The National Pension System is a flexible, long-term retirement wealth creator of the modern financial age.

It offers a dual-account structure defining this unique financial vehicle.

- The NPS tier 1 focuses on disciplined retirement savings.

- The NPS tier 2 functions as a flexible, unsung hero of the entire wealth creation process.

The NPS tier 2 is a voluntary investment platform with high liquidity. The NPS account can be a powerful wealth creation tool beyond traditional pension planning. Here’s how NPS Tier 2 provides a bridge between liquid savings and long-term growth.

The Cost-Effective Wealth Builder

Here are the main benefits of NPS tier 2 investing.

- Institutional Fund Management Fees - The fund management charges in the National Pension System are one of the lowest across the world.

- Minimal Expense Ratios - A lower expense ratio can lead to a considerably higher wealth accumulation over several years. With this structural advantage, more capital can participate in market growth.

- No Exit Loads - The NPS tier 2 structure has no exit fees eating into the retail investors’ returns.

- Efficient Compounding - There can be more efficient compounding when transaction costs stay at a minimum level. Over the long-term, this difference in fees can create a huge gap in the final corpus value.

- Transparency of Portfolio - Investors can refer to the detailed statements to know exactly where the money goes.

- Standardised Charge Structure - NPS subscribers can benefit from institutional-grade investment management without the high retail price of private wealth services.

Strategic Asset Allocation

With the NPS tier 2 account, subscribers can choose between Equity (E), Corporate Bonds (C), and Government Securities (G).

- The ability to switch between asset classes might help seek safe harbors during high market volatility.

- Subscribers can select "Active Choice" to manually decide the allocation percentage for each category.

- With the "Auto Choice" option, subscribers can select a lifecycle-based approach automatically shifting risk with the investor’s maturity.

- Investors can switch fund managers or asset ratios to align with changing financial stages throughout their career.

- NPS tier 2 subscribers can diversify across debt and equity, building a robust portfolio to withstand economic shifts.

- Investors can check the tier 2 NPS dashboard for daily updates on the NAV and performance of different asset classes.

How to Activate Tier 2 NPS Account

Active tier 1 NPS subscribers can activate their tier 2 NPS using a simple online process. Here are the steps.

- Access the official Protean eGov Technologies CRA portal using existing login credentials and PRAN.

- Locate the "Activate Tier 2" link within the main account dashboard.

- Investors can make a minimum initial contribution (₹1000) to get started.

- Subscribers can verify bank details for seamless future transfers and withdrawals.

- With instant activation, the digital formalities conclude and the payment succeeds.

- Investors can set up periodic contributions in their NPS account portal, automating the savings process.

NPS Tier 2 Monitoring & Management

The tier 2 NPS comes under the robust regulatory framework under the Pension Fund Regulatory and Development Authority (PFRDA). Thus, the Tier 2 NPS account’s regulatory oversight ensures that the fund managers comply with strict investment guidelines.

- The NPS subscriber can track their Net Asset Value (NAV) on a daily basis via the mobile app or the website.

- Central Recordkeeping Agencies (CRAs) like Protean eGov Technologies maintain records with high security and accuracy.

- With the NPS tier 2, subscribers can nominate beneficiaries similar to a standard bank account.

- The flexibility of the NPS tier 2 extends to the choice of the Pension Fund Manager (PFM). Investors can choose from several top-tier financial institutions to manage their funds.

- Subscriber can move their capital to another Pension Fund Manager (PFM) once per financial year.

Conclusion

The tier 2 NPS is a rare combination of low costs, high liquidity, and market-linked returns. It is, thus, a hidden gem for investors seeking to build wealth without the burden of high fees. A disciplined approach to the NPS account can yield significant financial freedom over the medium term.

Open the tier 2 NPS dashboard today to take full control of the investment journey. Wealth creation becomes a simple and transparent process with the right investment tools in place.

Frequently Asked Questions (FAQs)

Q1: Can a subscriber withdraw from an NPS Tier 2 account anytime?

