Are you looking to read the details regarding the Multiple Scheme Framework (MSF)?

If you have been an NPS investor for years, your Permanent Retirement Account Number (PRAN) has quietly been accumulating contributions invested in a steady mix of equity and debt. Now, you can consider your NPS leading to three broader possibilities.

- Diversified investment strategies

- Higher equity exposure

- Customised risk profiles

This is exactly what a Multiple Scheme Framework (MSF) under NPS is. For many investors, MSF can represent a pivotal shift. Your existing PRAN is no longer limited to a single, uniform investment scheme. Instead, it can now offer greater flexibility, control, and choice.

Let us understand Multiple Scheme Framework with the help of an analogy.

A weekday evening. Two friends, Arjun and Nita, both salaried professionals in their 30s, meet for coffee after work. The conversation quickly drifts to retirement planning.

Understanding the Change: The New MSF in NPS

Nita: Arjun, have you heard about this new Multiple Scheme Framework in NPS? My HR mentioned it today. It seems like a big change in how our PRAN works.

Arjun: Oh yes, the Multiple Scheme Framework or MSF! It’s quite a shift. Basically, PFRDA has revamped NPS to make it more flexible. Earlier, our PRANs were just accumulating funds under one fixed equity-debt mix, right? Now, they’ll let us choose multiple schemes within the same PRAN.

Nita: So, no more “one-size-fits-all” structure?

Arjun: Exactly. It’s an evolution with which you’ll be able to build your own portfolio inside NPS instead of being stuck with a single scheme.

The Old System vs. The New MSF Reality

Nita: Can you explain how it was before, and what’s changing now?

Arjun: Sure. Earlier, non-government subscribers like us could access only “Common Schemes.” Each Pension Fund Manager (PFM) offered one scheme per asset class, and the equity cap was 75%. You had to pick either Auto Choice or Active Choice.

Nita: Right, mine’s been on Active Choice for years.

Arjun: Now, with the MSF effective from October 1, 2025, as formalised by PFRDA, the system becomes far more flexible.

Here is what you will be able to do:

- Hold multiple schemes under your single PRAN across different PFMs or across multiple schemes of the same PFM.

- PFMs can design MSF schemes targeting different investor segments or risk profiles (for instance, those suited for professionals, gig workers, or corporate subscribers, depending on design approval).

- Select risk-variants (moderate, high) with the high-risk variant now allowing up to 100% equity exposure.

- Benefit from the revised cost structure. PFMs may charge up to 0.30% of AUM for MSF schemes (versus much lower earlier) and may get an additional 0.10% incentive for fresh subscriber inflows.

- Follow clearer vesting rules. Minimum vesting period of 15 years for MSF schemes, with exits aligned to age 60 or retirement, whichever is earlier.

Nita: So basically, my NPS will feel more like a personalised investment account now.

Arjun: Exactly. The old single-scheme structure is now giving way to a portfolio-style system within NPS.

Unlocking New Opportunities with MSF

Nita: Tell me more about what kind of new opportunities this brings.

Arjun: The best part is that your same PRAN can now become a gateway to diversified investments.

Portfolio Diversification within NPS

Earlier, you could invest in one scheme under NPS. Now, you can hold multiple schemes at the same time. For example, you might choose a high-equity scheme for long-term growth, a moderate-risk scheme for mid-career stability, and a conservative debt scheme for your later years.

Up to 100% Equity Exposure

If you have a high risk appetite and want a long retirement horizon, a higher-equity option within NPS, up to the regulatory cap, instead of an external investment product.

Persona-based schemes and strategic alignment

Under MSF, PFMs can design differentiated schemes addressing varied risk-return preferences, allowing subscribers from different professional backgrounds to choose suitable options. For example, self-employed professionals, digital-platform workers, corporate employees with employer contribution.

Easier switching and monitoring

MSF has the following relevant features:

- You can track each scheme by its NAV, benchmark, and risk-o-meter.

- You may switch between schemes in line with PFRDA’s prescribed limits and conditions.

