Are you an NRI individual? Heard of NPS or a NPS scheme?

If you are looking for NPS for NRIs, you have found the right article.

Just like any other individual, retirement planning is a significant part of financial planning for the NRIs.

The National Pension System (NPS) is a well-regulated, transparent, and cost-effective pension scheme backed by the GoI.

However, there’s a crucial question: Can NRIs invest in a NPS scheme?

The answer is a firm yes, provided certain NPS eligibility conditions are met.

Let’s learn more on NPS for NRIs below:

What is NPS for NRIs

NPS is a retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Its primary goal is to provide retirement income by encouraging regular savings during an individual’s working life. Through NPS subscribers can invest in a mix of equities, corporate bonds, and government securities. They also have the flexibility to choose a fund manager and investment option with NPS (example - active or auto allocation).

NPS for NRIs can be an avenue to stay connected to India’s economic growth while planning for long-term financial security.

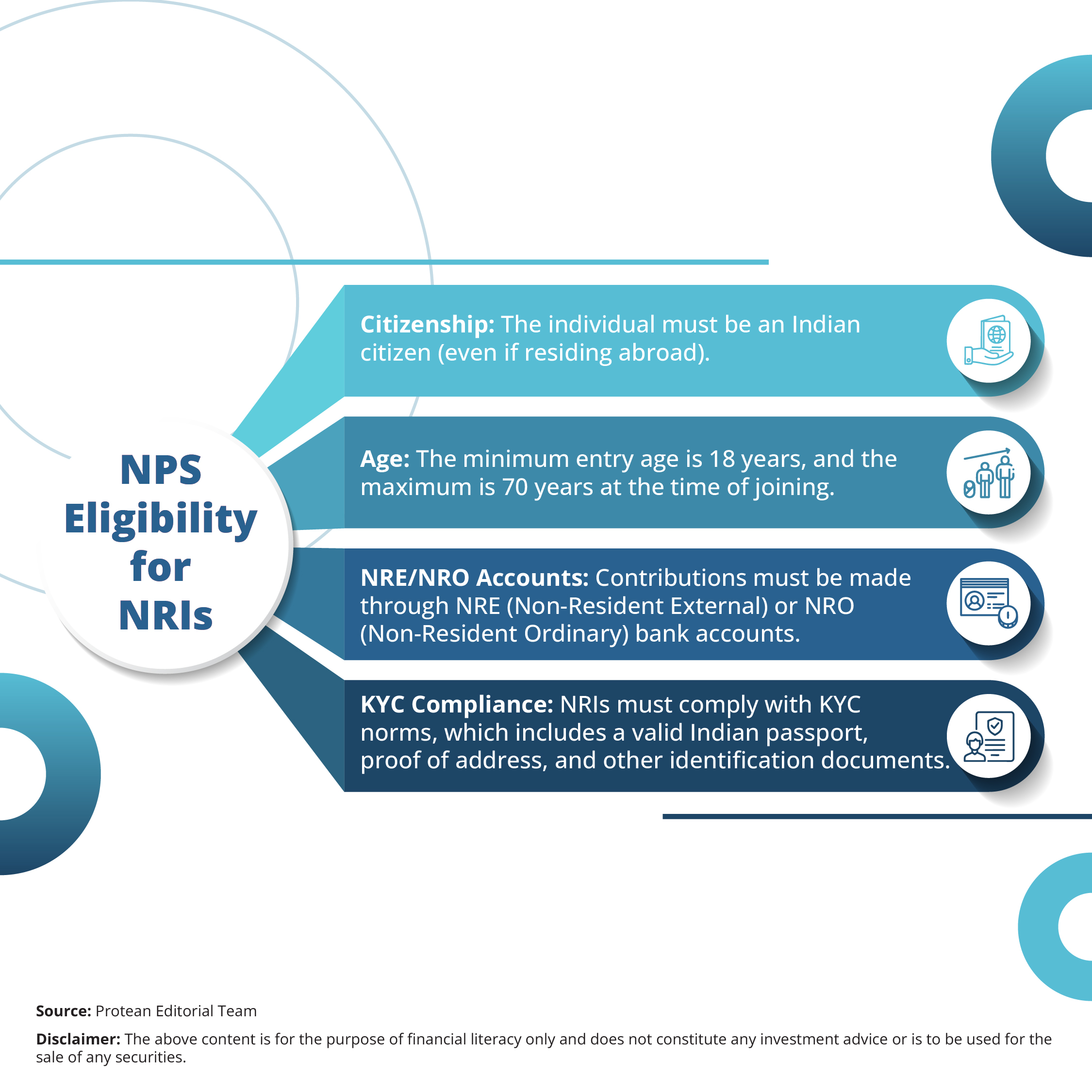

NPS Eligibility for NRIs

NRIs are explicitly eligible to open an NPS account, as per PFRDA guidelines. The following criteria apply:

Overseas Citizens of India (OCIs) are permitted to invest in NPS. However, the Persons of Indian Origin (PIOs) are not eligible to invest in NPS.

