Are you looking for NPS retirement planning benefits on the internet? Here is a magic number for investors to consider in 2026 to transform their retirement planning.

Retirement planning in India has now become more flexible than ever. In December 2025, the Pension Fund Regulatory and Development Authority (PFRDA) introduced transformative amendments.

These changes completely overhauled the NPS withdrawal framework. So, for 2026, the amount of ₹8 Lakh can stand out as the ultimate magic number for every National Pension System (NPS) investor.

Let’s understand how this figure could serve a dual purpose for your financial future. Let us learn how the crucial liquidity provided by the 100% corpus exit and high-income tax deductions efficiency works.

Withdrawing Your Entire Corpus Without Annuities

Here is the landmark rule change in NPS and its impact on your retirement planning goals.

100% Withdrawal Flexibility

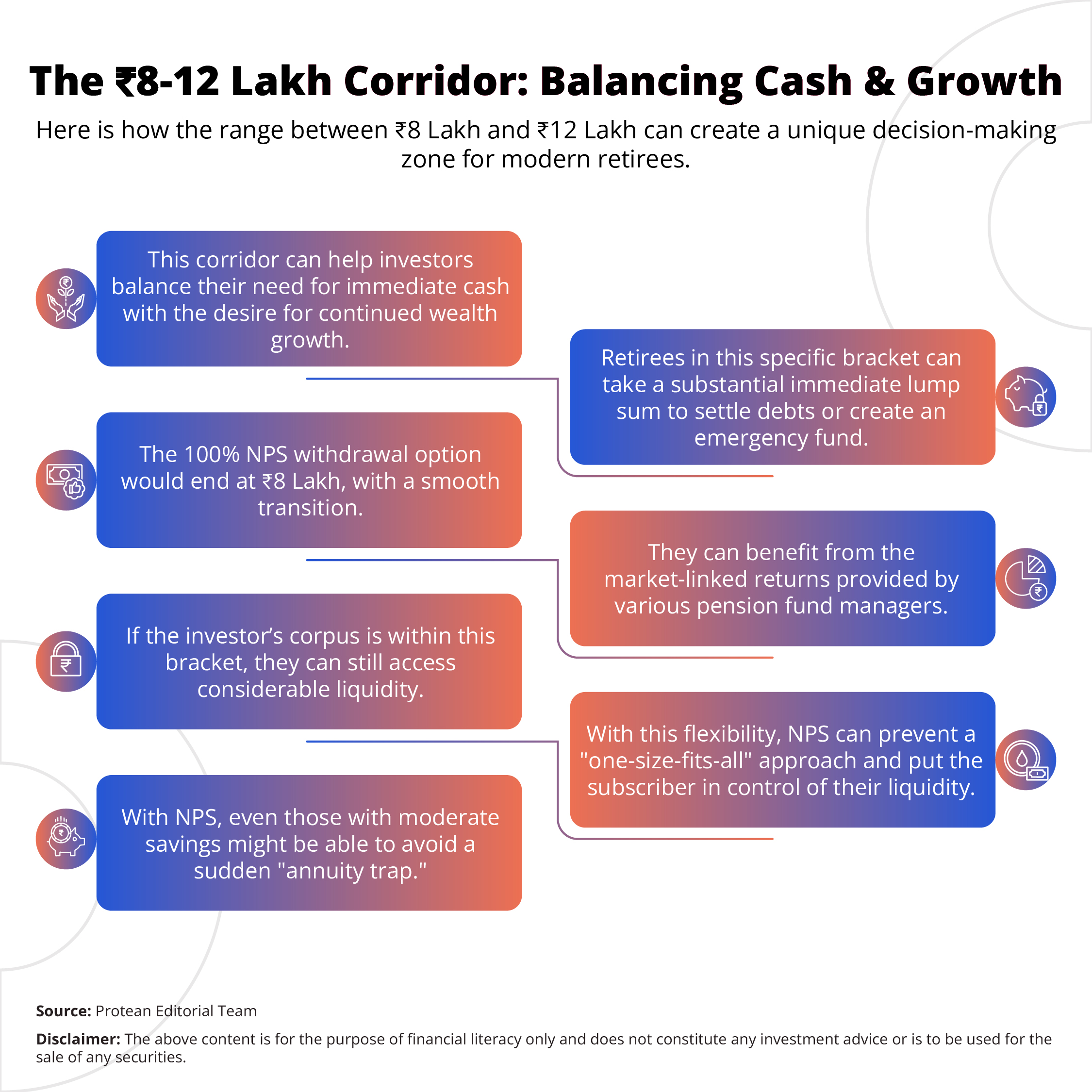

Investors can withdraw their accumulated pension wealth as a lump sum without having to purchase an annuity. The condition for this flexibility is the total corpus staying at or below ₹8 Lakh for non-government subscribers. With the 100% NPS withdrawal flexibility, individuals can utilise their full savings for major life events such as home renovations, medical costs, or children's weddings.

