The PFRDA (Pension Fund Regulatory and Development Authority) has introduced major regulatory changes to make the NPS (National Pension System) more flexible, transparent, and subscriber‑friendly for NPS subscribers. They have made changes such as:

- Revisions to exit norms

- Changes in withdrawal rules

- Investment options

- Scheme structures

The NPS changes are focussed on improving long‑term retirement savings for India’s workforce. These changes are effective for both, existing and prospective NPS subscribers. They can optimise retirement planning through market‑linked strategies while retaining the scheme’s tax benefits. Here is more on the NPS changes and their impact on NPS subscribers.

A Shift in Exit Norms

With the revised NPS rules, non-government NPS subscribers’ flexibility at retirement has increased. This is an improvement from the earlier use of the corpus to fund annuity and a longer contribution period required for exit.

- Higher Lump‑Sum Withdrawal Limit - With the recently changed NPS norms, non‑government subscribers can withdraw up to 80% of their accumulated pension wealth. They can withdraw it as a lump sum at normal exit (superannuation, age 60 or specified milestones). Also, now, only 20% is required for annuity purchase. This is a shift from the earlier limited lump‑sum withdrawal to 60% (40% reserved for annuity).

- Removal of 5‑Year Lock‑in - As per the earlier norms, a minimum five‑year lock-in period was required before being allowed to exit prematurely. This mandatory lock-in has now been removed for non‑government participants.

- Increased Investment Horizon - Now, subscribers can remain invested in NPS until age 85. This increase in the investment age limit is increased from the earlier 75‑year limit. Thus, investors can now experience extended capital growth and potentially higher retirement corpus.

These modifications can give NPS subscribers more control over how they manage accumulated pension wealth. Also, they support individual choices between liquidity and ongoing retirement income through annuity solutions.

