Indian fintech companies are undergoing a stage of digital transformation. For their growing needs of speed and security, they are moving from penny drop verification to penny less verification.

Earlier, financial institutions used penny drop verification to confirm that a bank account remained active and valid before any service initiation. However, this penny drop verification method created huge "statement clutter" for the average consumer.

Frequent fintech application users found their bank statements filled with small, confusing entries of one Rupee from various platforms. But today, the market moves toward penny less verification to solve this specific pain point and streamline the onboarding journey.

With a robust API integration, businesses can now verify accounts instantly without any physical fund movement.

What are the Structural Challenges of the Penny Drop Era

Traditional validation methods face serious hurdles due to the inherent limitations of physical banking rails.

- High Drop-Offs - Success for penny drop verification depends majorly on the stability and uptime of the IMPS or NEFT systems. Congestion within these rails often causes delays that last several minutes or even several hours during peak traffic. When a user is waiting for a deposit confirmation, their interest in the financial product can wane quickly. This can lead to high drop-off rates during the most important part of the registration journey for a new customer.

- Higher Chances of Failure - Internal finance teams bear a heavy "operational tax" while tracking crores of micro-transactions every month. Thus, reconciliation can become a logistical nightmare when a majority of these small deposits fail or return due to technical glitches. Mistakes in an IFSC code or issues with merged bank branches can frequently cause penny drop verification to fail even if the account is valid. An API integration can query the necessary data points directly from the source. This direct approach can significantly reduce the multiple failure points that plague older and slower validation methods.

Why the Switch Offers a Clear ROI

Financial efficiency is the main driver for the widespread adoption of penny less verification across the fintech sector. Here is why financial services businesses are switching to penny less verification.

