If you just searched for “NPS tax benefit” on the internet, you might be diligently planning for your golden years.

Surely, you might want to know about the nitty-gritty details of the new tax regime and the old tax regime.

You might be skimming through all the knowledge available on the internet to make the most of your tax saving investments. Of course, it is your hard earned income and you might be concerned about its underlying tax implications.

There are notable nuances of the National Pension System (NPS) that require a detailed discussion. Keep reading further to understand the intricacies of NPS tax saving and its applicability for your retirement planning goals.

Introduction To National Pension System (NPS)

| What is NPS? |

NPS is a notable social security initiative by the Government of India. Its aim is to provide financial security to Indian citizens. It can help in retirement planning through systematic savings during an individual’s working life.

You can also think of it as a long-term investment vehicle. NPS tax saving (through Tier I) and Tier II investments are specifically designed to help you build a strong retirement corpus.

| There are two primary account types through which NPS can operate. Let us discuss them below: |

Tier I Account

Your Tier I account is your primary retirement account. Tier I is the account that can help you plan your retirement. You can also avail the NPS tax benefit when you invest in it.

On your retirement, your NPS Tier I account contribution will mature. However, you can still partially withdraw under specific permitted circumstances. It is mandatory for government employees who joined service after January 1, 2004 (except for armed forces) to have this account.

Tier II Account

Your Tier II NPS account is a voluntary savings account. The Tier II account offers you with greater investment flexibility. In this account, you can deposit and withdraw funds as and when you need them.

However, unlike Tier I, investments in Tier II accounts do not offer NPS tax benefit. With voluntary investments, you can complement your Tier I NPS account and aim for building a stronger retirement corpus that can stand the test of time. Therefore, you can use your NPS Tier II account as your regular investment account.

NPS can help you cultivate a habit of disciplined saving for retirement. It can also provide you with a regular income stream after you stop working. Thus, both Tier I and Tier II accounts can help you fulfil the dial role of income tax saving and retirement planning.

Tax Benefits Under The Old Tax Regime

There were numerous NPS tax benefits available under the old tax regime. These benefits had made NPS one of the popular investor choices for tax saving through retirement planning. The following are the popular sections for income tax saving under the old tax regime:

