Did you know: NPS Vatsalya can be a thoughtful long-term gift you can give to your children on their birthday.

Yes, the Government of India (GoI) introduced the NPS Vatsalya scheme to address the special need for early pension planning for the younger generation.

This GoI-backed pension initiative is specifically designed for minors. NPS Vatsalya ensures a strong financial foundation even before your child begins their careers.

Furthermore, the cost of education and living is rising steeply. So, a traditional approach like bank savings is no longer sufficient in the modern economic landscape. With the NPS ecosystem, you can invest in a robust, regulated, and transparent platform for your child’s future.

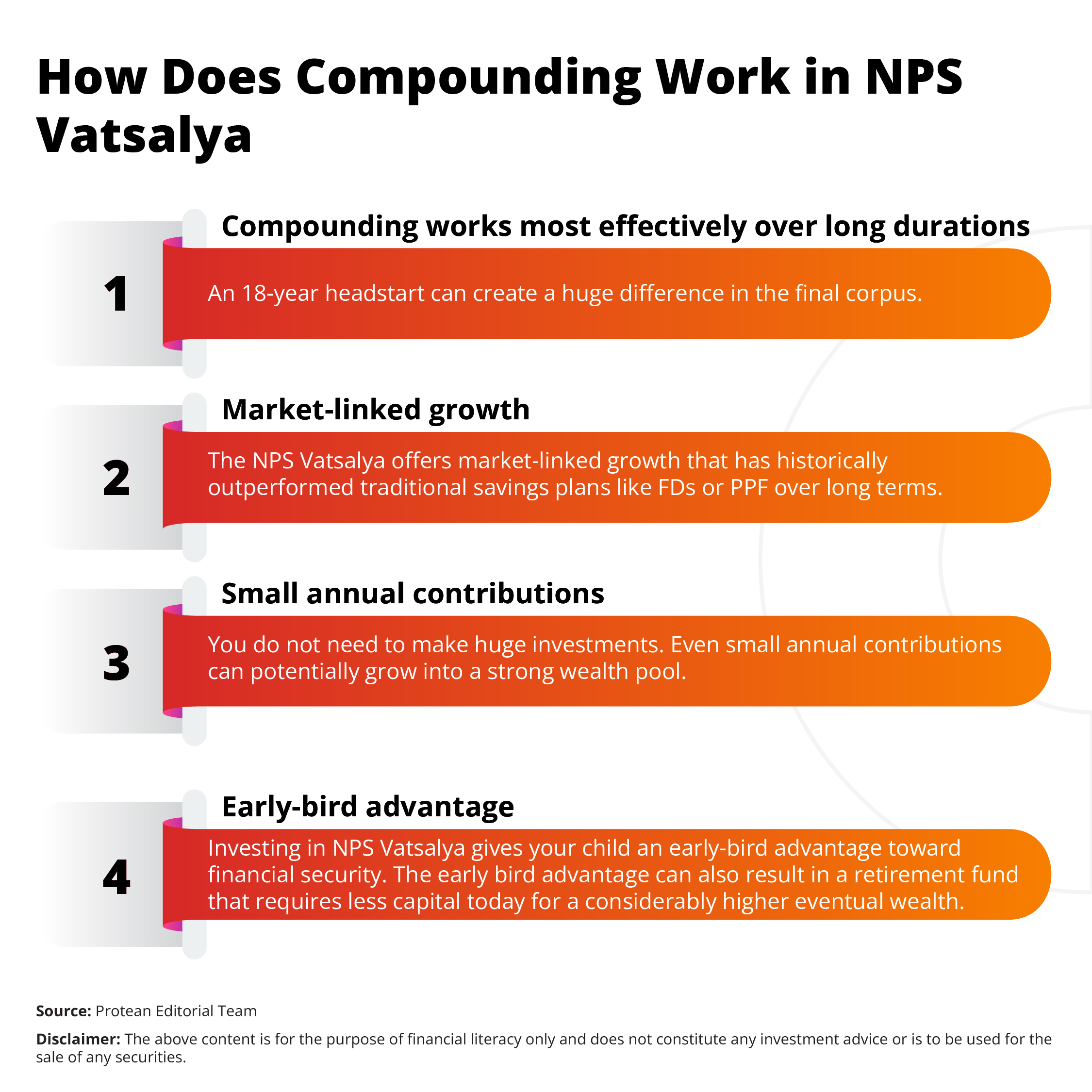

How Does Compounding Work in NPS Vatsalya

A child entering NPS Vatsalya at birth can have much advantage over an individual who starts at age twenty-five. Here is how compounding works in NPS Vatsalya.