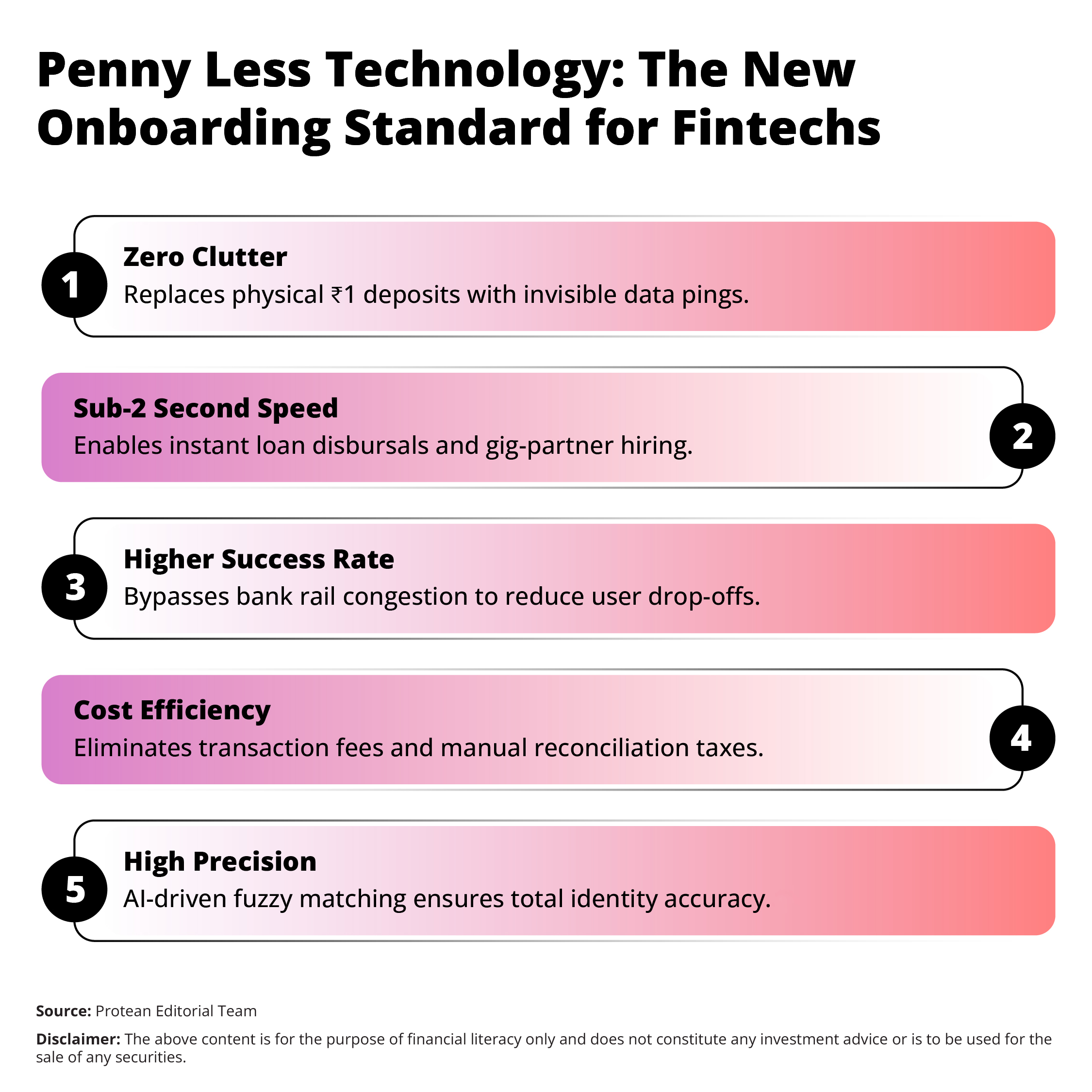

Quick & Efficient - A platform onboarding several users every month can save a huge amount on transaction fees and capital. The cost of a physical deposit includes both the Rupee itself and the associated processing charges from the bank. But penny less verification can lower the per-user validation cost to a high extent. It removes the need for a fund transfer.

Higher Success Rate - The transition to penny less verification can also yield a much higher success rate for the clients’ initial onboarding. The older systems often peak at a certain rate. But modern API integration solutions can achieve higher success rates.

Effective Business Scaling - Users appreciate a clean bank statement, lacking repetitive "one rupee credit" entries from multiple different apps. With such an invisible process, users can enhance the perceived quality of a brand and build a more premium image. Every successful API integration can help a business scale without the burden of manual reconciliation or financial tracking.

Therefore, the return on investment can become clear as the brand reduces customer acquisition costs through higher completion rates.

Where Penny Less Verification Wins in 2026

Financial efficiency is the main driver for the widespread adoption of penny less verification across the fintech sector. Here is why financial services businesses are switching to penny less verification.

Quick & Efficient - A platform onboarding several users every month can save a huge amount on transaction fees and capital. The cost of a physical deposit includes both the Rupee itself and the associated processing charges from the bank. But penny less verification can lower the per-user validation cost to a high extent. It removes the need for a fund transfer.

Higher Success Rate - The transition to penny less verification can also yield a much higher success rate for the clients’ initial onboarding by reducing drop-offs through instant validation. Modern API integration solutions can achieve higher onboarding completion rates.

Effective Business Scaling - Users appreciate a clean bank statement, lacking repetitive "one rupee credit" entries from multiple different apps. With such an invisible process, users can enhance the perceived quality of a brand and build a more premium image. Every successful API integration can help a business scale without the burden of manual reconciliation or financial tracking.

Therefore, the return on investment can become clear as the brand reduces customer acquisition costs through higher completion rates.

Compliance & Security in the New Framework of Penny Less Verification

It is important for Indian financial service providers to maintain regulatory compliance. Here is how a shift from penny drop verification to penny less verification can result in higher compliance and safety.

- The move to penny less verification is aligned with the latest PFRDA and RBI guidelines for digital KYC and bank validation.

- Modern systems use AI-driven fuzzy name matching to identify even the smallest discrepancies in a user’s identity. This technology catches errors that a simple penny drop verification might overlook or ignore.

- With modern API integration, the data exchange can take place through a "Consent-First" framework for the protection of the user. Meaning, users need to provide explicit permission before their data travels through encrypted digital handshakes.

Conclusion: From Trial Deposits to Data Pings

The Indian fintech industry is transitioning from traditional "Trial Deposits" to more efficient API-based verification methods. Protean eGov Technologies can offer the infrastructure required for large-scale digital transformation.

Thus, every business needs to audit its current onboarding success rates to identify potential leaks in the funnel. The future of finance can depend on invisible, secure, and rapid identity checks that respect the time of the user. With the adoption of a modern API integration, your platform can remain at the forefront of the competitive financial industry.

Frequently Asked Questions (FAQs)

Q1: What is the main difference between a penny drop and a penny less check?

A physical deposit of ₹1 defines the traditional check used by older systems. But a secure data query defines the modern check. One can create a permanent bank statement entry. However, the other is invisible to the customer during the process.

Q2: Is penny less verification legal for digital loan disbursals in India?

Yes, this method is compliant with the latest RBI guidelines (via Account Aggregator framework) for account validation. It can provide a secure and auditable trail for identity checks without physical movement of cash.

Q3: Does RISE with Protean support existing legacy systems for verification?

The platform offers flexible tools that connect with various existing digital infrastructures. This allows for a smooth transition from old methods to new ones without a total restart. Businesses can upgrade their processes through a simple API integration for better results.