Planning for retirement may seem like a distant worry when you’re in your 30s or 40s, busy building a career and juggling daily expenses. Yet, setting up a pension account now can make a significant difference later, not just in terms of financial security, but also in exercising flexibility, tax efficiency and peace of mind. In India’s evolving pension ecosystem, the National Pension System (NPS) and the newly introduced Multiple Scheme Framework (MSF) stand out as powerful tools for today’s working individuals.

You should consider having a pension account and be aware of key regulatory updates and insights that benefit NPS subscribers.

The case for a pension account: Why this matters

A pension account is different from your standard savings or even mutual fund investments. It’s designed specifically for the long-term horizon, for your post-working years. Here is why every working individual in India should pay attention.

- Longer time horizon, compounding effect - The earlier you start, the more years your contributions and returns have to compound. For example, someone starting contributions at age 30 has far more years ahead compared to someone starting at 45.

- Structured discipline - Pension accounts like NPS enforce retirement-oriented discipline; funds in Tier I are locked in until age 60 with limited partial withdrawals allowed after 3 years, and the accumulated corpus is used to provide a regular pension or annuity later.

- Regulatory backing and transparency - NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA), which adds protections and standardised structure for the subscriber.

- Flexibility and growth orientation - With recent reforms allowing up to 100% equity investment in NPS for younger subscribers, you can tailor your pension-investment mix to suit your risk appetite and time horizon.

- Tax efficiency - Contributions to NPS Tier I are eligible for tax deductions under Sections 80CCD(1), 80CCD(1B), and 80CCD(2). Partial withdrawals and up to 60% of maturity corpus withdrawal are tax-free, while the remaining 40% used for annuity is taxable as income.

Understanding NPS: What is it and how it works

The NPS or National Pension System is a defined-contribution retirement scheme available to Indian citizens aged 18 to 70 years. Its key features include:

Two-tier structure

- Tier I – A pension-focused account with tax benefits and withdrawal restrictions.

- Tier II – A voluntary, flexible account without tax incentives.

Investment flexibility

Subscribers can choose their Pension Fund Manager (PFM) and asset allocation across equity, debt, and government securities. Returns are market-linked.

Withdrawal and annuity

On retirement or exit, a portion of the accumulated corpus must be used to purchase an annuity for regular pension income. Recent reforms have introduced greater withdrawal flexibility.

Tax benefits

Tier I contributions are eligible for tax deductions up to ₹1.5 lakh under Section 80C, plus an additional ₹50,000 under Section 80CCD(1B) as per the old tax regime.

Disciplined savings structure

Individuals open a PRAN (Permanent Retirement Account Number), contribute regularly (self or employer), and systematically build a long-term retirement corpus.

What MSF brings to the table: More choice, greater control

One of the most important recent reforms in the Indian pension space is the Multiple Scheme Framework (MSF) introduced by PFRDA for NPS.

- Under MSF, non-government subscribers can hold multiple schemes under a single PRAN and across different CRAs (Central Recordkeeping Agencies). This can help in the segmentation of investment style, risk-profile or time-horizon.

- It allows up to 100% equity exposure under a high-risk variant for those comfortable with market volatility and having a long horizon.

- With MSF, pension fund managers can launch differentiated schemes with mandatory moderate and high-risk variants, and optionally low-risk variants, thereby creating choice for subscribers to select schemes matching their life stage, risk appetite, or retirement timeline.

- Under MSF, PFRDA has also standardised charges (fees capped at around 0.30% of AUM) and introduced clearer disclosures.

So, why is this important for you? Here, you can make choices as per your life-stage.

- If you are young (say 25–35) you could go for a high-equity scheme

- If you are nearing retirement you might choose a more conservative variant

How NPS and MSF fit into your broader retirement plan

The pension schemes are isolated products, but their real value emerges when you integrate them into an overall retirement strategy.

- Working years (accumulation phase) - You are contributing, growth is the focus, risk appetite may be higher. Here you may favour equity-oriented schemes under MSF for NPS.

- Transition years (pre-retirement) - Risk appetite typically shrinks; you may shift to conservative variants, accumulate more, reduce volatility. Use MSF flexibility to move into a lower-risk scheme.

- Retirement/decumulation - Start converting corpus into regular pension or systematic withdrawals. With recent reforms you have more withdrawal flexibility and better options under NPS.

- Tax planning layer - With NPS, you can aim for both tax savings and long-term growth. This combination is often missing in other retail instruments.

- Complement other instruments - NPS can complement your investment in other products by offering retirement-specific discipline, regulation and structure.

