What are the important features of MSF (Multiple Scheme framework) strategy? Let us find out more about MSF and the NPS scheme.

NPS (National Pension System) has always been a landmark retirement planning instrument for non-government employees. The recent regulatory amendments introduced by the PFRDA (Pension Fund Regulatory and Development Authority) have fundamentally reshaped how you manage your long-term savings.

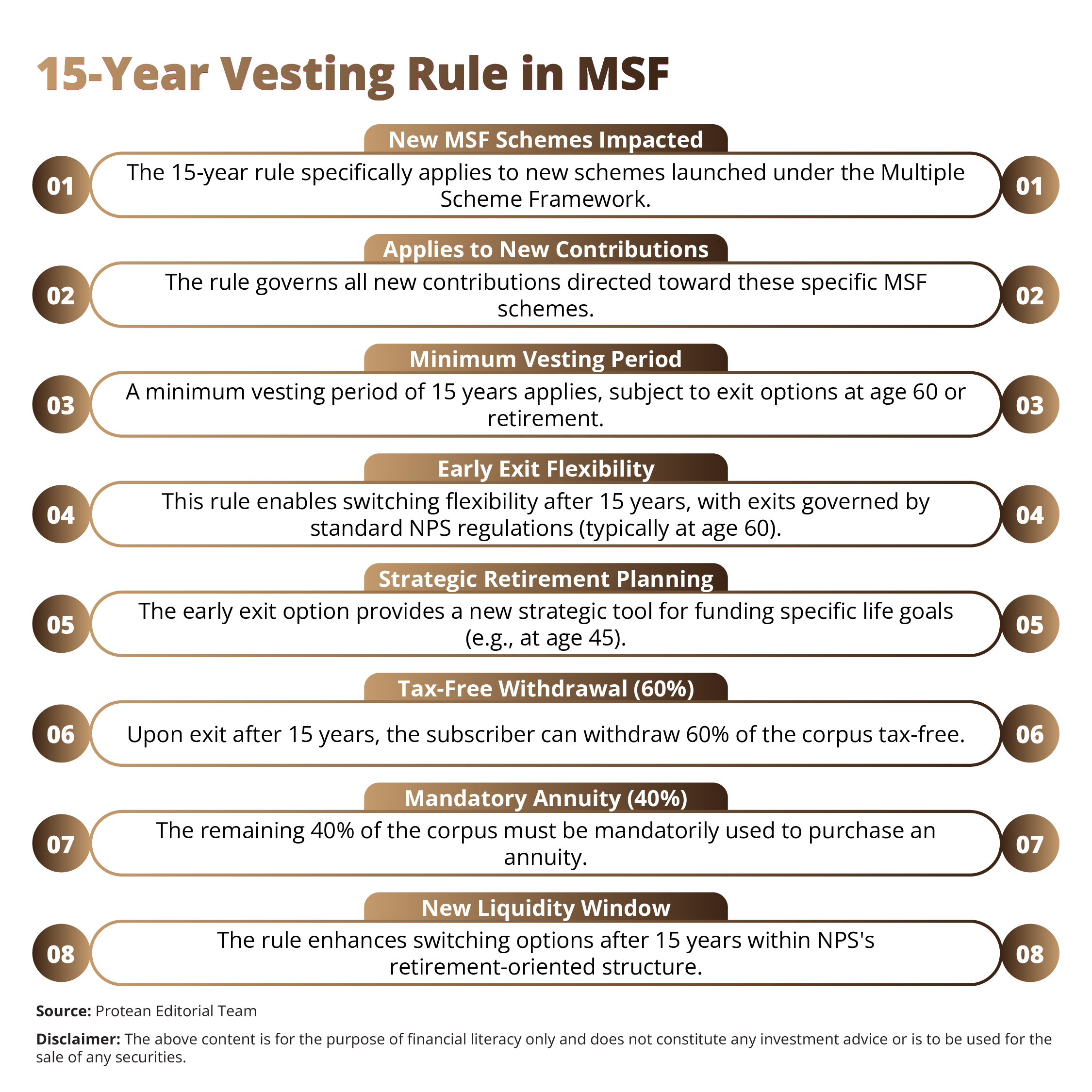

The Multiple Scheme Framework introduces a 15-year vesting period for switching between MSF schemes in both Tier I and Tier II accounts. This requires a strategic re-evaluation of your entire NPS scheme portfolio.