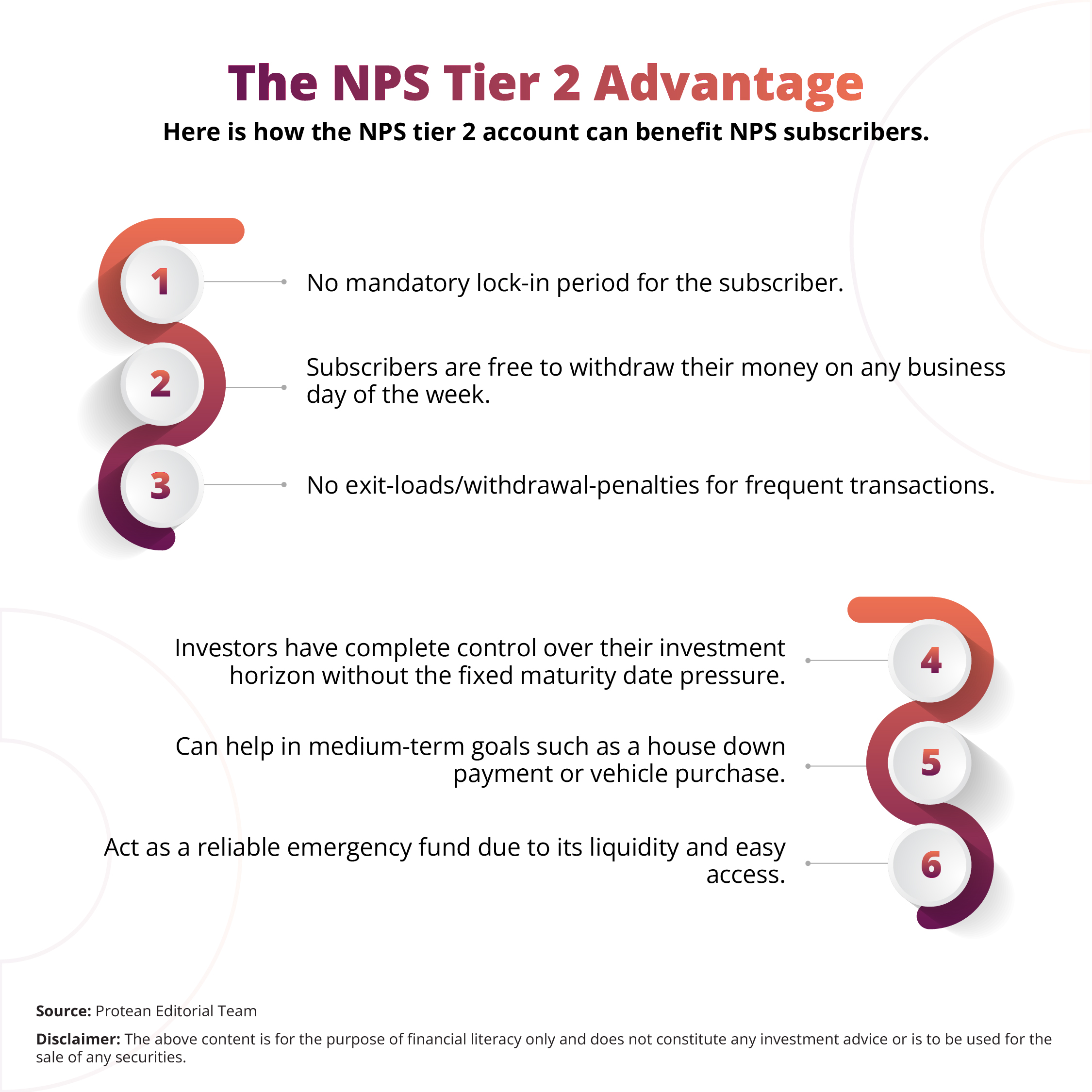

Yes. An NPS tier 2 account has no lock-in period. It permits withdrawals on any business day. The funds usually reach the bank account within a few working days.

Q2: What is the tax treatment for Tier 2 gains?

The NPS tier 2 gains attract tax according to the subscriber’s income tax slab. This account doesn’t provide the same tax deductions as the Tier 1 NPS account.

Q3: What are the minimum investment requirements for Tier 2?

Tier 2 NPS account requires a ₹1000 minimum opening investment. There is no mandatory annual minimum for Tier 2 (unlike Tier 1). However, the account stays active as long as the Tier 1 account is active.

Q4: Can I choose different fund managers for Tier 1 and Tier 2?

Yes. Investors can choose different fund managers for both, tier 1 and tier 2 NPS accounts. Subscribers have the freedom to pick Asset Allocation (E, C, and G) independently for both accounts, though Asset Class A is exclusively available only for Tier 1.