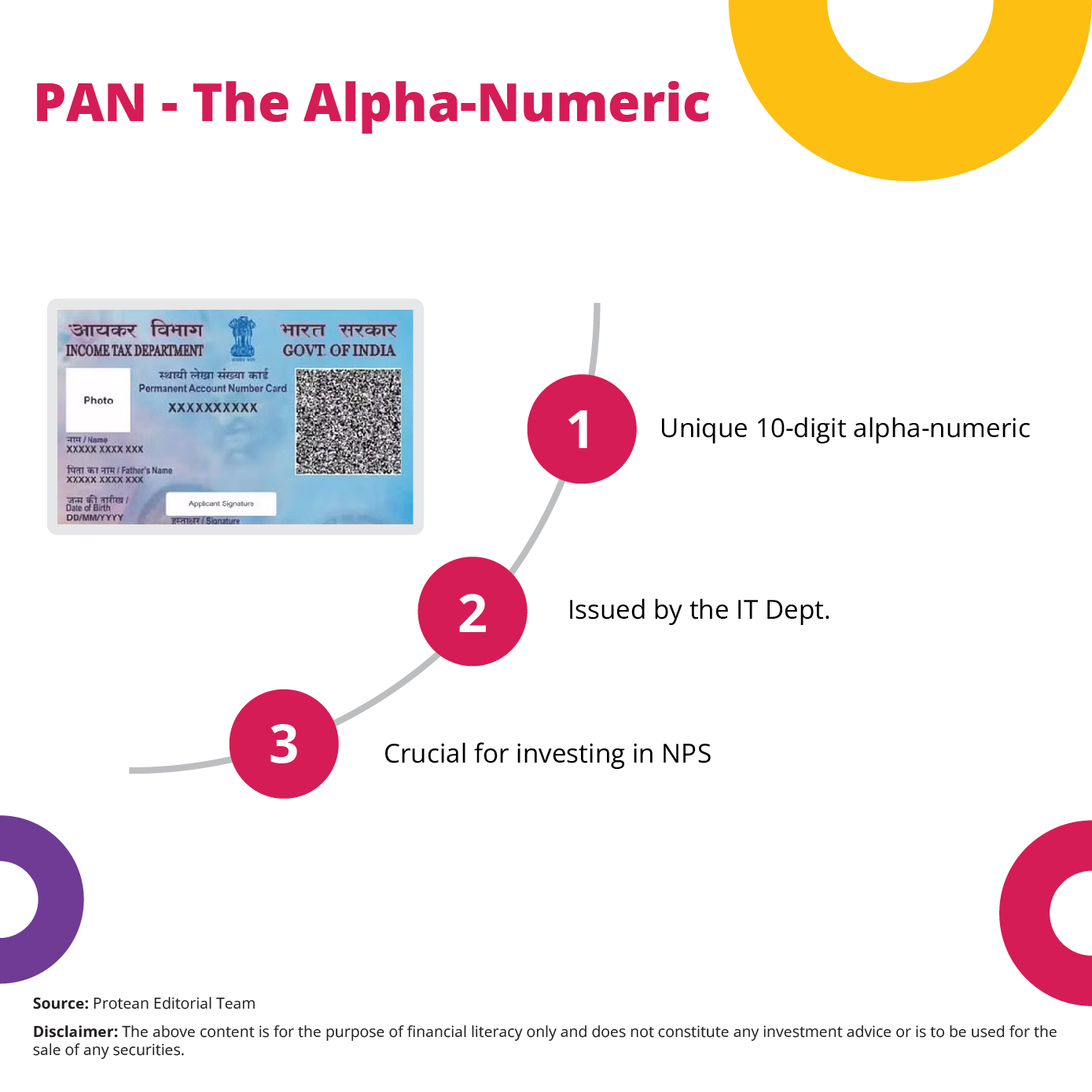

What comes to your mind when you hear PAN? You might be thinking about taxes, right? The Permanent account Number or PAN is one of the cornerstones of the Indian tax system. It is simply a unique 10-digit alphanumeric number. This number is issued by the Income Tax Department.

What’s more about this Alpha-Numeric?

