Are you looking for NPS partial withdrawal steps? Is NPS withdrawal different for Tier-I and Tier-II accounts?

Let us find out!

The National Pension System (NPS) can be the core of retirement planning, with a maturity-based Tier-I account, and the flexible Tier-II account.

However, life is unpredictable. Recognising this, the Pension Fund Regulatory and Development Authority (PFRDA) has permitted partial withdrawals under specific, well-defined circumstances.

Let us learn more about the NPS withdrawal rules and NPS partial withdrawal conditions.

| Check the elaborate list of NPS withdrawal rules here. |

Eligibility and Conditions for NPS Partial Withdrawal

To safeguard your long-term retirement corpus, NPS withdrawal rules are governed by strict criteria.

Eligibility Criteria

- Minimum Subscription Period: You must have been subscribed to the NPS Tier-I account for at least three years to qualify for a partial withdrawal.

- Purpose-Specific Withdrawals: The facility is strictly event-based. This means that you cannot withdraw randomly. The withdrawal must align with one of the permitted NPS withdrawal scenarios.

Permitted NPS Withdrawal Scenarios (as of May 2025)

Partial withdrawals from the NPS Tier-I account are allowed only under the following circumstances:

- NPS Withdrawal for Marriage – For your own wedding or that of your children (including legally adopted).

- NPS Withdrawal for Education – For your children’s higher education (including legally adopted).

- NPS Withdrawal for Medical Expenses – For critical illnesses suffered by you, your spouse, children, or dependent parents. Illnesses are as defined under PFRDA norms.

- NPS Withdrawal for Home Purchase/Repair – Provided you do not already own residential property (either solely or jointly). Major structural renovation or repair of your own home can also be considered.

Other major NPS withdrawal reasons can be natural calamities and skill development or self-employment.

| Learn all about NPS. Access NPS resources now! |

Decoding the NPS Withdrawal Limit: How Much Can You Withdraw?

The NPS withdrawal limit is designed to maintain balance, addressing urgent needs without compromising retirement goals.

- Withdrawal Cap: You may withdraw up to 25% of your own contributions (excluding any contributions made by your employer) as on the date of application.

- Frequency: You can make only three partial withdrawals during the entire tenure of your NPS Tier-I account.

Here is an example:

If you have contributed ₹8 lakhs (excluding employer contributions) to your NPS account, you can withdraw a maximum of ₹2 lakhs (25%) under an eligible reason.

Exploring Lesser-Known Scenarios

While the broad rules are widely known, some aspects of NPS premature withdrawal deserve closer attention. These are as follows:

- Your First House Purchase

- NPS Withdrawal is only allowed if you do not already own a residential property.

- The amount must be used strictly for purchase or construction, and proof of utilisation may be required.

- Critical Illness Coverage

- PFRDA defines a list of critical illnesses such as cancer, stroke, organ failure, and heart surgeries. The condition must be certified by a registered medical practitioner.

- The claim can be made for family members as well, making it a valuable safety net.

- For Skill Development or Self-Employment

- This relatively new inclusion supports career transitions and entrepreneurship.

- Withdrawals can fund certified skill development programmes or initial business set-up costs.

| Click here to start your NPS investment journey now! |

NPS Partial Withdrawal Documentation Requirements

Each withdrawal reason demands specific proof. These are as follows:

- Marriage: Wedding invitation or certificate.

- Education: Fee receipts or admission letter.

- Medical: Diagnosis reports and cost estimates.

- Housing: Property papers or construction bills.

- Skill Development: Course enrolment details or self-employment plans.

You can ensure that documentation is accurate to avoid delays.