- Each scheme’s risk level is clearly defined through a risk-o-meter.

- Your NPS account now functions as a mini-portfolio, enabling you to fine-tune your investment strategy within the same PRAN.

Leverage existing infrastructure (your PRAN)

The best part here is that you don’t need a new account or any change to your Tier I setup.

- Your PRAN stays the same, carrying your records and tax benefits.

- The MSF can help you add multiple schemes under it. It can ensure a smooth and convenient transition.

Nita: So my PRAN basically turns into a mini investment portfolio!

Arjun: Exactly. You get flexibility and transparency while staying within the same system.

Using Your Existing PRAN

Nita: Do we have to open a new account for this?

Arjun: Not at all. That’s the beauty of it. Your existing PRAN remains the same, along with all your Tier I benefits and records. You just get to add multiple schemes under it without extra paperwork or compliance.

Navigating the Corporate Model and Contributions

Nita: What about people like us who contribute through our employers under the corporate NPS model?

Arjun: The MSF works well there too. In the corporate model, in some cases, Tier I participation remains mandatory, and both employer and employee contributions flow into the same PRAN. With MSF, you’ll now be able to choose how those contributions are invested.

Nita: That’s useful! So can I align my employer’s contribution with my own investment strategy?

Arjun: Exactly. During onboarding or reviews, you can work with your Pension Fund Manager or select schemes online to choose the investment strategies that best suit your profile. Some PFMs are even designing dedicated MSF schemes for corporate subscribers, tailored to employer patterns and long-term goals.

Nita: That makes it far more strategic than before.

Arjun: It does. And when you check your corporate NPS benefit statement, you’ll actually see your scheme name, benchmark, and risk level clearly mentioned. That’s a big improvement in transparency.

Main Points To Consider When Allocating Contributions

Nita: So before shifting to MSF, what should we keep in mind?

Arjun: There are a few key points:

- Continuity of Tier I Rules – The main Tier I framework stays the same, including vesting and annuitisation.

- Choice Across PFMs – You can choose schemes within one PFM or across several PFMs.

- Employer Contribution Alignment – Ensure both your and your employer’s contributions are aligned to your chosen MSF schemes through mutual agreement.

- Review of Benefit Statements – Keep checking your statement for scheme name, benchmark, and risk details.

Nita: Makes sense. It’s more power, but with responsibility to monitor.

Arjun: Exactly.

Costs, Vesting, and Strategic Planning

Nita: Let’s talk about money, what’s the cost and locking period again?

Arjun: The cost structure allows PFMs to charge up to 0.30% of AUM annually, slightly higher than before. Plus, PFMs can earn an extra 0.10% for new inflows if they attract 80% new subscribers for three years.

Nita: That is fair if they are offering better products and services.

Arjun: True. Just remember that there’s a minimum 15-year vesting period for MSF schemes. Exits are allowed at 60 or retirement, whichever is earlier.

As for switching, you can:

- Move from an MSF scheme to a common scheme during vesting, but

- Not between two MSF schemes until vesting ends.

So, it is important to plan your selections wisely.

