The Government of India has been focused on creating strong financial frameworks for the next generation, and one of the critical reforms introduced in the July 2024 Union Budget is NPS Vatsalya—a pension scheme specifically designed for minors.

Finance Minister Nirmala Sitharaman’s launch of the NPS Vatsalya scheme on September 18, 2024, saw an impressive turnout on ‘Day 1’, with 9,705 minors enrolling right out of the gate. This response highlights a growing interest among families in securing a strong financial future for the next generation.

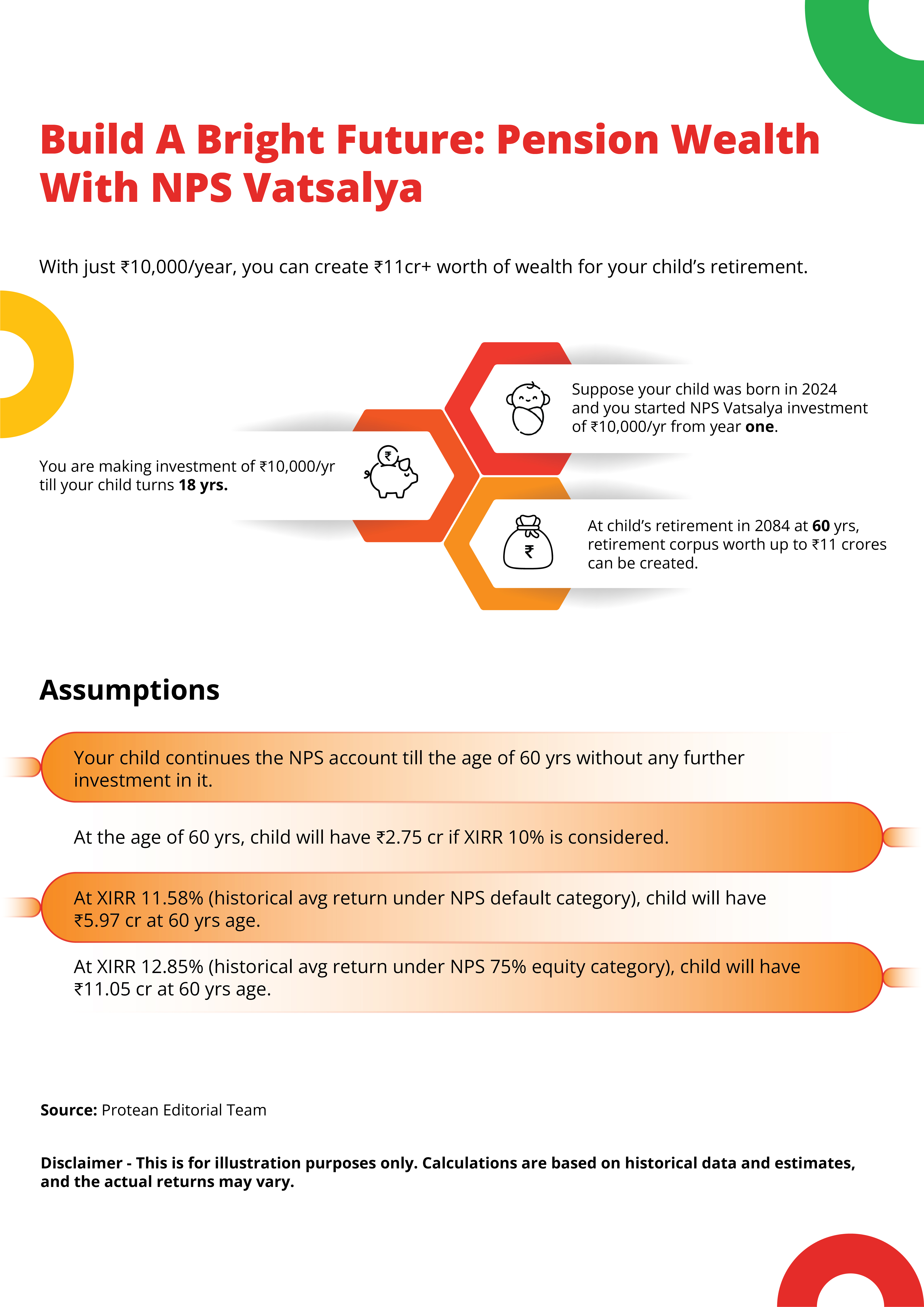

So, what exactly is NPS Vatsalya? How does it benefit both parents and children? Let’s dive into the details and data-driven strategies to help you leverage the power of compounding for your child’s future.

| Ready to invest? Learn how to contribute to NPS Vatsalya online and offline for a seamless experience. |

What is NPS Vatsalya?

