The updated NPS withdrawal rules have transformed retirement planning in India. The Pension Fund Regulatory and Development Authority (PFRDA), in its December 2025 amendments, introduced a new rule allowing up to an 80% lump sum NPS withdrawal for non-government subscribers.

This change in NPS withdrawal rules comes with important tax caveats and strategic choices. Here is how to explain this game-changing NPS update to employees who step into retirement. Let’s learn how a successful NPS withdrawal requires careful consideration of long-term financial health.

Breaking Down the New 80:20 Exit Strategy

Here is a bifurcation of the new 80:20 NPS exit strategy.

For Non-Government Subscribers

Non-government subscribers with a corpus above ₹12 lakh have a lower mandatory annuity requirement (now 20%). Thus, retirees retain control over a larger portion of their hard-earned money.

For Government Subscribers

Generally, government employees follow a different structure necessitating a 40% annuity purchase unless their corpus falls below specific thresholds.

Lump Sum vs Staggered Post-Retirement Payout

The new NPS withdrawal rules help subscribers choose between a one-time lump sum and a staggered payout. With this flexibility, individuals can handle their immediate post-retirement expenses effectively. Thus, NPS investors are not forced to rely on predetermined pension streams. Their NPS withdrawal decision can be flexible (based on their accumulated amount).

Employees need to evaluate the net benefit of a higher lump sum compared to the tax liability. The NPS withdrawal rules provide the option for more cash, but the tax burden might reduce the actual usable amount.

Smart Alternatives to a Single Massive Payout

Retirees might face the dilemma of how to handle a large sudden influx of cash. Here are a few points for them to consider.

The Systematic Lump-sum Withdrawal (SLW)

With SLW, a subscriber can periodically withdraw the lump sum portion, instead of a one-time exit. Thus, retirees can have a steady income while the remaining funds can stay invested in the market.

Staying Invested Until Age 85

With the updated NPS withdrawal rules, individuals can remain invested until the age of 85. This is a longevity benefit for employees who possess other sources of income at age 60. Investors’ deferred NPS withdrawal can help their retirement corpus to compound in a tax-deferred environment for an additional 25 years.

The New SUR Facility

With the new Systematic Unit Redemption (SUR) facility, units over a minimum period of six years can be redeemed. Here, those with a corpus between ₹8 lakh and ₹12 lakh can benefit, by avoiding mandatory annuities. Such structured withdrawals can provide a safety net against market volatility.

Tax Outgo Management

The SUR facility can help in the management of the tax outgo over several financial years rather than a single year. Any employee who does not need immediate liquidity can consider these sophisticated alternatives.

