NPS Vatsalya can help build a substantial retirement corpus through compounding, depending on contributions and returns.

Here is a story about Aarav and his parents to help you better understand the NPS Vatsalya scheme.

When Aarav was born in 2026. His parents, Rohan and Meera, were already thinking beyond school admissions and Aarav's birthday milestones.

They focused on planning his future.

They were aware that inflation erodes purchasing power and traditional savings fall short, so they opened an NPS Vatsalya account. This marked the start of a disciplined, long-term financial journey with regular contributions for Aarav's future. They started NPS Vatsalya investing with the aim of building a ₹10 crore corpus for their child.

About NPS Vatsalya Scheme

With the NPS Vatsalya scheme, parents can open a National Pension System (NPS) account in the name of a minor child. The parents act as the guardian until the child turns18 years old.

The NPS Vatsalya is regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

In NPS Vatsalya, your contributions are invested across equity, corporate debt, and government securities.

Parents can choose between the Active Choice and Auto Choice options.

- Active Choice - Here, parents will actively manage fund allocation across equity (up to 75%), corporate bonds, government securities, and alternate assets (max 5%). Their allocation will be based on their risk preference.

- Auto Choice - The allocation can adjust automatically over time. The equity exposure would gradually reduce as the child nears adulthood. This can be done with options like Conservative (LC25), Moderate (LC50), and Aggressive (LC75) Life Cycle Funds.

Thus, NPS Vatsalya scheme is recognised for its transparency, professional fund management, and ultra-low cost structure that make it a long-term child-focused investing pro.