Here are 24 commonly searched questions on PAN and other related tax concepts. You can check answers to them to get the essential knowledge of effective tax planning and tax compliance in India.

| You can also go through our PAN guide for more information. |

1. What is Income Tax?

As the name suggests, income tax is tax imposed by the government on your income. Here, you can either be an individual or business entity in India. In either of these cases, your income can incur income tax as per the prevailing government norms for the financial year.

Income tax is one of the significant sources of government revenue. It is also an important source for funding public services and infrastructure development.

2. What is meant by Tax Deduction at Source?

So, what is TDS? Again, as the name suggests, Tax Deduction at Source (TDS) is a mechanism where the payer of income is legally obligated to deduct tax. The payer makes this deduction at the prescribed rates from the income payable to the payee. This deducted tax is deposited with the government.

The TDS process can ensure that tax liabilities are met promptly. It can also help the government streamline tax collection.

3. What is TDS?

TDS, as explained above, stands for Tax Deducted at Source. It is a crucial component of the Indian tax system, facilitating efficient tax collection and ensuring compliance.

4. Who is a specified employee?

The Income Tax (IT) Act defines an employee with salary exceeding a certain threshold as a specified employee. A specified employee is subject to specific tax deduction rules and regulations.

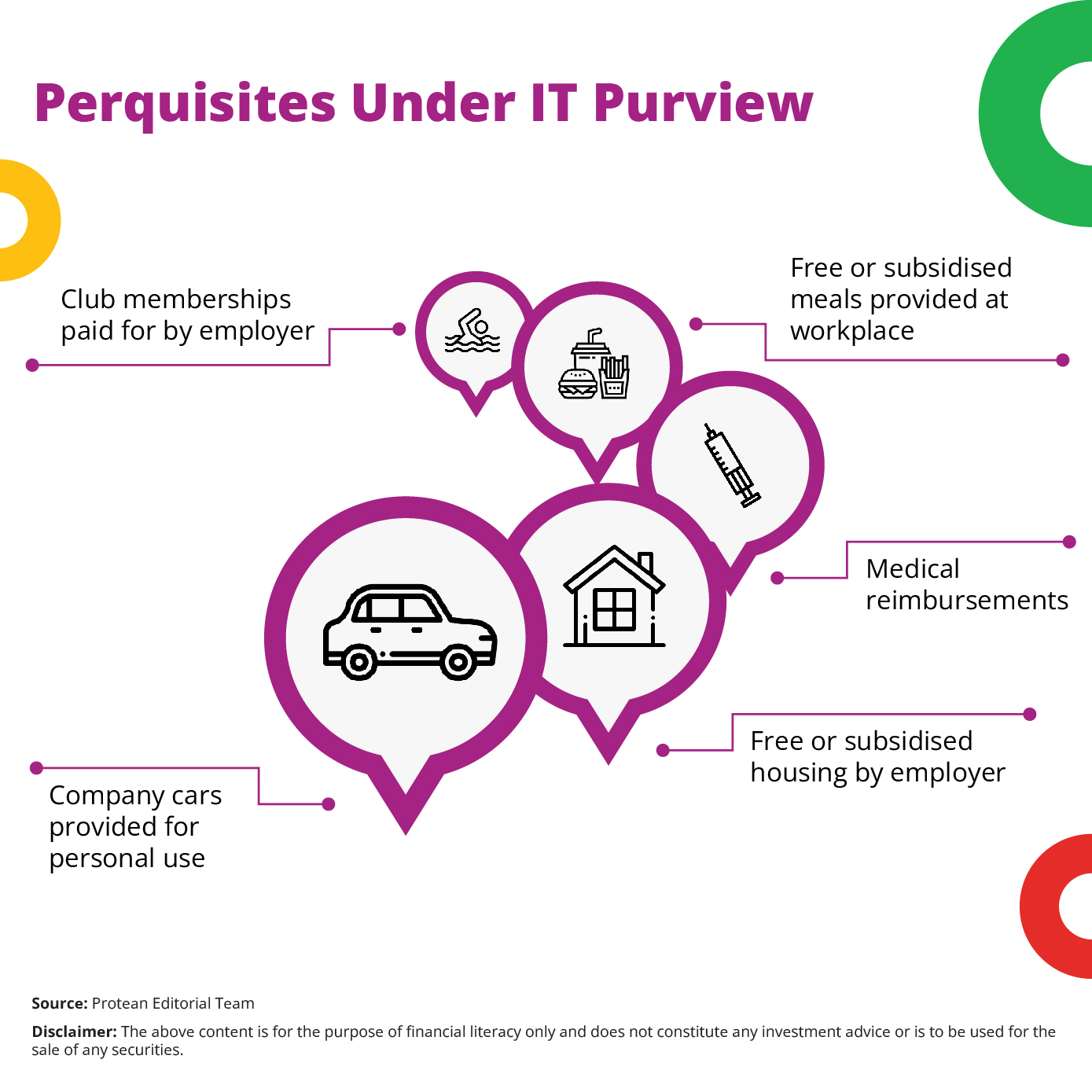

5. What are the number of Taxable prerequisites?

The number of taxable perquisites can vary depending on the specific nature of the benefits provided by the employer. However, common examples include company cars, subsidized meals, housing allowances, and other non-cash benefits.

6. What is the previous year in Income Tax?

In the context of Income Tax (IT) the "previous year" refers to the Financial Year (FY) preceding the Assessment Year (AY). For example, the previous year for AY 2024-25 would be FY 2023-24 i.e. April 1, 2023, to March 31, 2024.

7. What is Permanent Account Number (PAN)?

A Permanent Account Number or PAN is a unique ten-digit alphanumeric number. The IT Department issues a unique PAN to every individual and entity in India.

As explained in the intro, PAN serves as a unique identifier for all tax-related transactions. These can include filing IT returns, conducting financial transactions, and investing in various financial securities.

PAN is mandatory for NPS investments (especially for certain high-value transactions ₹50,000+), and it is mandatory to link it with Aadhaar to align with Section 139AA of the Income Tax Act.

| Read about the PAN creation process here. |