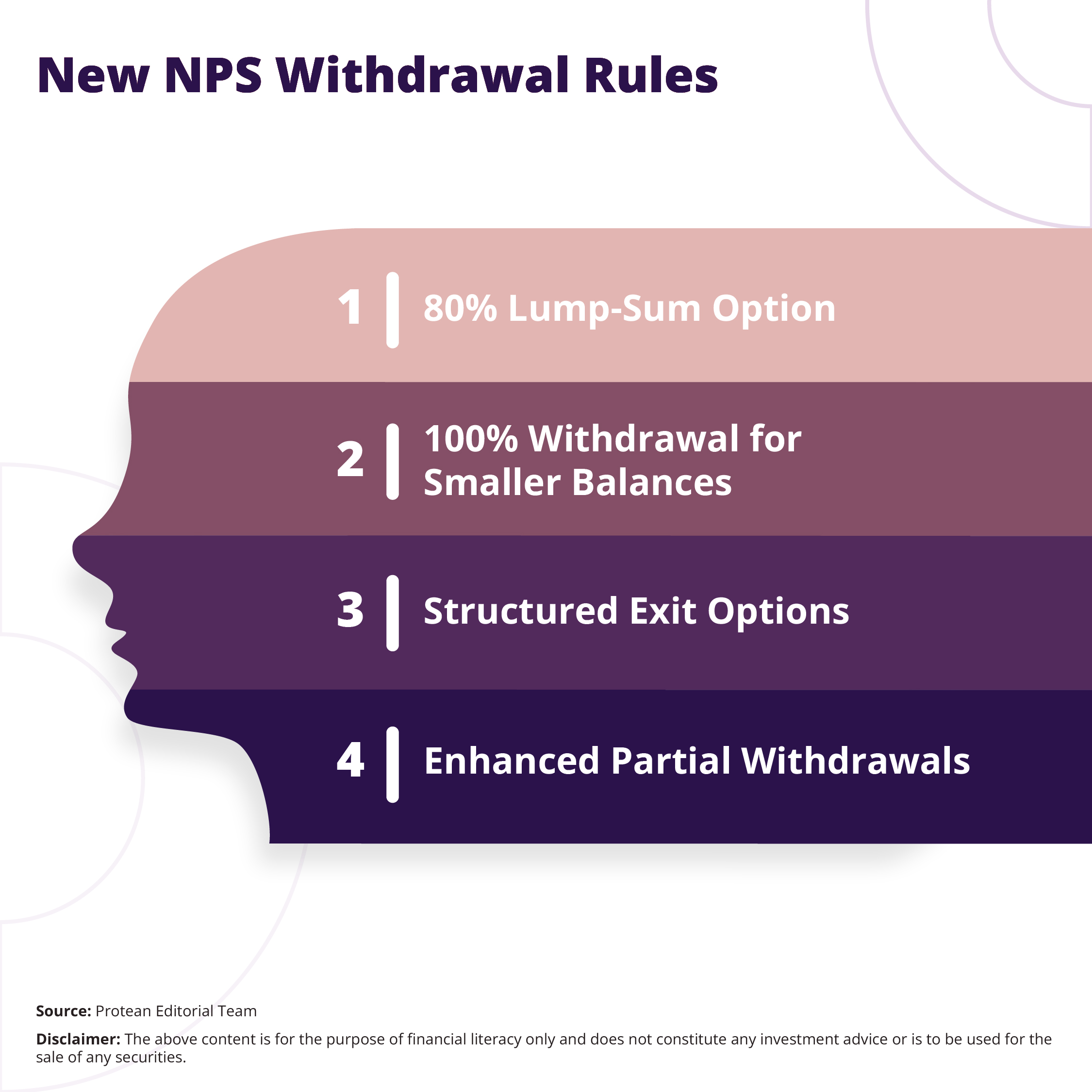

New NPS Withdrawal Rules

The current PFRDA (Exits and Withdrawals under the NPS) (Amendment) Regulations, 2025 regulations have updated withdrawal norms for non‑government subscribers.

80% Lump‑Sum Option

With the revised rule, non‑government NPS subscribers can take up to 80% of their corpus as a lump sum at exit. Thus, only 20% of the accumulated pension wealth needs to be used to purchase an annuity. Thus, NPS subscribers can achieve a balance between upfront funds and a periodical pension.

100% Withdrawal for Smaller Balances

NPS subscribers can withdraw the full corpus on normal exit without the compulsory annuity purchase for accumulated pension wealth below thresholds such as ₹8 lakh. This change in rules can particularly benefit NPS subscribers who retire early or those with smaller retirement corpuses.

Structured Exit Options

In addition to lump sum, NPS subscribers can also employ systematic unit redemption and structured periodic withdrawal options. Such structured exit options can offer the flexibility to match withdrawals with individual financial goals to the subscribers.

Enhanced Partial Withdrawals

Now, NPS allows up to four partial withdrawals before reaching age 60. But this is subject to conditions like educational or medical needs. With increased partial withdrawal rules, NPS subscribers can gain liquidity without full exit.

The recent NPS reforms empower investors to customise their retirement payout strategies along with the essential pension income focus. The ability for many subscribers to access a larger proportion of accrued savings up front can improve investor confidence and alignment with diversified financial objectives.

Multiple Scheme Framework (MSF)

Another milestone in NPS reforms is the introduction of MSF for non‑government NPS subscribers.

With MSF, participants can hold multiple investment schemes under a single PRAN (Permanent Retirement Account Number). MSF is embedded with many advantages of improved scheme flexibility, higher equity allocation potential and PAN-led consolidation.

- Scheme Choice and Flexibility - Pension Funds can design schemes specifically for subscriber groups such as self‑employed professionals or corporate employees. Each of these schemes can have a varied risk‑return profile.

- Higher Equity Allocation - NPS subscribers can choose high-risk variants, within MSF. Such variants can offer up to 100% equity exposure for long‑term growth potential.

- PAN‑based Consolidation - Holdings across schemes are consolidated at the PAN level. Thus, unified reporting and easier portfolio tracking is possible.

The MSF framework helps investors customise investments and align asset allocation with their risk appetite and retirement horizon.

Entry and Exit Age Extension

PFRDA has also extended the permissible entry and exit ages for NPS participation. Now, the maximum age for opening and contributing to NPS remains up to age 85. Thus, individuals can join NPS even later in their career or continue investing well into their 60s, 70s, and beyond.

This NPS extension complements the relaxed exit age provisions. With these extensions, seasoned contributors can benefit from longer market exposure and compound growth.

Conclusion

NPS still offers robust tax incentives. Thus, it combines the dual goals of tax saving and retirement planning for Indian investors. NPS Tier-I contributions are eligible for deductions under Section 80CCD (1), Section 80CCD(1B) and Section 80CCD(2).

Together, with these provisions investors can create a triple tax benefit to considerably reduce taxable income and build a strong retirement corpus.

The recent regulatory developments, including expanded exit flexibility, modernised withdrawal norms and multi‑scheme investment options, can help NPS subscribers to have more control over retirement planning than ever before. Therefore, opening or increasing contributions to a Tier‑I account, specifically under the updated framework, offers tax efficiency, investment flexibility and greater peace of mind as part of a disciplined retirement planning journey.