Are you trying to learn about NPS withdrawal rules from the internet?

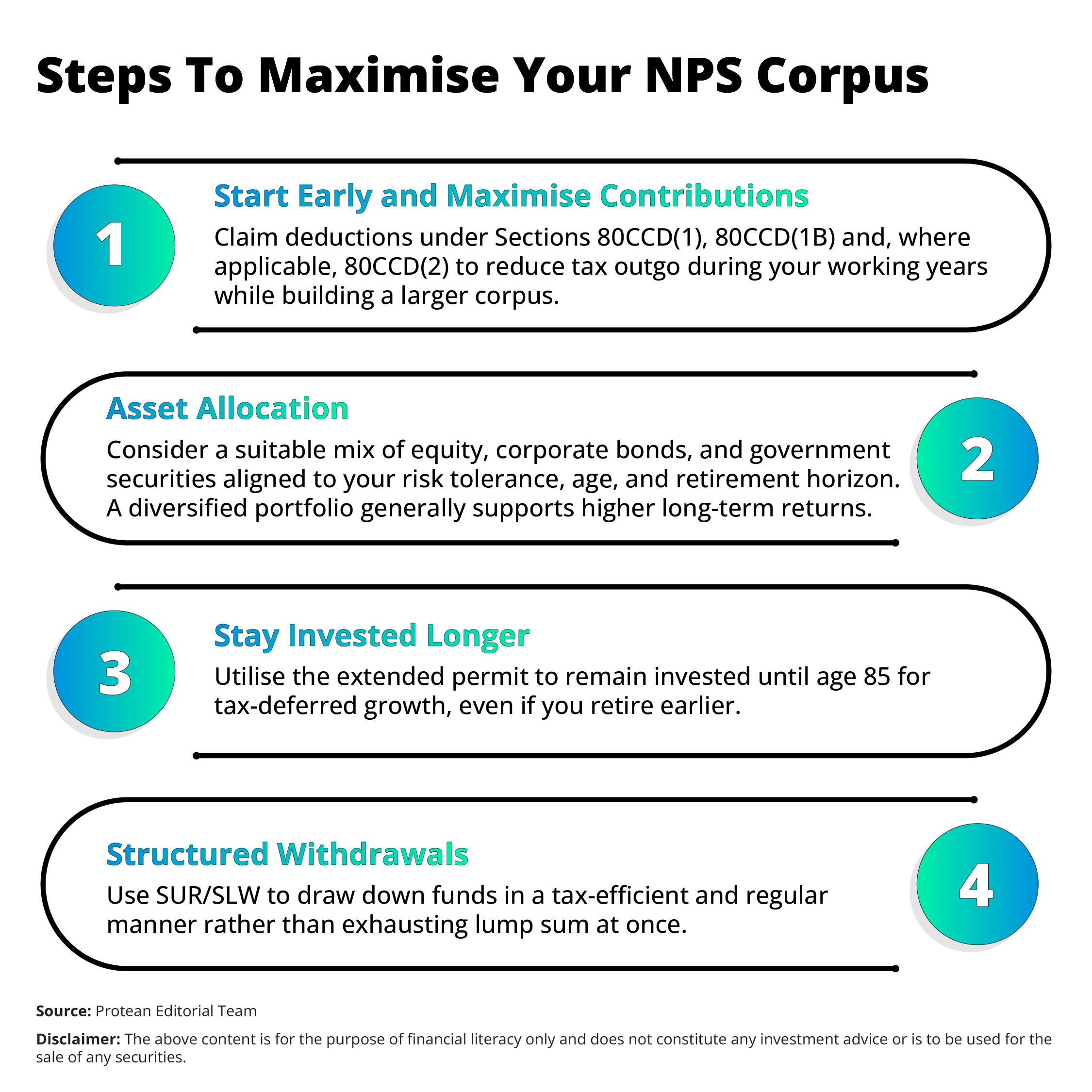

The National Pension System (NPS) has long been a major retirement planning tool in India. It balances disciplined long-term savings with tax-efficient growth.

In December 2025, the PFRDA (Pension Fund Regulatory and Development Authority) announced major modifications to exit and withdrawal norms under the NPS.