8. What do you mean by an Assessee?

The IT Act defines an assessee as any person who is by or under this Act liable to pay any tax or any other sum under this Act. An assessee can be an individual, business, trust, or other entities.

| Want to make corrections in your PAN? Learn how to make PAN card corrections here. |

9. What do you understand by Advance Payment of Tax?

Advance Tax is a mechanism where individuals and businesses are required to pay tax on their estimated income in advance. This advance tax is required to be paid in installments, throughout the financial year. This can help to ensure that tax liabilities are met in a timely manner. Advance tax can also help avoid a large tax burden at the end of the financial year.

Individuals can pay advance tax if their tax liability exceeds ₹10,000 in a financial year.

10. What do you understand by aggregation of income?

Aggregation of income is the process of combining income from different sources to determine the total taxable income of an individual or entity. This can include income from salary, business or profession, house property, capital gains, and other sources.

11. What are the kinds of perquisites?

Perquisites, or perks, are benefits provided by an employer to an employee in addition to their salary.

12. What is cost of improvement?

The cost of improvement refers to the expenditure incurred on enhancing or improving an asset (property). Examples for this can be the following:

- Renovating a house

- Adding extensions

- Upgrading machinery

All the three above would be considered costs of improvement.

13. What is Tax Planning?

Tax planning is a process wherein you can strategically structure your financial affairs from the tax lens. You can do tax playing to minimise your tax liability within the framework of the Income Tax law.

Here, you can identify tax deductions, exemptions, and credits, and make investment decisions that optimise your tax position.

An example of tax planning is investing in the National Pension System (NPS), which can be a part of effective tax planning.

14. How do you treat bad debt recovered earlier written off?

If a bad debt previously written off is recovered in a subsequent year, it is treated as income in the year of recovery. This is because the original write-off provided a tax benefit, and recovering the debt effectively reverses that benefit.

As per Section 41(1) of the Income Tax Act, recovered bad debts are taxable in the year of recovery.

15. What are listed and unlisted securities?

The securities that are traded on recognised stock exchanges are listed securities. Such securities are listed on exchanges (NSE - National Stock Exchange and BSE - Bombay Stock Exchange).

On the other hand, unlisted securities are typically held privately. Meaning, they aren’t listed on a stock exchange.