Guiding Employees Through the Final Exit Process

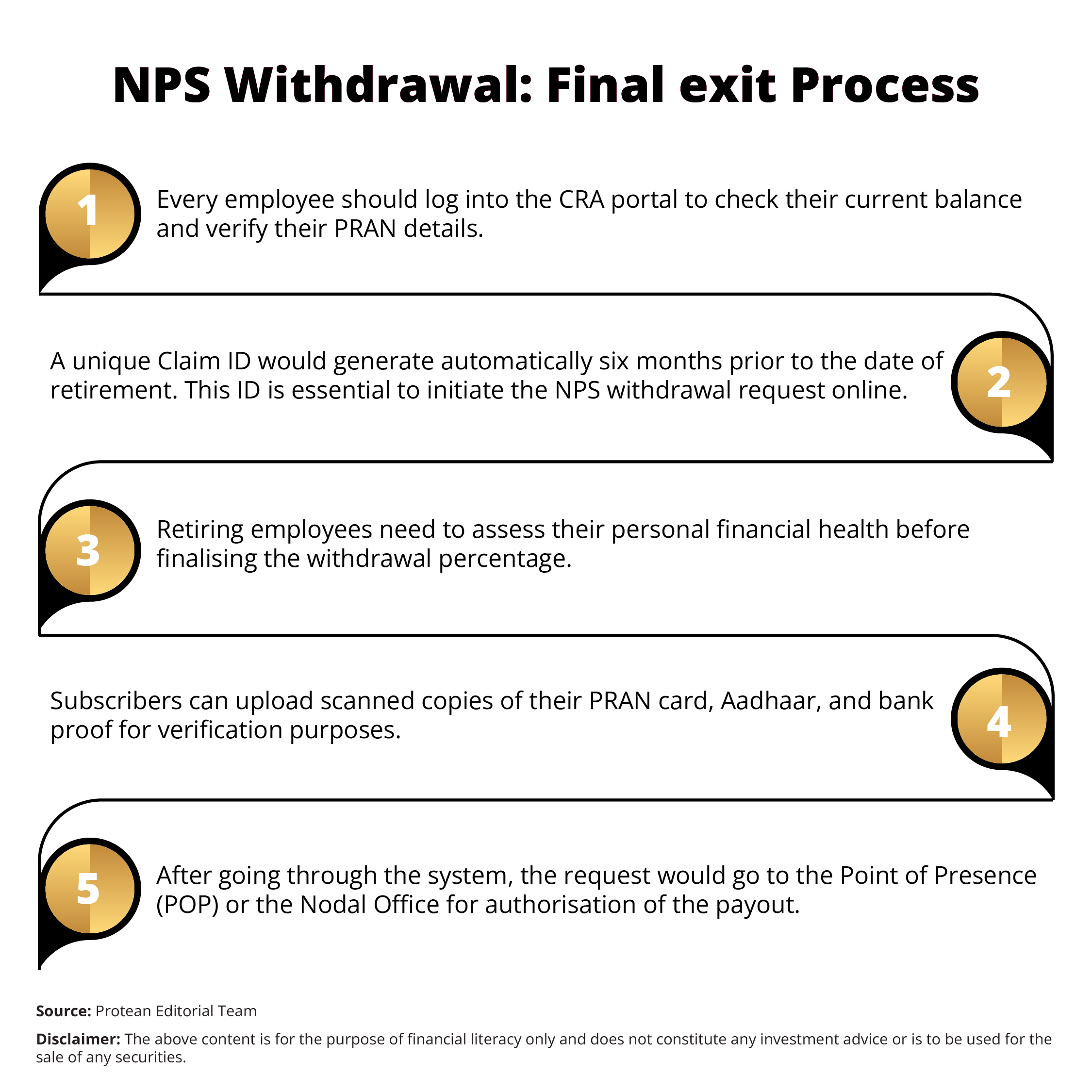

After thoroughly understanding the new NPS withdrawal process, investors should seek a clear understanding of the digital interface provided by Protean eGov Technologies.