With these changes, non-government subscribers can withdraw up to 80% as a lump sum (minimum 20% annuity for corpus >₹12 lakh), making NPS more flexible.

Here is more on the revised withdrawal rules, tax implications, and strategies to maximise the NPS corpus for a secure retirement.

New NPS Withdrawal Rules for 2026

There are three main changes in the revised PFRDA (Exits and Withdrawals under the National Pension System) Regulations, 2025.

1. Higher Lump Sum Withdrawal at Exit

The mandatory annuity requirement is reduced from to 20% (from the earlier 40%) of the accumulated pension corpus.

Subscribers can now withdraw up to 80% of their NPS corpus. They can do this either as a one-time lump sum or through structured options such as Systematic Unit Redemption (SUR) or Systematic Lump Sum Withdrawal (SLW).

2. Corpus-Based Withdrawal Slabs

The revised withdrawal limits are based on the size of the accumulated pension wealth.

- For a corpus of up to ₹8 lakh - 100 % withdrawal as a lump sum is now permitted.

- For a corpus between ₹8 lakh and ₹12 lakh - Here, up to ₹6 lakh can be withdrawn. But the remaining amount is to be used through SUR or annuity purchase.

- For a corpus exceeding ₹12 lakh - The standard 80% lump sum and 20% annuity structure is applicable.

3. Reduced Vesting Period and Extended Investment Tenure

The minimum participation period for a normal exit has now been reduced to 15 years.

Furthermore, subscribers are also allowed to remain invested in NPS up to the age of 85. This enables continued tax-deferred compounding even after retirement.

Why More Lump Sum Means a Better Retirement

More accessible lump sum savings at retirement can largely improve your financial security and flexibility.

Traditionally, the NPS framework had mandated a larger portion of the corpus be used to buy an annuity. This had reduced immediate liquidity and forced retirees into predetermined pension streams.

But with the new 80% lump sum option, retirees can gain greater discretion to meet large post-retirement costs. These are costs such as healthcare, debt repayment, family support, or strategic reinvestment.

This can benefit individuals with higher retirement objectives. It can also benefit those who prefer a diversified retirement income approach that combines:

- Lump sum reserves

- Annuity income

With access to a larger upfront amount, retirees can manage inflation and market-related risk through customised asset allocation in a better way.

Is the 80% Withdrawal Tax-Free?

The PFRDA now permits up to 80% lump sum withdrawal. According to the Income Tax Act, 1961, only up to 60% of the accumulated pension wealth withdrawn on retirement is explicitly exempt from tax under Section 10(12A).

The additional 20 per cent withdrawal is not automatically tax-free and may be taxed according to your income tax slab unless future budget changes provide an exemption.

Also, the annuity purchased with the mandatory 20% is not taxed at the time of investment but the pension received later will be treated as taxable income. Therefore, planning for tax on the extra 20% withdrawal is crucial to avoid surprises in your retirement year.

Conclusion

The 80% lump sum provision in NPS is changing the way Indian retirees access and use their retirement savings in 2026 and beyond.

The compulsory annuity requirements are reduced and flexible exit and structured withdrawal options are introduced.

Thus, PFRDA’s reforms provide non-government subscribers greater control over their financial destiny. However, must be weighed against current tax provisions that currently favour only 60% of lump sum as tax-free for Government employees.

With thoughtful planning, early accumulation, and understanding tax implications retirees can fully benefit from the new NPS withdrawal landscape.

Frequently Asked Questions

Q1: Can any NPS subscriber withdraw 80% of their corpus at retirement?

Yes. Under the revised PFRDA rules, non-government NPS subscribers with accumulated pension wealth above ₹12 lakh can withdraw up to 80%. They can make the withdrawal as a lump sum upon retirement or normal exit after 15 years.

Q2: Is the entire 80% lump sum tax-free?

Currently, only 60% of the withdrawal enjoys tax exemption under Section 10(12A). The additional 20% could be taxable until tax laws are amended.

Q3: What happens to the remaining 20%?

At least 20% must be used to purchase an annuity, which ensures a periodic pension stream.

Q4: Can I stay invested in NPS after age 60?

Yes. The revised rules permit remaining invested in NPS up to age 85, offering additional compounding and exit flexibility.