Tier I vs. Tier II Accounts for NRIs

NPS has two account types:

- Tier I Account is the primary retirement account. It is mandatory for all subscribers and can offer the maximum tax benefits, but it has restricted withdrawal rules until retirement.

- Tier II Account is a voluntary savings account with no tax benefits and no withdrawal restrictions. As an NRI you cannot open Tier II accounts under the current regulations.

NPS Tax Benefits for NRIs

NPS can provide a favorable tax structure under the Indian Income Tax Act, even for NRIs.

Contribution Benefits (Under Indian Income Tax Act)

Contributions made by NRIs to their NPS Tier I accounts are eligible for the same tax deductions as those available to resident Indians:

- Section 80C: Deduction up to ₹1.5 lakh annually under the overall limit.

- Section 80CCD(1B): Additional exclusive deduction of ₹50,000, over and above Section 80C, for NPS contributions.

Meaning, NRIs can claim a total deduction of ₹2 lakh in a financial year, which reduces their taxable income in India. These deductions can be particularly relevant for NRIs who have income taxable in India, such as from rental properties, capital gains, or other sources.

These tax benefits apply only to income earned in India. They do not reduce tax liability in the country of residence unless there is a Double Taxation Avoidance Agreement (DTAA) in place that recognises such deductions.

What is E.E.E. Status for NRIs

NPS is accorded an Exempt-Exempt-Exempt (EEE) status. Meaning, the contributions, returns, and withdrawals (within limits) are all tax-exempt under Indian tax law.

Here’s how this applies to NRIs:

- At Maturity (Age 60): Upon reaching the age of 60, an NRI can withdraw up to 60% of the accumulated corpus tax-free in India. The remaining 40% will be used to purchase an annuity, which provides monthly pension income. The annuity income, however, is taxable as per the applicable slab in India.

- Premature Exit (Before Age 60): If an NRI exits NPS before age 60, only 20% of the corpus can be withdrawn tax-free; the remaining 80% must go into an annuity.

- Partial Withdrawals: After completing three years in NPS, an NRI can make partial withdrawals (up to 25% of contributions) for specific purposes (e.g., medical expenses, children’s education, marriage, etc.). These are tax-free under Indian law.

- Upon Death: In case of the subscriber’s demise, the entire NPS corpus is paid to the nominee and is exempt from tax in India.

For NRIs, the taxation in their country of residence (if any) on annuity income or lump-sum withdrawal must be reviewed with local tax advisors to ensure clarity on global tax implications.

NPS for NRIs in Retirement Portfolio

Advantages for NRIs

- NPS can be better for building a corpus that can support old age income.

- With lower fund management charges, NPS can be one of the most cost-efficient pension products in the world.

- NRIs can allocate up to 75% of their funds to equities, offering capital appreciation potential.

- While NPS is rupee-denominated, it can offer a hedge for NRIs planning to return to India post-retirement.

Considerations and Limitations

- NPS proceeds are credited to the NRE/NRO account. But repatriation (especially of annuity income) is subject to RBI and FEMA guidelines.

- As noted, NRIs cannot open a Tier II account, limiting liquidity options.

- Some countries may tax overseas pension income or require declaration of foreign assets. NRIs need to review implications under their resident jurisdiction.

NPS can complement an NRI’s broader retirement strategy. These can include investing in mutual funds, real estate, foreign pension plans, and sovereign instruments.

Conclusion

NPS for NRIs can offer a structured, low-cost, and tax-efficient vehicle to build a retirement corpus aligned with Indian residency goals.

However, it is crucial to understand that while the NPS scheme can offer tax benefits and retirement security in India, one must also consider the applicable tax rules and reporting obligations in the country of residence. Also, liquidity and repatriation constraints need to be factored in before making large contributions.

Starting early and staying invested, especially with the additional deduction under Section 80CCD(1B), can be better for their retirement portfolio. Open NPS for NRIs account now!