Section 80C

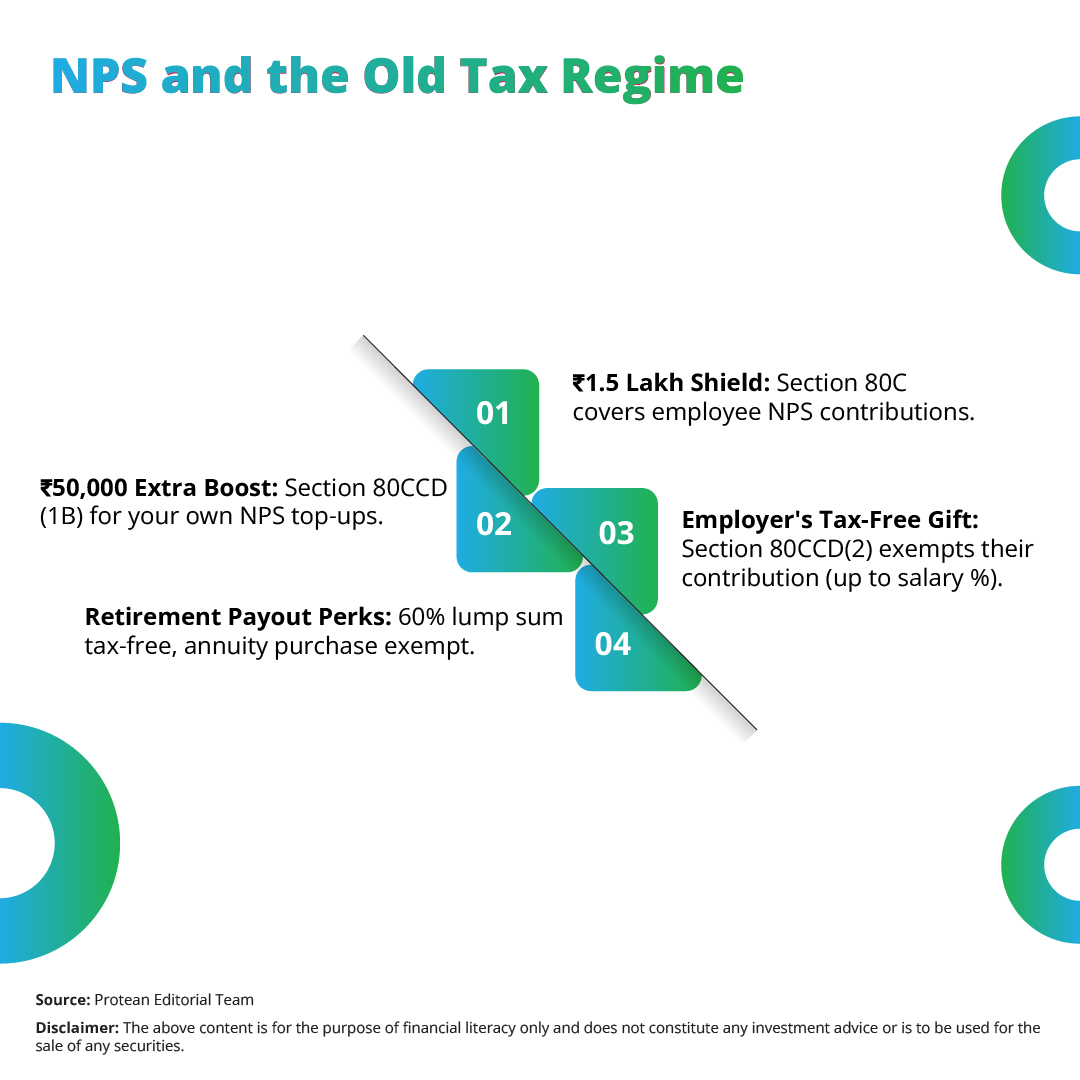

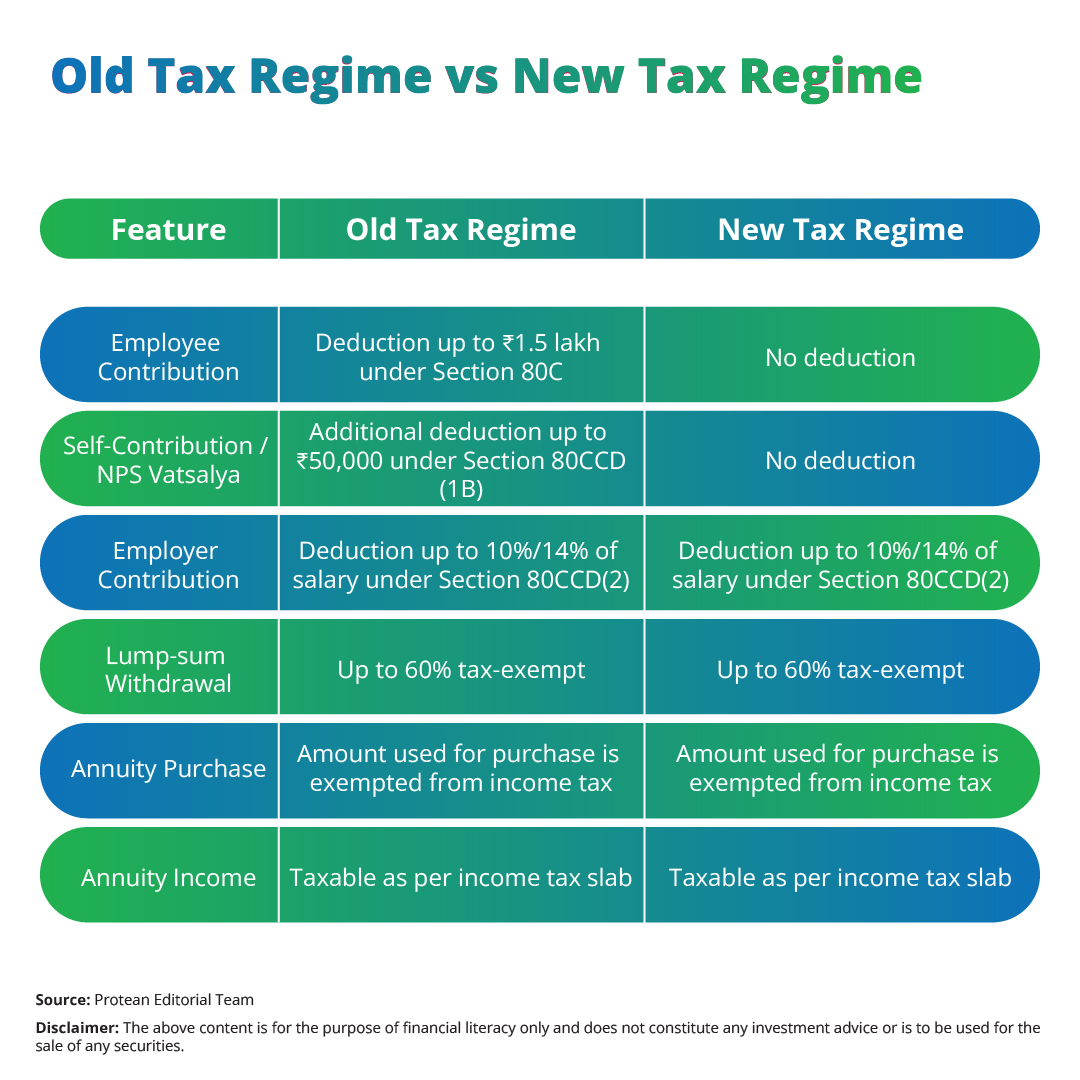

Section 80C of the Income Tax Act, 1961, is a well-known avenue for tax saving. It will include your contributions as an employee to your Tier I NPS account. You can claim a deduction of up to ₹1.5 lakh from your taxable income in a financial year under this section.

This limit is a combined limit for various eligible investments and expenditures. These investments and expenditures can include provident fund contributions, life insurance premiums, and certain other investments.

Suppose your annual salary is ₹10 lakh, and you contribute ₹75,000 to your Tier I NPS account. This ₹75,000 will be deductible from your gross total income, effectively reducing your taxable income to ₹9.25 lakh under Section 80C. If your total investments eligible under Section 80C (including your NPS contribution) amount to ₹1.8 lakh, you can still only claim a maximum deduction of ₹1.5 lakh.

Section 80CCD(1B) Brings an Exclusive NPS Bonus of ₹50,000

Beyond the umbrella of Section 80C, the old tax regime can offer an exclusive NPS tax benefit through Section 80CCD(1B). With this section, you can claim an additional deduction of up to ₹50,000 for your self-contributions to your Tier I NPS account. This deduction is over and above the ₹1.5 lakh limit available under Section 80C. With Section 80CCD(1B), you can divert more money towards your retirement planning goal through NPS investing.

Additionally, an individual may choose to contribute to the NPS Vatsalya Scheme. While contributions are subject to the standard tax limits under Section 80CCD(1) and 80CCD(1B), the tax-efficient structure of NPS would support effective financial planning, particularly for individuals in higher tax brackets.