NPS Vatsalya is a pension scheme aimed at minors, designed to foster a habit of savings from an early age. According to Finance Minister Nirmala Sitharaman, the primary goal is to help young subscribers develop a disciplined savings routine. "NPS Vatsalya provides an excellent opportunity for minors to accumulate wealth over the long term through the power of compounding," said the Finance Minister during the scheme's launch.

Enrolling your child to NPS Vatsalya gives them access to a disciplined, government-backed pension scheme that could generate significant wealth by the time they retire.

Imagine starting with an initial investment and seeing it multiply into a healthy retirement corpus—thanks to compounding, this is very much a reality.

| Explore the online and offline methods to start contributing to NPS Vatsalya today! |

Key Features of NPS Vatsalya

NPS Vatsalya brings several unique features, making it stand out from other financial instruments designed for minors. Here are some key features that make the scheme attractive:

- Eligibility: The scheme is available to minors under 18, allowing them to start saving for retirement.

- Compounding Benefits: Since the scheme is designed for long-term wealth building, it leverages the power of compounding, meaning that the longer the investment horizon, the greater the wealth accumulated.

- Flexibility in Investments: The scheme allows investors to choose between Active and Auto investment choices, which we will explore later in this blog.

- Nomination Facility: Parents can nominate their child for this scheme, ensuring their child's financial safety and security in the event of an unfortunate incident.

- Pension Wealth: NPS Vatsalya builds a pension corpus that can later be converted into an annuity, providing a steady income stream during retirement.

- Low Minimum Contribution: Parents can start with an annual contribution as low as ₹1,000.

| Learn how to invest in NPS Vatsalya using simple steps here. |

Contributions and Investment Choices in NPS Vatsalya

The NPS Vatsalya scheme offers a flexible approach to contributions and investment management, allowing guardians to tailor their financial plans according to their goals:

- Account Opening Contribution: A minimum initial contribution of ₹1,000 is required to open the account, with no upper limit on how much you can invest.

- Subsequent Contributions: A minimum contribution of ₹1,000 per year is necessary to keep the account active, though there’s no cap on how much can be contributed annually.

Guardians can choose from various Pension Funds registered with the Pension Fund Regulatory and Development Authority (PFRDA) to manage their child’s investments.

When it comes to selecting how the funds are invested, NPS Vatsalya provides three key choices:

- Default Choice: The Moderate Life Cycle Fund (LC-50) is the default option, where 50% of the investment is allocated to equity, providing a balanced growth approach.

- Auto Choice: Guardians can opt for one of three lifecycle funds depending on their risk appetite:

- Aggressive (LC-75): Up to 75% of the investment is allocated to equity, ideal for those comfortable with higher risk for potential high returns.

- Moderate (LC-50): A balanced fund with 50% invested in equity, offering moderate risk and returns.

- Conservative (LC-25): This fund allocates 25% to equity for those with lower risk tolerance, minimising risk while allowing for gradual growth.

- Active Choice: This option gives guardians complete control over how to allocate funds across different asset classes. They can invest:

- Up to 75% in equity for higher growth potential,

- Up to 100% in corporate debt for stability,

- Up to 100% in government securities for safety,

- Up to 5% in alternate assets for diversification.

This flexibility allows guardians to tailor their investment strategy to financial goals and risk preferences.

| For more details, refer to the official announcement from the Press Information Bureau here. |

| Discover how you can invest in NPS Vatsalya online and offline. |

| Ready to start? Here’s how you can contribute to NPS Vatsalya effortlessly! |

Conclusion

NPS Vatsalya is a scheme aimed at securing the financial future of minors by instilling a savings habit. With flexible investment choices, tax benefits, and the potential to generate significant wealth over time, NPS Vatsalya is a must be considered by every parent who wants to ensure their child’s financial independence in retirement.

By investing in NPS Vatsalya, you are not just saving for the future; you are building a financial safety net for your child that will provide long-lasting benefits well into their retirement years.

| Learn how to contribute to NPS Vatsalya today! |

Also read:

7 Key Benefits Of NPS Vatsalya

NPS Vatsalya Vs Mutual Funds Vs PPF

NPS Vatsalya related to Opening of NPS Vatsalya Account

NPS Vatsalya related to Accumulation under NPS Vatsalya Account

NPS Vatsalya related to partial or full exit from NPS Vatsalya Account

story by Bruhadeeswaran R.