16. What is the Cost Inflation Index?

The Cost Inflation Index (CII) is an index used to adjust the cost of acquisition of assets for inflation while calculating long-term capital gains. This can help to ensure that the tax burden on long-term capital gains is not unduly impacted by inflation.

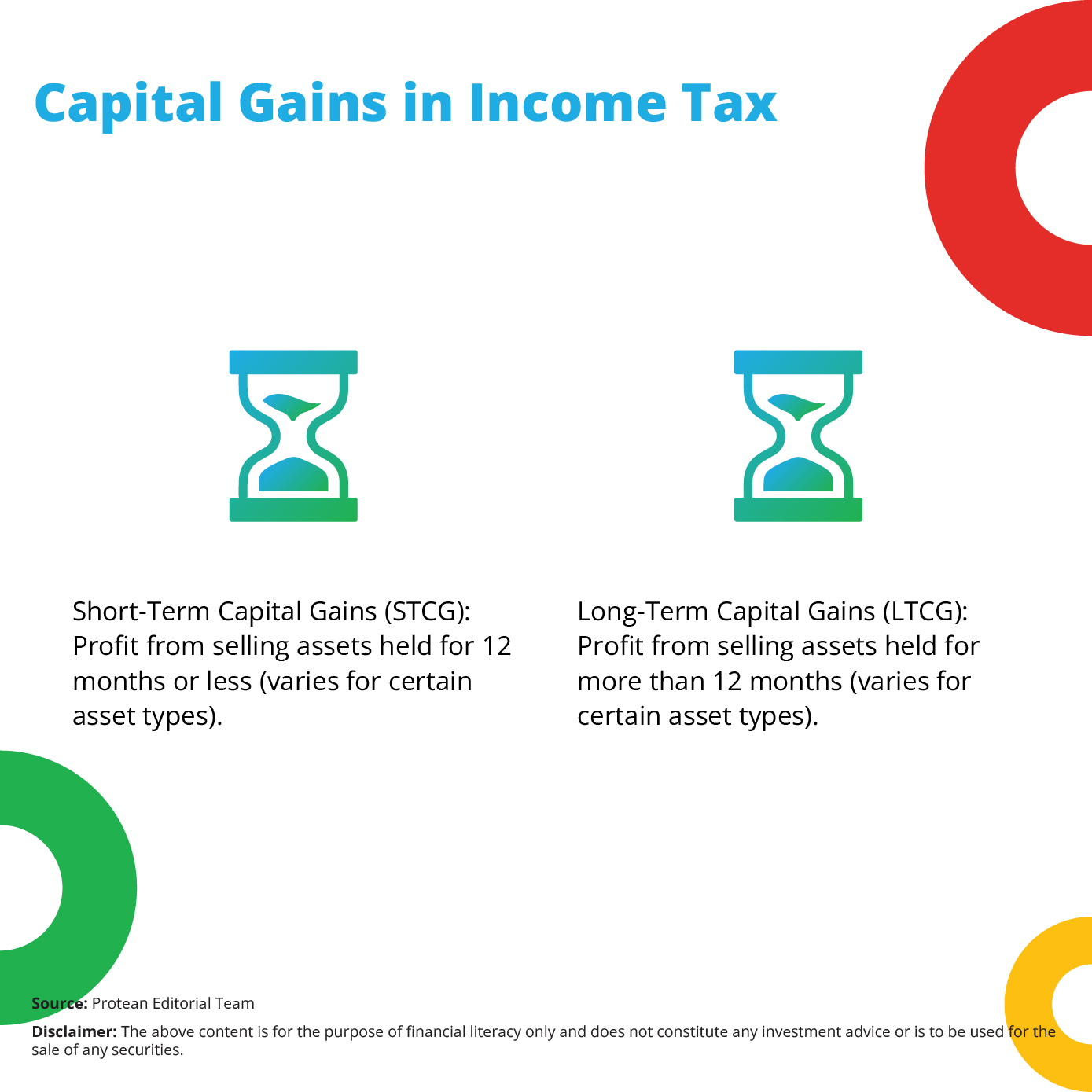

17. What is Capital Gain?

Capital gain is the profit realised from the sale or transfer of a capital asset. Capital assets include shares, bonds, real estate, jewellery, and other valuable assets.