| Learn more about NPS partial withdrawal rules here. |

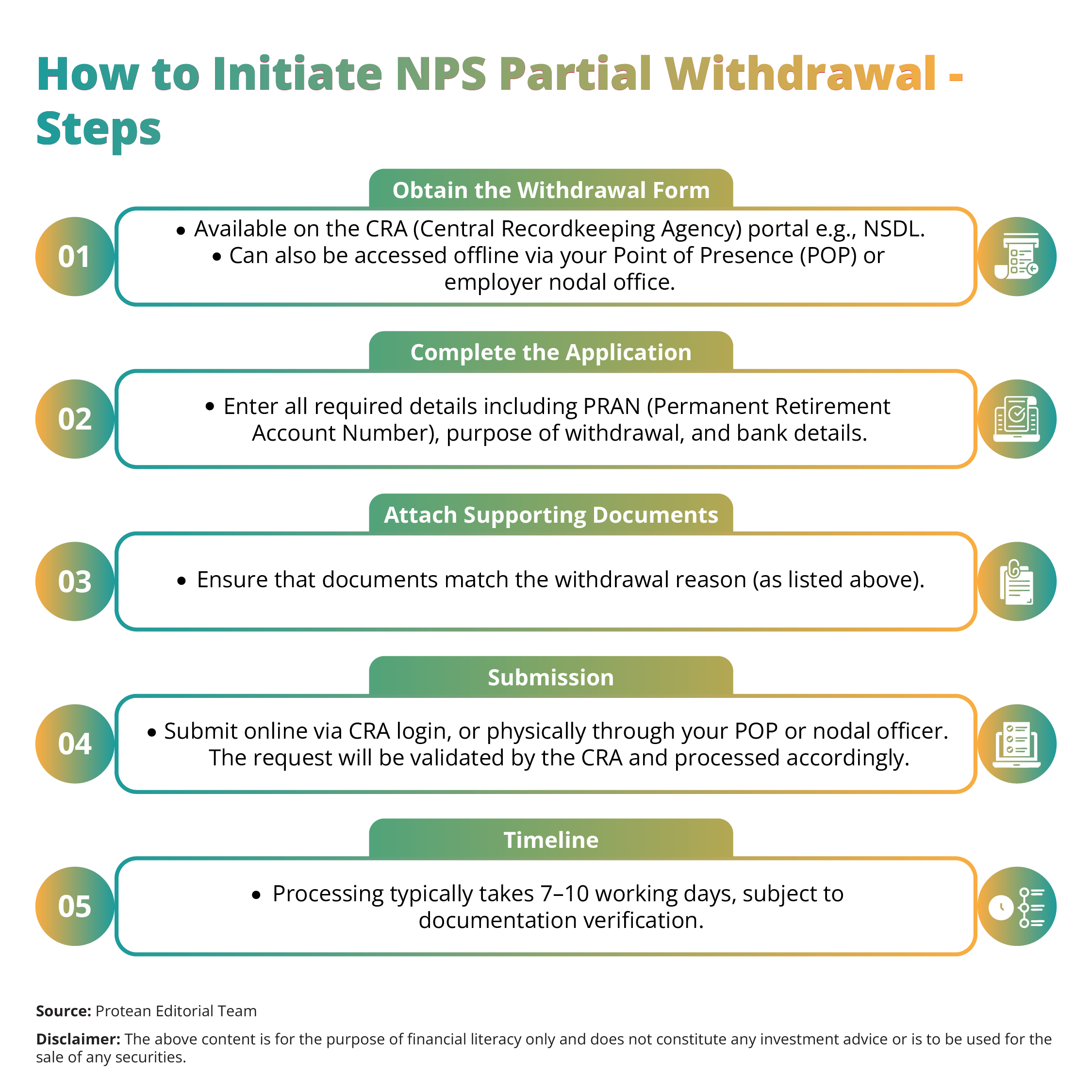

Step-by-Step NPS Withdrawal Process: How to Initiate NPS Partial Withdrawal

Here is a brief roadmap (as of May 2025) for partial NPS withdrawal:

Important Considerations and Potential Implications

Before opting for a NPS partial withdrawal, it is important to weigh the following:

- Impact on Retirement Corpus: Every withdrawal reduces your long-term accumulation and potential annuity.

- Tax Implications: As of May 2025, partial withdrawals (within permitted conditions) are tax-exempt. However, taxation norms are subject to change.

- Strategic Planning: Align your withdrawal with critical needs, not short-term desires. Therefore, you should always keep your retirement goals in focus.

| Why wait? Begin your NPS investment today! |

Conclusion

The NPS withdrawal facility can offer crucial support in times of need, be it for family, education, or rebuilding after a crisis. Subscribers can make empowered decisions without jeopardising their retirement dreams if they make NPS withdrawals in an informed manner and use this facility judiciously and only when essential.

| Take the right step towards post-retirement financial security, start investing in NPS now! |