Conclusion

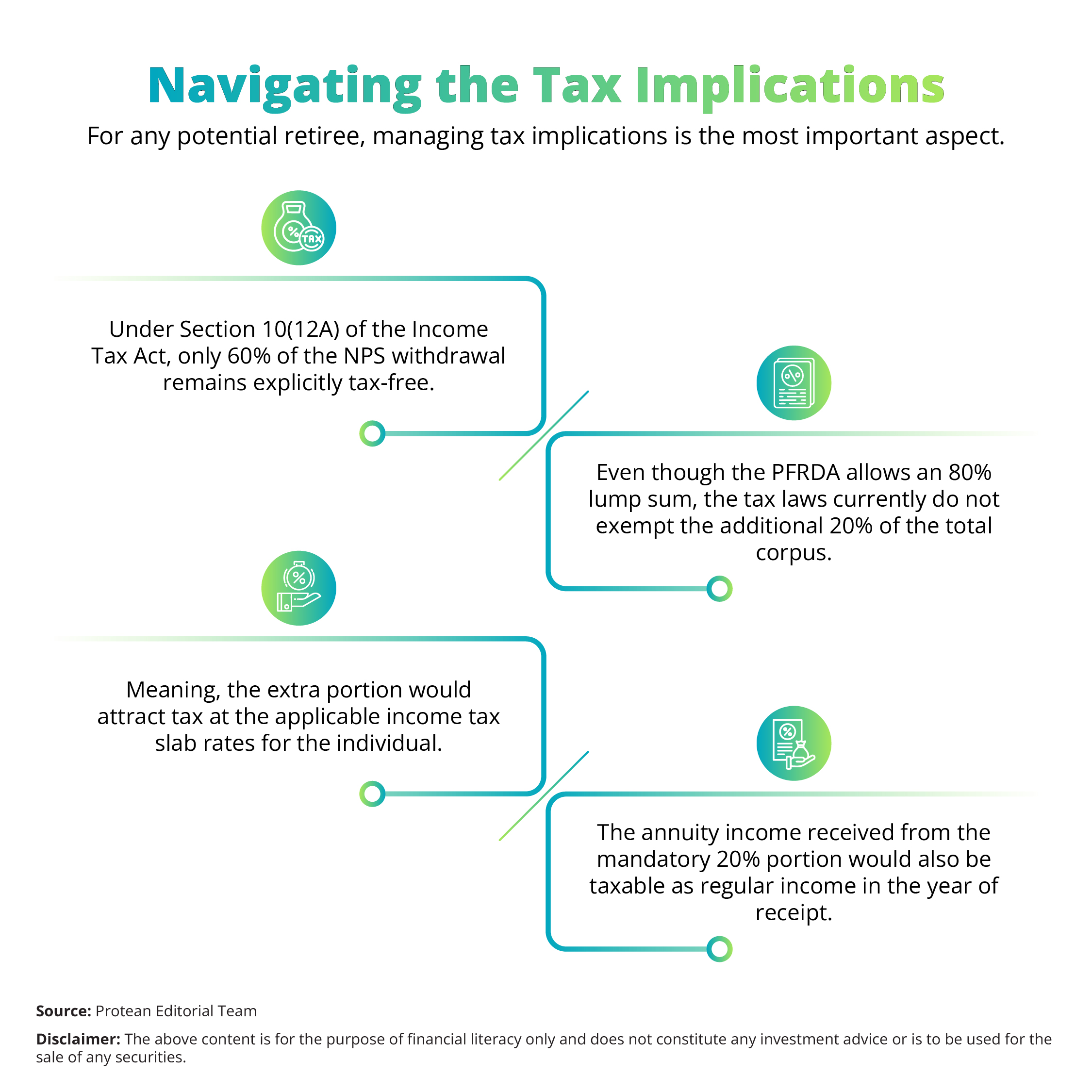

The updated NPS withdrawal rules can offer non-government employees flexibility by unlocking up to 80% of their retirement corpus. However, without proper planning, the tax hit on the extra 20% could become a burden.

Every individual possesses unique financial needs, and the NPS system is now accommodating those diverse requirements. Thus, NPS is gradually evolving by becoming subscriber-centric. It is also transforming the retirement landscape in India.

Are you preparing for retirement? Log into your CRA portal today and view your corpus size to develop your perfect exit strategy. A smooth NPS withdrawal can begin with informed decision-making and a clear vision for the future.

Frequently Asked Questions (FAQs)

Q1: Can a government employee withdraw 80% as a lump sum?

Generally, government employees need to use at least 40% of their corpus for an annuity. The 80% rule applies to the non-government sectors like the ‘All Citizen Model.’

Q2: Is the SLW option mandatory for all retirees?

No. The Systematic Lump-sum Withdrawal is an optional facility for those preferring regular payouts over a one-time lump sum at the time of exit.

Q3: Has the tax exemption limit increased to 80% in 2026?

No. The tax-free limit under Section 10(12A) remains at 60% of the total corpus despite the increase in the withdrawal limit by the PFRDA.

Q4: How many partial withdrawals are permitted before retirement?

A subscriber can make up to four partial withdrawals for specific reasons like education, marriage, or house construction after three years of participation.