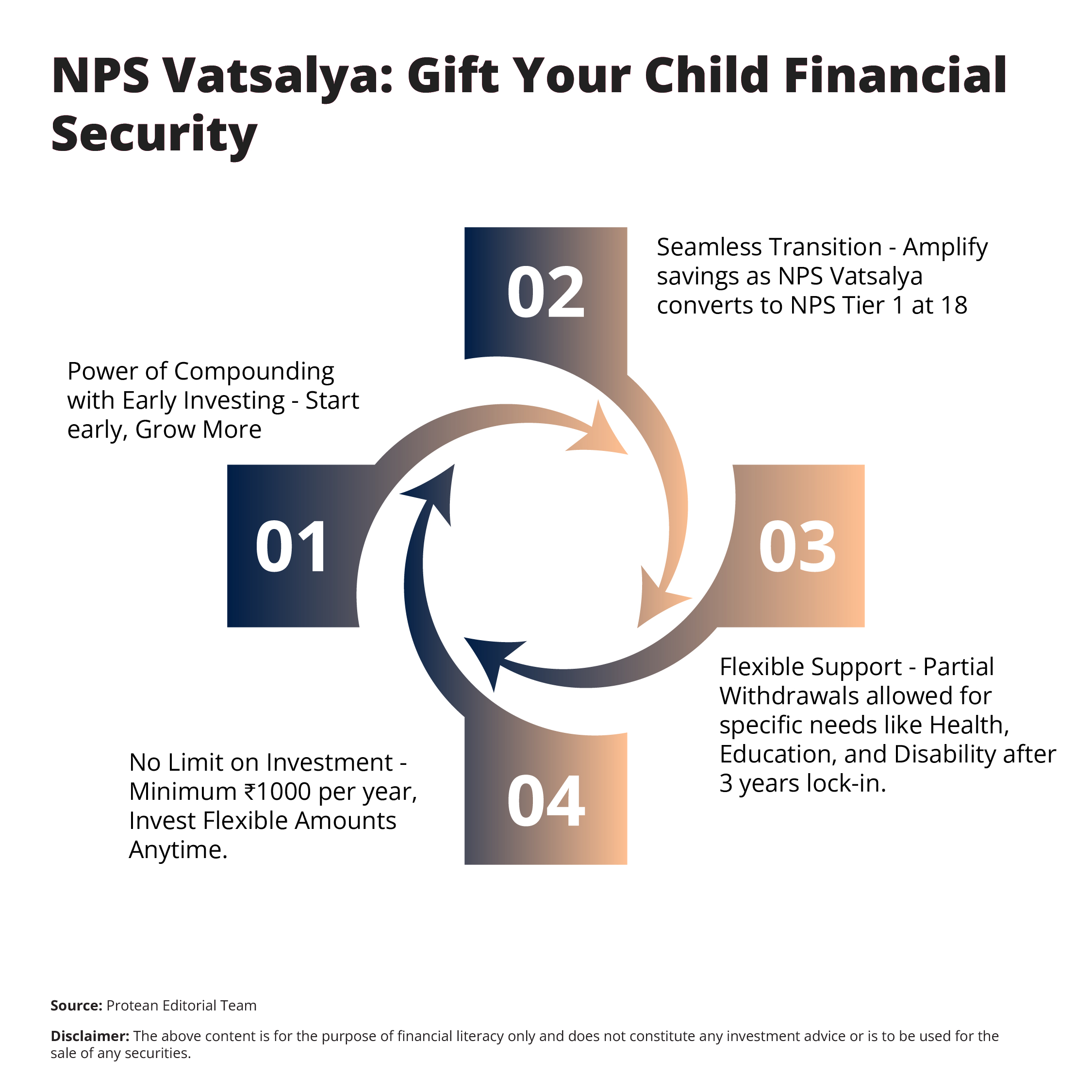

The Power of Compounding

The magic of compounding works well in the longer investment horizon. Starting an investment for a child, even a newborn, can provide a runway of 18 years (and beyond) for the money to grow. When compounded over decades, the market-linked returns can build a strong corpus that can far outpace traditional savings.

Flexibility for Your Child's Needs (Partial Withdrawal)

Your NPS Vatsalya investment money is not locked away completely. This is a standout NPS Vatsalya benefit. You can also make partial withdrawals to support your child's journey. You can withdraw up to 25% of the subscriber's total contribution (excluding returns) for specific, needs mentioned below:

- The child's higher education.

- Treatment of specified illnesses.

- In case of disability (more than 75%).

This facility is available after the account has been active for a minimum of three years. It can be used a maximum of three times before the child turns 18.

Seamless Transition to Adulthood

Another major NPS Vatsalya benefit is its flawless continuity into adulthood. When the subscriber turns 18, the account does not close or mature abruptly. It shifts into an NPS Tier-1 Account automatically under the All Citizen Model.

No Cap on Investment

With NPS Vatsalya you can contribute as much as you want for your child’s future. This can be better for parents who wish to build a larger corpus for their child's future. It can also be a blessing for parents aiming for their child's education abroad, starting a business, or as a retirement head-start.

The Journey to Adulthood: Transition and Exit Rules

The NPS Vatsalya scheme is designed to mature with your child. Here is what happens to the child’s account at 18 years of age.

- The account automatically converts to a standard NPS Tier-1 account.

- The subscriber, now an adult, must complete a fresh KYC process within three months of turning 18 years.

- Further contributions to the account are allowed only after the subscriber completes the fresh KYC post turning 18.

- From this point on, all features, benefits, and exit norms of the NPS Tier-1 All Citizen Model become applicable.

Exit Options After Turning 18

If the subscriber (now an adult) decides to exit the scheme upon turning 18 there are multiple options available.

- Annuity Purchase - At least 80% of the total accumulated pension wealth must be used to purchase an annuity (a regular pension).

- Lump Sum Withdrawal - You can withdraw the remaining balance (up to 20%) as a lump sum.

- Special Exception - IIf the total accumulated corpus in the account is ₹2,50,000 or less, the subscriber would have an option to withdraw the entire amount as a lump sum.

The following contingency provisions apply:

- In case of the minor's death the entire accumulated pension wealth is paid to the registered guardian.

- In case of the guardian's death, a new guardian needs to be registered on behalf of the minor by submitting the required KYC documents to continue the account.

Conclusion: The Gift of a Head Start

This Children's Day, you, as parents/guardians have the opportunity to give a gift that truly lasts a lifetime. The NPS Vatsalya scheme is a promise of empowerment. Here, you are building a secure launchpad for your child's retirement, with the added flexibility of partial withdrawals for education and critical needs. The NPS Vatsalya benefits of compounding, flexibility, and a seamless transition have made it one of the most powerful and thoughtful gifts you can give to your children. So, why wait, make your NPS Vatsalya contribution now!