18. What is the Cost of the Acquisition of capital assets?

The original or actual cost incurred for acquiring an asset is called cost of acquisition of a capital asset. Such cost can be incurred on any expenses for bringing the asset to its current condition. The cost of acquisition of capital assets can include the purchase price, brokerage fees, stamp duty, and other related expenses.

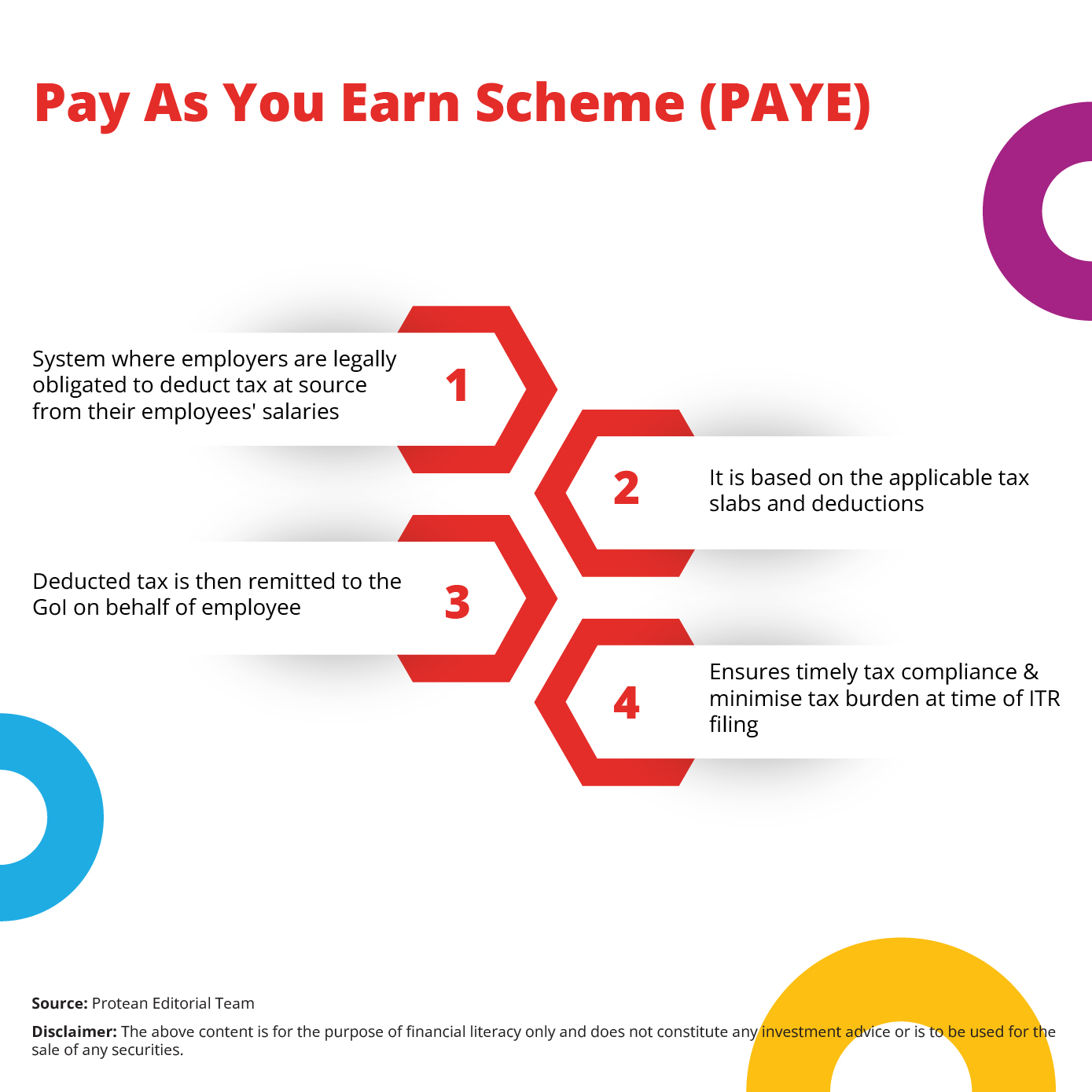

19. What do you understand by "Pay As You Earn" scheme?

The "Pay As You Earn" (PAYE) scheme is a system where employers are legally obligated to deduct tax at source from their employees' salaries based on the applicable tax slabs and deductions. The deducted tax is then remitted to the Government of India (GoI) on behalf of the employee. This can ensure timely tax compliance and minimise the tax burden at the time of income tax returns filing.