Thus, it is important to understand these changes to maximise the tax and growth potential of your NPS investing. Here’s more information on the MSF 15-year vesting period for scheme switching and its applicability to Tier II accounts.

15-Year Vesting Rule: A New Window of Opportunity

One of the most talked-about changes under MSF is the minimum vesting period. The new 15-year rule would directly affect schemes launched under the MSF umbrella.

- Vesting Period Defined - The schemes launched under the MSF now come with a minimum vesting period of 15 years. The vesting rule is applicable to all new contributions made to these schemes.

- The Early Exit Option - This introduces a major point of liquidity in NPS scheme investing. If you invest in one of these new NPS scheme options, you can switch between MSF schemes after completing 15 years of participation or at normal exit (age 60 or retirement).

- Withdrawal Implications - Premature exit norms apply for withdrawal before age 60, even after 15 years vesting (e.g., at age 45). For premature exit before age 60, you can withdraw up to 20% tax-free as a lump sum, with at least 80% mandatorily used for an annuity. This early access can prove to be a new strategic tool for investors planning for specific life events.

Tier II and the Evolving Role in the MSF Ecosystem

In subtle ways, the multiple scheme framework has redefined the role of the NPS Tier II account. Tier II remains the voluntary savings account within the new pension scheme. It has a primary advantage of high liquidity with no lock-in period, which remains intact.

The most important change is that the MSF applies to both:

- Tier I (mandatory retirement savings)

- Tier II (voluntary savings) accounts

Meaning, you can gain the benefit of scheme diversification and the potential for a 100% equity allocation in your Tier II account as well.

Tier I is the primary vehicle for tax-advantaged retirement savings. However, now, Tier II continues to serve as a low-cost, liquid investment vehicle, enhanced by MSF options and comparable to many mutual funds.

Subscribers can use Tier II for additional investments, leveraging MSF for diversified, long-term strategies. Thus, they can utilise the new, high-growth, 100% equity schemes without the long lock-in of the Tier I account.

Asset Allocation New Rules: Unlocking 100% Equity

The freedom to allocate up to 100% of fresh contributions to equity schemes for non-government subscribers is the most revolutionary change introduced under the MSF.

This can completely transform the NPS scheme into a far more competitive investment tool for younger investors and those with a high-risk appetite.

Now PFMs (Pension Fund Managers) can offer specific "High-Risk" variants under the multiple scheme framework to facilitate this higher equity exposure. There are two ways in which this structural change fundamentally alters your NPS investing approach:

Tailored Risk Profiles

Now, a young subscriber starting their career can commit a full 100% of their future contributions to equity for the first 15 to 20 years. Thus they can capitalise fully on the power of compounding. This high-risk approach is ideal for investors with a long-term horizon.

Modular Portfolio Construction

With MSF, investors can hold multiple schemes simultaneously under your single PRAN (Permanent Retirement Account Number). You can seamlessly blend conservative and aggressive strategies.

Investors can adopt this modular approach for sophisticated, customised asset allocation that aligns perfectly with your individual life stage and financial goals.

The PFRDA has now emphasised the need for mutual agreement between the employer and the employee regarding the choice of Pension Fund Manager and the specific investment schemes.

Conclusion

The structural changes brought about by the Multiple Scheme Framework and its 15-year vesting rule have transformed MSF investing within NPS. These reforms have transformed the NPS into a flexible, powerful, and modern investment tool.

With MSF, NPS investing is defined by choice, personalisation, and the potential for maximised growth (via 100% equity contribution).

Thus, investors can effectively manage risk, align portfolio with financial goals, and ultimately build a larger retirement corpus than was possible under the previous rules.

Frequently Asked Questions

Q1: Does the 15-year rule apply to my existing NPS corpus?

No, the minimum 15-year vesting period only applies to fresh contributions made to the new schemes launched under the Multiple Scheme Framework (MSF).

Q2: Can I switch between two different MSF schemes before the 15-year period is complete?

No. Switching from a new MSF scheme back to an existing "Common Scheme" is permitted, but free switching between two MSF schemes is only allowed after completing 15 years or upon normal exit.

Q3: Does the 100% equity cap apply to my entire NPS portfolio?

No. The option for up to 100% equity allocation only applies to the High-Risk variants of the new schemes available under the MSF. The total allocation is restricted to new funds you choose to direct into those specific schemes.