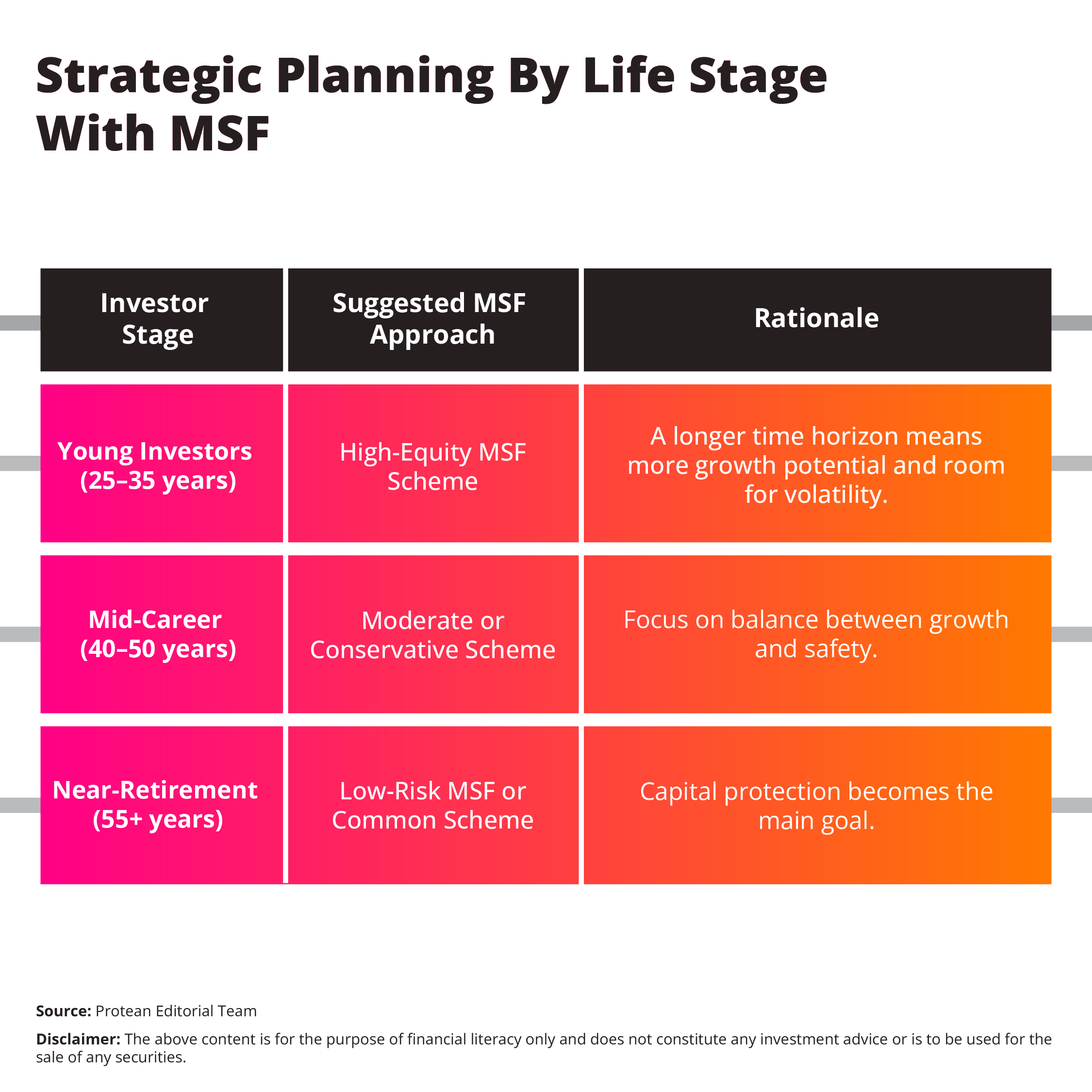

Strategic Planning By Life Stage

Nita: How would you suggest planning it based on age or career stage?

Arjun: I’d look at it like this:

You could even go for a core-satellite approach, one stable core scheme with a couple of growth-oriented ones for better overall returns.

Nita: That’s very practical. It’s like life-stage investing within NPS itself.

Conclusion

Nita: Honestly, this feels like the upgrade NPS needed. It used to be too rigid.

Arjun: Exactly! The Multiple Scheme Framework transforms NPS from a plain, fixed structure into a customisable, dynamic retirement platform.

It lets you:

- Hold multiple schemes under your PRAN,

- Go up to 100% equity exposure,

- Align investments with your risk profile and career stage,

- Manage corporate contributions more effectively, and

- Track everything with better visibility.

Nita: So it’s like having more flexibility like mutual funds, but with the discipline and tax efficiency of NPS.

Arjun: Perfectly said. It’s still the same safe, long-term pension product, just more modern and investor-friendly.

Nita: I’m definitely going to revisit my NPS allocations once this goes live.

Arjun: Same here. With MSF, we are not just saving for retirement, we are designing it.