How NPS Vatsalya Provides Flexibility That Fits Every Parent’s Pocket

The NPS Vatsalya scheme focuses on providing a few core features to Indian parents. Let us look at them.

- Accessibility - Accessibility remains a core feature of the NPS initiative for young Indian families. A minimum annual contribution of ₹1,000 makes the NPS Vatsalya scheme affordable for households across all income groups. Thus, investing in NPS Vatsalya can be accessible for parents across income-levels.

- Three Investment Sub-Options - Parents choose between three primary investment sub-options within the Auto Choice framework.

- Aggressive (LC-75)

- Moderate (LC-50)

- Conservative (LC-25)

With these options, you can choose automatic age-based asset rebalancing.

- The Active Choice - With this option, a guardian can decide the exact percentage of funds in Equity, Corporate Debt, and Government Securities manually.

- Switching - The guardians can enjoy the freedom to switch between fund managers and investment choices up to four times a year.

These are the flexibility parameters for your NPS portfolio to remain in total alignment with the family’s risk appetite and financial goals.

How is NPS Vatsalya More Than Just a Pension

The NPS Vatsalya scheme can be a financial lifeline during important stages of the child’s development and adulthood. Here is how.

- 3-Year-Holding Period - Current guidelines permit a partial NPS withdrawal of up to 25% after a three-year holding period. Guardians can utilise these funds for the child’s education or for the treatment of specified critical illnesses.

- Severe Disability - Access to these funds also applies in cases of minor subscriber's disability exceeding 75% as per PFRDA regulations.

- Financial Identity - Possession of a unique Permanent Retirement Account Number (PRAN) at a young age builds a distinct financial identity for the minor.

- Financial Discipline - The child can learn financial discipline by observing the growth of their own account over the years.

- Transparent - The NPS Scheme is regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Thus, there is enhanced transparency. A digital record of all transactions via the Central Recordkeeping Agency (CRA) can provide total clarity for the guardian.

Thus, the NPS Vatsalya scheme can balance long-term wealth creation and liquidity for life's major milestones and emergencies.

A Seamless Leap into Adulthood

The conversion of the account occurs automatically when the minor reaches the age of eighteen. Here is how the transformation would take place.

- The NPS Vatsalya would transition into a regular Tier-I account without the need for a new PRAN or a complicated account transfer process.

- The subscriber only needs to complete a fresh Know Your Customer (KYC) process within three months of attaining majority to take full control.

- After KYC, the young adult can manage their own investment journey as they enter the workforce.

The NPS framework remains consistent and portable regardless of the individual’s future job changes or relocation across India. Once the account becomes a regular Tier-I account, the subscriber can also open a Tier-II account for additional liquidity.

Conclusion

A PRAN card carries far more value than any modern gadget or expensive toy. Gadgets lose their utility and value over time. However, the NPS Vatsalya scheme grows alongside the child.

With NPS Vatsalya, you can gift financial independence to your child with a legacy of disciplined saving. Invest in your child's future today to witness the incredible power of a headstart in the NPS ecosystem.

Frequently Asked Questions (FAQs)

Q1: What is the minimum age to open an NPS Vatsalya account?

The NPS Vatsalya scheme is open to all minor Indian citizens generally from a very young age up to 18 years. Any minor child under the age of 18 qualifies for this account through a natural or legal guardian. The account stays in the name of the minor, but the parent or legal guardian operates it until the child attains majority.

Q2: What happens if the guardian passes away?

If the guardian passes away, the alternate guardian registered with the account usually takes over its operation. If both parents pass away, a legally appointed guardian may continue to operate the NPS Vatsalya account in the child’s interest, as permitted under the scheme.

Q3: Are there tax benefits for parents?

Yes, parents can claim tax benefits on contributions made to the NPS account of their minor child. Under the current tax laws, parents can claim deductions up to ₹50,000 under Section 80CCD(1B) for Tier 1 investments under the Old Tax Regime. This benefit is available in addition to the ₹1.5 lakh limit under Section 80C in the old tax regime.

Q4: What is the minimum annual contribution to keep the account active?

The NPS Vatsalya scheme requires a minimum annual contribution of ₹1,000 to maintain the account's active status. There is no specified maximum limit on the maximum contribution, allowing parents to invest more as their income grows.