The New Limit

The new NPS withdrawal limit can provide investors with immediate financial freedom. So, when a corpus crosses this specific threshold, the NPS investment dynamics can shift. Also, now, non-government subscribers with a corpus >₹12 Lakh can choose an 80:20 split. Meaning, an NPS subscriber can take up to 80% as a lump sum, and 20% will be used to buy an annuity for post-retirement financial security.

Strategising ₹8 Lakh in Deductions for High Earners

Here is how the number ₹8 Lakh can also become the magic target for high earners with annual salaries above ₹20-25 Lakh.

The Unique Advantage

High-income professionals might struggle to determine whether the Old Tax Regime or the New Tax Regime could offer better savings.

- Now, a taxpayer would typically require roughly ₹8 Lakh in total deductions to make the Old Tax Regime more beneficial.

- With the National Pension System investors can gain a unique advantage in this calculation.

- The exclusive ₹50,000 deduction under Section 80CCD (1B) can be the important missing piece for high-income earners.

A Tax-Saving Blueprint

Here is how the NPS ₹8 Lakh total deduction target can be a high-salaried investor’s tax-saving blueprint.

- Investors can start with the ₹50,000 standard deduction available to all salaried employees.

- They can add the ₹1.5 Lakh limit under Section 80C. This usually includes their provident fund and life insurance.

- Next, they can incorporate up to ₹2 Lakh for home loan interest under Section 24(b) and any applicable House Rent Allowance (HRA).

- Finally, their voluntary contribution to the National Pension System Tier- 1 can provide that extra ₹50,000 push.

- With this combination, high-income earners can reach the ₹8 Lakh deduction target to optimise their tax outgo.

Here, the National Pension System can be the unique investment vehicle offering this specific additional deduction.

As a Central Recordkeeping Agency (CRA), Protean eGov Technologies Ltd. can provide the digital infrastructure for seamless transactions.

Conclusion

The National Pension System investing in 2026 has transformed it into a more flexible retirement vehicle for Indian investors. Here, the investor stays at the driver’s seat, whether aiming for the ₹8 Lakh liquidity floor for a full withdrawal or using NPS contributions to help hit an overall ₹8 Lakh tax deduction target.

The ability to take a 100% NPS withdrawal even for a smaller amount might provide greater financial security. Meanwhile, with the enhanced lump sum options for larger corpuses the subscriber’s retirement can be comfortable and self-funded.

Review your current contributions to see if you hit the magic number. Open an account today to leverage the power of compounding and achieve financial security.

Frequently Asked Questions (FAQs)

Q1: Can I withdraw my entire NPS corpus if it is exactly ₹8 Lakh?

Yes. As per the latest PFRDA amendments a 100% NPS withdrawal as a lump sum is allowed upon normal exit (age 60 or superannuation) if the total accumulated wealth is ₹8 Lakh or less.

Q2: How does the ₹8 Lakh deduction target help in tax planning?

For high earners, reaching ₹8 Lakh in total deductions can make the Old Tax Regime more beneficial than the New Tax Regime. With NPS Tier 1, there is an exclusive ₹50,000 deduction to help investors reach this goal.

Q3: What is the new rule for corpuses above ₹12 Lakh?

Non-government subscribers, with a corpus exceeding ₹12 Lakh, can now make a lump sum NPS withdrawal of up to 80% upon normal exit or retirement. The remaining 20% needs to be used to purchase an annuity.

Q4: Is the ₹50,000 NPS deduction part of the ₹1.5 Lakh 80C limit?

No. The deduction under Section 80CCD(1B) for NPS Tier 1 is an additional benefit. It is separate from and over and above the ₹1.5 Lakh limit of Section 80C.