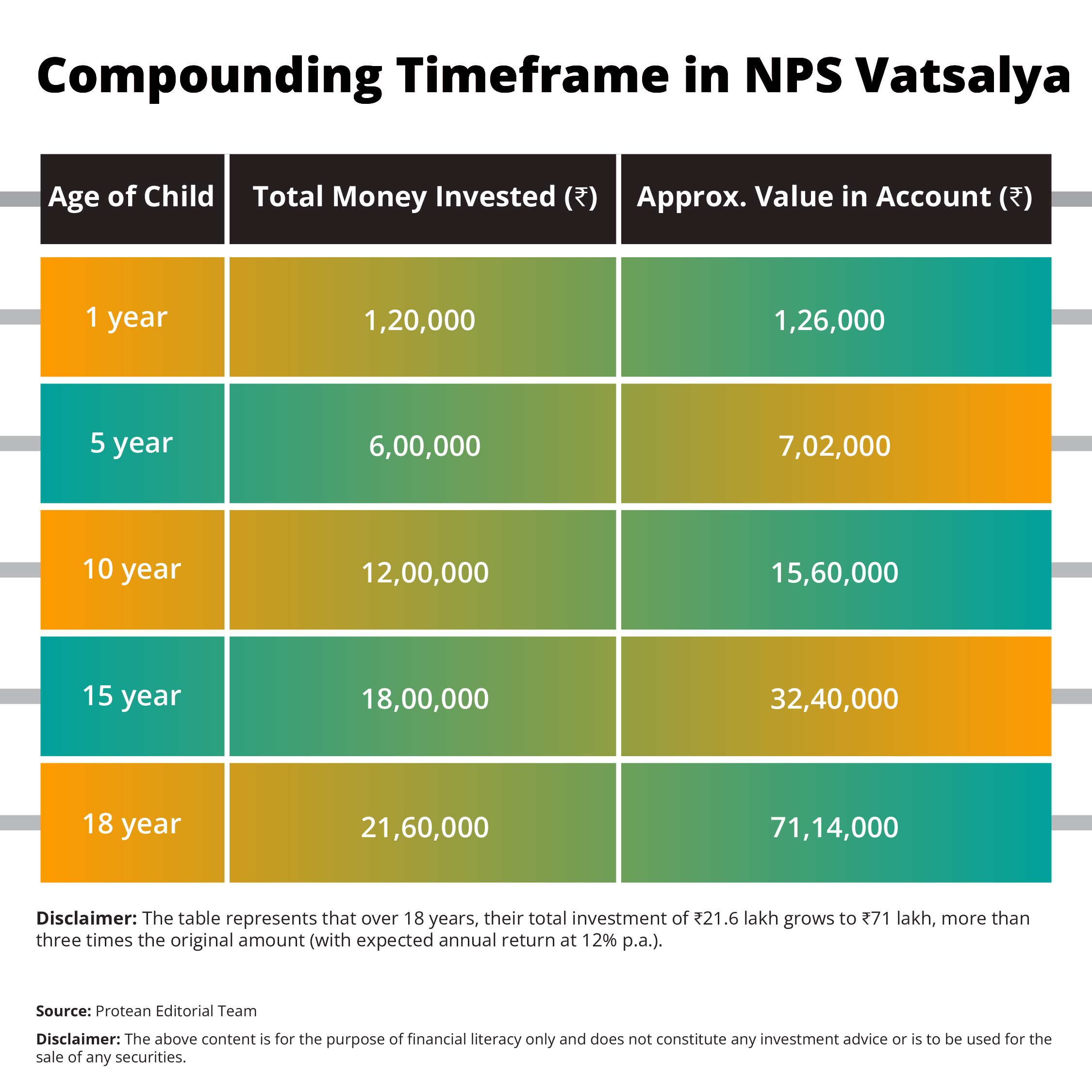

The Roadmap to a ₹10 Crore Corpus: A 2026 Perspective

In our example, when Aarav turned one, his father started a monthly contribution of ₹10,000 into NPS Vatsalya. He was consistent in his investments.

Years passed, his incomes rose and contributions too increased gradually. But what remained unchanged was the time horizon.

The power of compounding worked its magic. The corpus started accelerating after the first decade. As Aarav reached his teenage years, the investment growth far outpaced the total contributions made.

Digital onboarding through platforms like Protean eGov Technologies Ltd helped in seamless contribution tracking, and regulatory stability. This made early, long-term investing more accessible for young parents.

Main Benefits: Why NPS Vatsalya Outshines Traditional Savings

Initially, Meera, Aarav’s mother had considered fixed deposits and child education plans.

However, when she looked at the projection, they told a different story.

Fixed-income instruments struggled to outperform inflation over long periods. But the NPS Vatsalya scheme offered controlled equity exposure, which is essential for real wealth creation.

Also, one of the most important advantages was cost efficiency. NPS fund management charges are among the lowest in the Indian investment landscape. Lower fund management costs meant more of Aarav’s money stayed invested and compounded over time.

The scheme also helped the parents develop financial discipline. They made monthly contributions. The limited withdrawal flexibility, and lifecycle-based investing reduced the risk of impulsive decisions.

For Rohan and Meera, this was not a limitation, but a safeguard for their child’s future.

Flexibility and Withdrawal Rules You Must Know

When Aarav was 14, he showed exceptional talent in robotics and qualified for an advanced international training programme.

Rohan was relieved to learn that NPS Vatsalya allows partial withdrawals for specific purposes such as education, medical treatment of specified illnesses, or disability, subject to PFRDA norms.

This balance between flexibility and long-term commitment is a defining feature of the scheme. It ensures funds are available for genuine developmental needs while protecting the investment’s compounding potential.

Once Aarav turns 18, the account can transition into a regular NPS account in his name, subject to fresh KYC within three months. He will then have the option to continue contributions, adjust asset allocation, and align the investment with his own career and financial goals, turning childhood planning into lifelong financial discipline.

Conclusion

Rohan and Meera’s story is simply about the importance of time.

NPS Vatsalya is designed for parents who understand that time is the most valuable financial asset a child can have. You can start early, invest regularly, and trust a regulated, low-cost system to transform your modest contributions into compounded wealth.

In an age where future costs are uncertain, NPS Vatsalya offers a certain process, disciplined structure, and the power of compounding. Thus, building a substantial corpus, such as ₹10 crore over the long term, becomes possible through disciplined contributions and compounding.

Frequently Asked Questions

Q1: What is NPS Vatsalya and how does it work?

NPS Vatsalya is a minor-focused National Pension System account that allows parents to invest systematically for their child’s long-term financial future.

Q2: Is NPS Vatsalya safe and regulated?

Yes. The scheme is regulated by PFRDA and follows the same governance and investment standards as NPS.

Q3: Can parents withdraw money before the child turns 18?

Partial withdrawals are allowed for defined purposes such as education, medical needs, or skill development, as per PFRDA guidelines.

Q4: What happens when the child becomes an adult?

At 18, the account converts into a standard NPS account in the child’s name, allowing continued long-term investing.

Q5: Why choose NPS Vatsalya over other child investment options?

NPS Vatsalya effectively combines low costs, disciplined investing, market-linked growth, and regulatory oversight. This makes it a strong foundation for long-term child wealth creation.