Here is a hypothetical example.

Suppose you have already exhausted your ₹1.5 lakh limit under Section 80C through other tax saving investments. If you further contribute ₹60,000 as a self-contribution to your Tier I NPS account or you contribute in NPS Vatsalya, you can claim an additional deduction of ₹50,000 under Section 80CCD(1B), further reducing your taxable income. The benefits from the tax-efficient structure of NPS, though contributions to the child's account do not qualify for separate tax deductions, however, it brings your total potential deduction from NPS contributions to ₹2 lakh under the old tax regime.

Employer Contribution (Section 80CCD(2)) Putting Tax Exemption On The Top

The old tax regime can also provide a significant NPS tax benefit on the contribution made by your employer to your Tier I NPS. This can be done under Section 80CCD(2). This contribution is considered an income in your hands, but you can claim a deduction for it.

The maximum deduction allowed under this section is up to 10% of your salary (basic pay + dearness allowance) for non-government employees and up to 14% of your salary for government employees. There is no monetary limit on this deduction. Deductions are purely based on a percentage of your salary.

Here is a hypothetical example.

- You are a non-government employee with an annual salary of ₹12 lakh (₹1 lakh per month).

- Your employer contributes ₹1.2 lakh (10% of your salary) to your Tier I NPS.

- This entire ₹1.2 lakh is eligible for deduction under Section 80CCD(2).

- This is over and above the deductions you can claim under Section 80C and Section 80CCD(1B).