20. How would you determine taxable income from house property?

Taxable income from house property can be calculated as follows:

- Gross Annual Rent: This can include actual rent received or notional rent (if the property is self-occupied).

- Less: Allowable Deductions:

- Municipal taxes paid

- Interest paid on home loans

- Standard deduction (if applicable)

- Taxable Income from House Property: The resulting amount after deducting allowable expenses.

Let us look at this numerical example to understand this better:

- Property Type: Say, this is a rented-out property.

- Gross Annual Rent: ₹3,00,000 (This is the total rent received over the year)

- Municipal Taxes Paid: ₹10,000

- Interest Paid on Home Loan: ₹1,20,000

- Standard Deduction: In India, the standard deduction for house property is 30% of the Gross Annual Rent. So, 30% of ₹3,00,000 = ₹90,000

Here is the detailed calculation:

- Gross Annual Rent: ₹3,00,000

- Less: Allowable Deductions:

- Municipal Taxes: ₹10,000

- Interest on Home Loan: ₹1,20,000

- Standard Deduction: ₹90,000

- Total Deductions: ₹10,000 + ₹1,20,000 + ₹90,000 = ₹2,20,000

- Taxable Income from House Property: ₹3,00,000 (Gross Annual Rent) - ₹2,20,000 (Total Deductions) = ₹80,000

Therefore, the taxable income from house property in this example is ₹80,000. This is the amount that will be considered while calculating your total income and tax liability as per the example.

| You can learn more about such tax concepts here. |

21. What are short-term capital assets?

Short term capital assets are assets that are held for a period of less than the prescribed holding period, which is generally 12 months for most assets.

22. What is meant by Tax Deduction at Source?

TDS is a mechanism where the payer of income is legally obligated to deduct tax at the prescribed rates from the income payable to the payee and deposit it with the government. This ensures that tax liabilities are met promptly and helps the government streamline tax collection.

23. What is the importance of PAN in investing with NPS?

PAN is crucial for investing in the National Pension System (NPS). It is mandatory to provide your PAN while opening an NPS account and for all subsequent transactions related to your NPS investments. PAN is used to track your contributions, calculate tax benefits, and ensure compliance with tax regulations.

PAN is mandatory for NPS Tier I & Tier II accounts under Rule 114B of Income Tax Rules.

| Learn about opening NPS account here. |

24. Can I link my Aadhaar card to my PAN online?

Yes, you can easily link your Aadhaar card to your PAN online through the Income Tax Department's official website or through the dedicated online portal. Linking your Aadhaar with your PAN is mandatory for various tax-related activities, including filing income tax returns.

Linking PAN-Aadhaar is mandatory for filing ITR under Section 139AA. Non-linking attracts a ₹1,000 fee.

| Learn more about linking PAN with Aadhaar here. |

Conclusion

It is essential to understand these key concepts related to PAN and the Indian tax system. This applies equally to individuals as well as business entities. You can familiarise yourself with these concepts and adhere to tax regulations. With this, you can ensure tax compliance, minimise your tax liabilities, and effectively plan your personal finances.

Also read:

PAN 2.0 FAQ: All Your Questions Answered

PAN for Everyone: Application Processes for Individuals, Minors, NRIs, HUFs and Trusts

PAN 2.0: 10 Key FAQs About India's New Single Portal for PAN/TAN Services (Government Release)

PAN for Everyone: Application Processes for Individuals, Minors, NRIs, HUFs and Trusts

Story by Bruhadeeswaran R.

Bruhadeeswaran has 15+ years of experience as a content strategist, communication, and editorial professional. Currently, he is leading an innovative content development process, translating complex B2B products into engaging, user-friendly narratives.