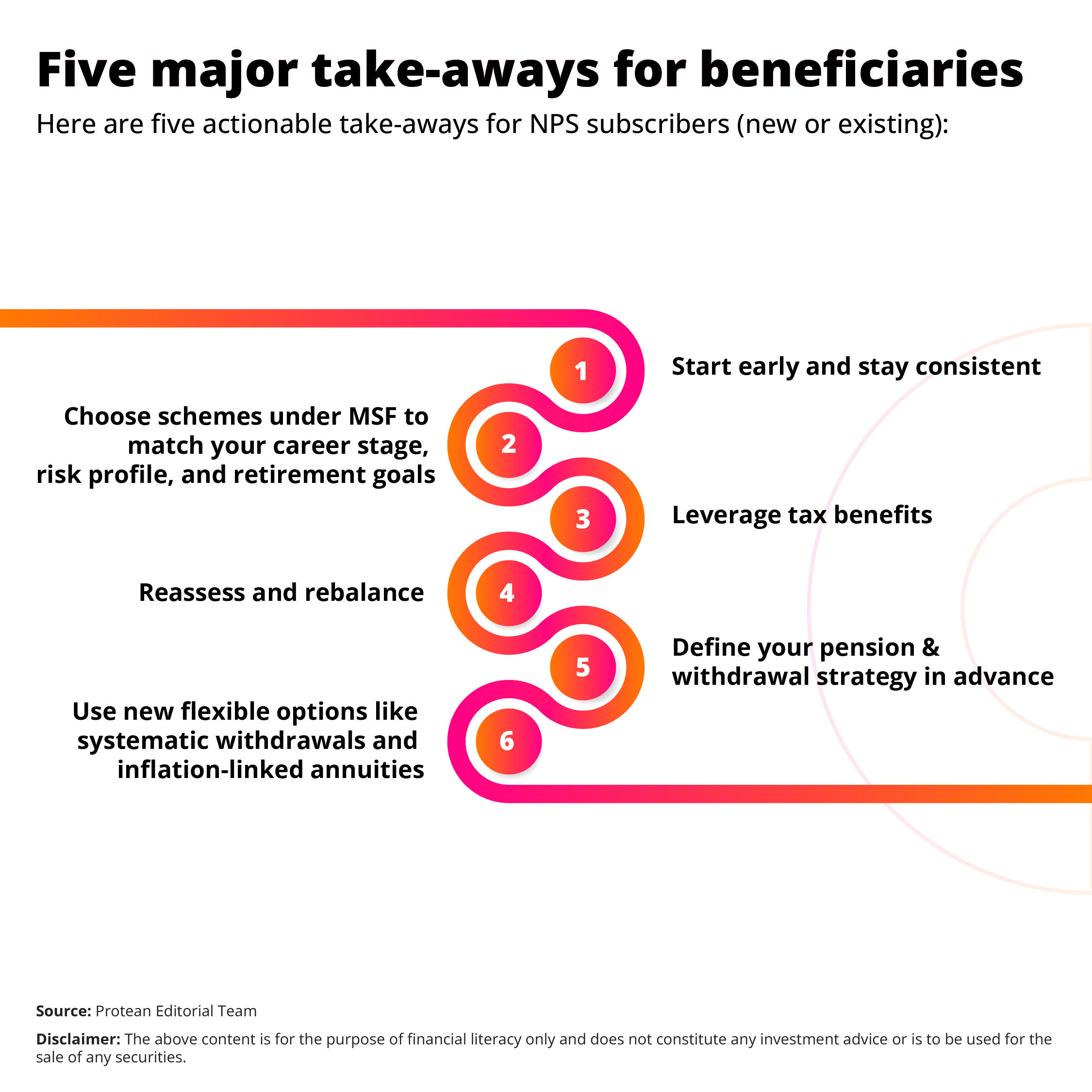

Encouragement for working individuals: Make it happen

Are you in your twenties just starting a job? Or, in your thirties juggling ambitions and family? Or in your forties repositioning for the next decade? It is never too early or too late to open or review a pension account. The reforms (MSF 100 % equity option, and proposed inflation-protected payouts currently under development) mean that the NPS ecosystem is evolving to become more flexible, more customised, and more efficient for you.

- Contribute regularly to build a strong retirement corpus.

- Review your scheme allocation as your goals and circumstances change.

- Use NPS and MSF strategically to structure long-term retirement savings.

- Consult a financial advisor to align NPS with your overall financial plan.

- Start early to maximise the benefits of compounding and flexibility.

Conclusion

The National Pension System (NPS) has provided a regulated, tax-efficient and flexible platform for building retirement wealth. The introduction of the Multiple Scheme Framework (MSF), has given investors greater choice and control over their portfolio. So, why wait? Open or review your NPS account, align your scheme selection with your goals, and plan for a retirement built on preparation and financial confidence.