Taxation On Maturity/Withdrawal (Old Regime Perspective)

The tax treatment of your NPS corpus at maturity or upon withdrawal under the old tax regime is as follows:

- Lump-sum Withdrawal: A portion of the lump-sum withdrawal upon retirement is exempt from tax. As of the current regulations, up to 60% of the total accumulated pension wealth can be withdrawn as a lump sum, and this withdrawal is tax-exempt. The remaining 40% is required to be used for purchasing an annuity plan, which provides a regular pension income.

- Annuity Purchase: The amount utilised to purchase an annuity plan is also exempt from tax at the time of purchase. However, the annuity income you receive in the future will be taxed as per your applicable income tax slab rates.

| Learn about NPS Vatsalya. Click here for NPS Vatsalya eligibility and benefits. |

Tax Benefits Under The New Tax Regime

The new tax regime was introduced to simplify the income tax structure. This introduction will take a different approach to NPS tax benefit.

While it can offer lower tax rates in some slabs, it can have a trade-off of fewer exemptions and deductions.

No Deduction under Section 80C and 80CCD(1B)

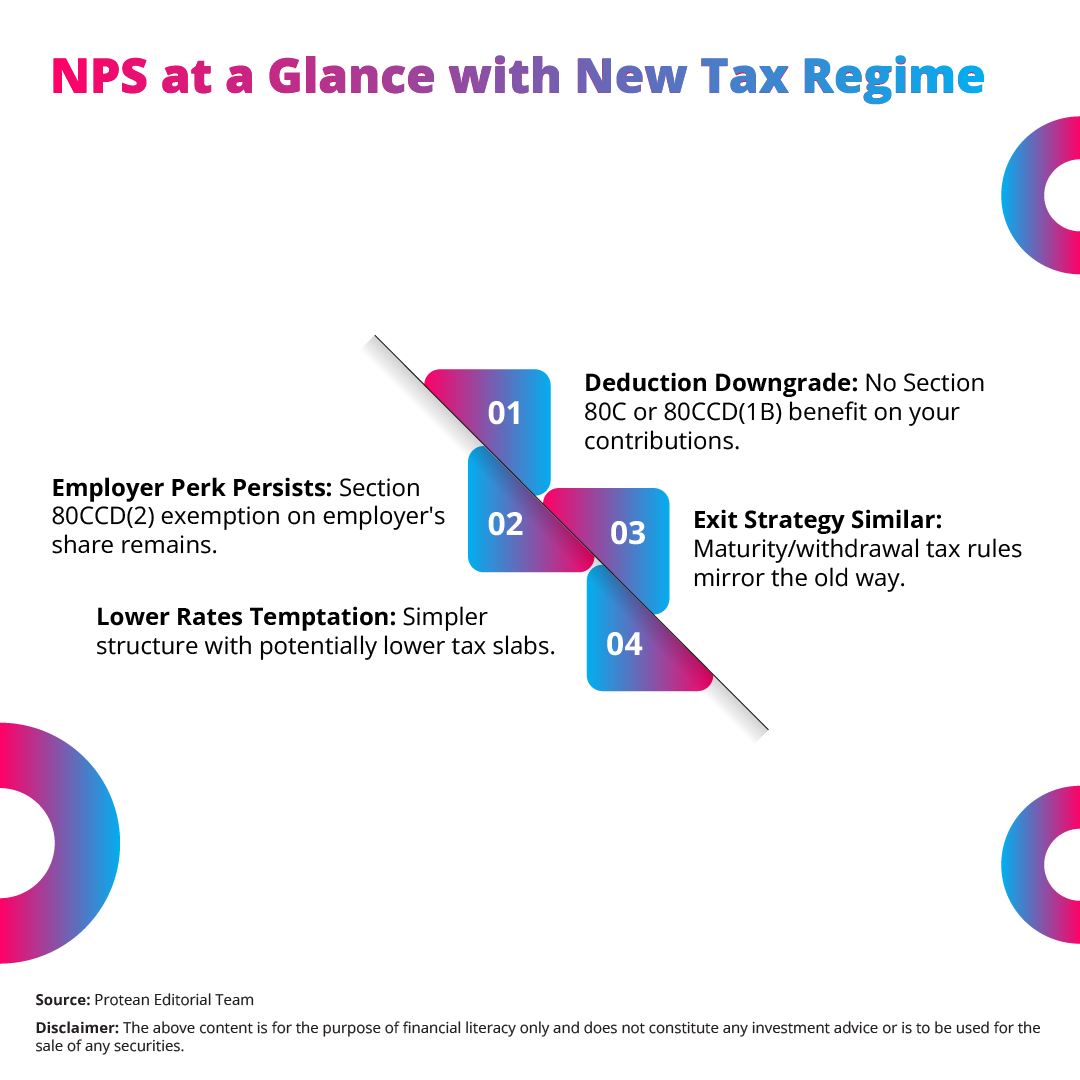

The new tax regime does not allow you to claim deductions under Section 80C and Section 80CCD(1B) for your contributions to the Tier I NPS account.

What does it mean for your income tax saving goals?

- This can mean that the ₹1.5 lakh deduction under Section 80C for employee contributions and the additional ₹50,000 deduction under Section 80CCD(1B) for self-contributions are not available if you opt for the new tax regime.

- This can be a major consideration if you are actively utilising these sections for tax saving.

Employer Contribution (Section 80CCD(2))

Interestingly, the tax exemption on the employer's contribution to your Tier I NPS account under Section 80CCD(2) will remain applicable even if you choose the new tax regime. Meaning, the contribution made by your employer (up to 10% of salary for only non-government employees and 14% for government employees under Old Tax Regime and up to 14% for government and non-government employees under New Tax Regime) would continue to be exempt from tax in your hands. This would be regardless of the tax regime you select.

This consistent treatment could highlight the government's intention to encourage employer-sponsored retirement planning.

Taxation at Maturity/Withdrawal (New Regime Perspective)

The taxability of the NPS corpus at maturity or withdrawal under the new tax regime is largely going to be similar to that under the old tax regime. Here are the notable points:

- Lump-sum Withdrawal: The portion of the lump-sum withdrawal (up to 60% of the accumulated corpus) would remain tax-exempt.

- Annuity Purchase: The amount used to purchase an annuity would also be exempt from tax at the time of purchase. The subsequent annuity income will be taxed according to your applicable income tax slab rates.

Therefore, the upfront NPS tax benefit on your own contributions would differ significantly between the two regimes. However, the tax treatment at the time of withdrawal or annuity purchase would broadly be the same.

A Quick Comparison between Old Tax Regime and New Tax Regime

Here is a look at a table summarising the key NPS tax benefit points under both the old tax regime and the new tax regime:

| Which Regime Are Better For Your NPS Benefits? |

It is not a one-size-fits-all decision to decide whether you want to choose the new tax regime or the old tax regime. The decision between the two regimes would hinge on your overall financial situation. You can take into account your preference for claiming deductions, and your other tax saving avenues.

You might find the old tax regime more beneficial for your NPS investments if:

- You actively contribute for NPS tax benefit to your Tier I NPS account.

- If you want to leverage the deductions under Section 80C and Section 80CCD(1B).

- You are making significant investments in other instruments that qualify for deduction under Section 80C (maximising the ₹1.5 lakh limit).

- You prefer to claim various other deductions available under the old tax regime. For example, your home loan interest, medical insurance premiums, and education loans.

On the other hand, the new tax regime might be more appealing if:

- You are a fan of lower tax rates.

- You need a simplified tax structure without the hassle of tracking and claiming numerous deductions.

- Your employer is making a substantial contribution to your Tier I NPS under Section 80CCD(2). The benefit remains available in both regimes.

- Your total deductions under the old tax regime, even including NPS contributions, are not significantly reducing your overall tax liability compared to the lower rates offered by the new tax regime.

To effectively combine your tax saving goal with your retirement planning goals, you can evaluate your entire income tax profile, not just the NPS tax benefit in isolation. Calculate your tax liability under both regimes, considering all applicable deductions and exemptions under the old tax regime, to determine which option results in a lower tax outgo for you.

Key Takeaways

Before you begin tax saving for the financial year, it is essential for you to study and compare both the tax regimes. You can effectively combine your retirement planning goals with your tax saving goal by understanding NPS investing, NPS tax benefit and the two tax regimes (the new tax regime and the old tax regime).

Your ultimate choice between the two regimes should depend on your individual preferences, tax slabs and financial goals. You can carefully assess your income, investment patterns, and eligibility for various deductions before making a decision. Whether it is the old tax regime or the new tax regime, investing in NPS is essential for tax benefits and securing a financially independent retirement.