Did you just search ‘NPS for women’ or ‘NPS scheme for women’ on the internet? You might have found many articles, but here’s an easier explanation of NPS and NPS scheme for retirement planning through the story of Meera and Asha!

Meera (Senior HR Professional):

Asha, I’ve noticed a rising trend. More women in our firm are seeking financial advice, especially on long-term savings. And it’s not just about saving; it’s about retiring smart.

Asha (Financial Planner):

That’s wonderful, Meera. But the reality is, many still overlook structured retirement planning. With career breaks, wage disparities, and higher life expectancy, women need to be strategic with their retirement choices.

Meera:

Exactly! I’ve been reading up on the National Pension System (NPS). I’m curious to learn more about NPS for women.

Asha:

Let’s break down how Indian women can maximise benefits from the NPS scheme for long-term financial security.

The Financial Journey of Indian Women

Meera:

Many of my female colleagues take career breaks for maternity, childcare, or even elder care. In fact, some leave the workforce entirely for years.

Asha:

Absolutely true. These breaks, though essential, lead to discontinuity in income and in contributions to other retirement vehicles like EPF (Employees’ Provident Fund). That loss of compounding can be significant over the years.

Meera:

And, even when women return, they often come back on part-time roles, freelancing, or self-employment. Here, structured retirement savings are not automatically deducted.

Asha:

This is why a dedicated, long-term, low-maintenance tool like NPS can help fill that gap. The NPS scheme is voluntary, structured, and portable across employment types. NPS scheme for women can be better for salaried, self-employed, or those switching career tracks.

Meera:

So, it acts like a bridge for those disrupted earning years?

Asha:

Yes, and more. It instills the discipline needed to save consistently. NPS retirement planning can be especially important when your earning years are uneven.

Check how NPS investment compares to other investment options here.

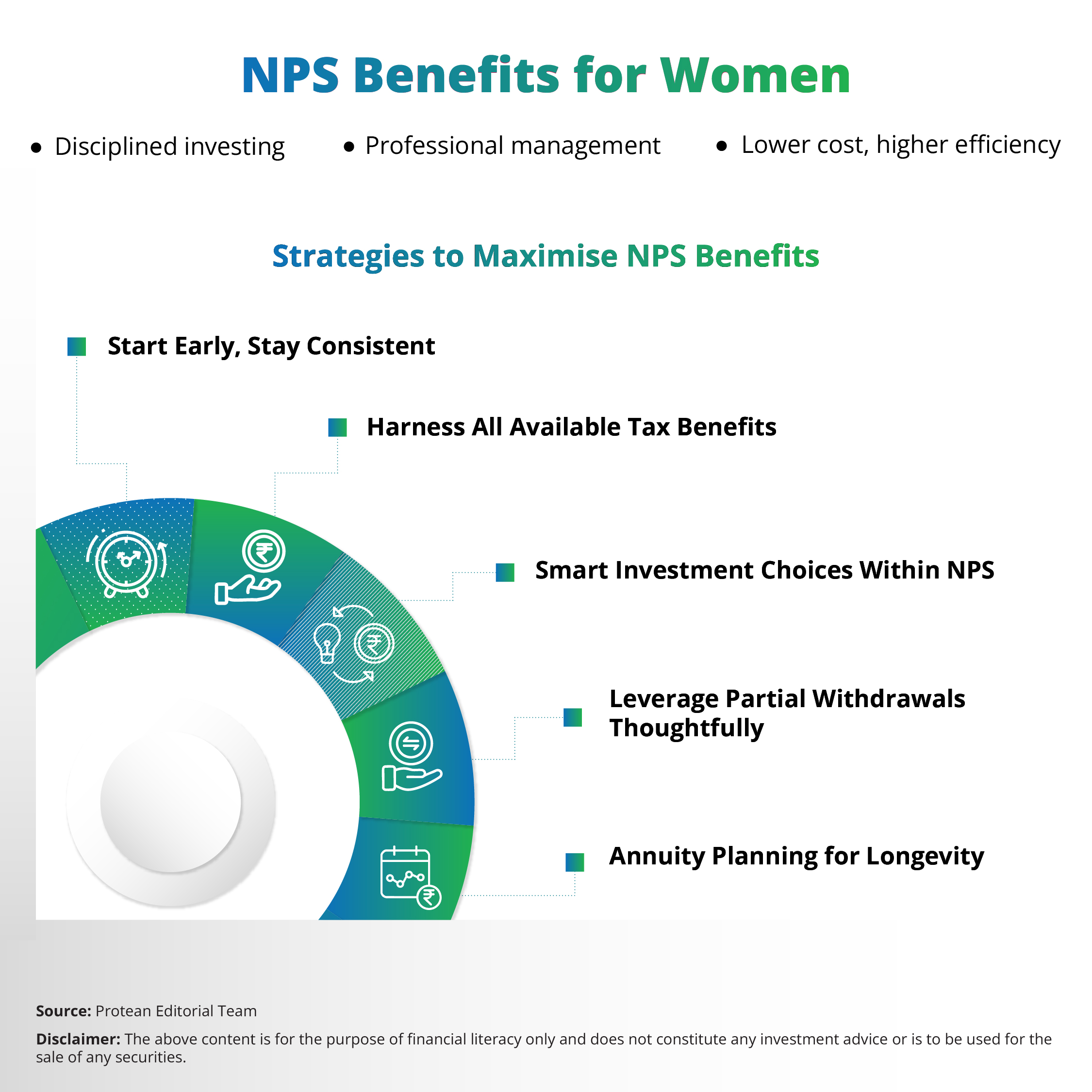

NPS Benefits for Women

So, why is NPS particularly better for women in terms of tax saving and retirement planning?

Here are three major points of NPS benefits for women:

- The Tier-I account, which is the primary NPS account, is a long-term savings account with limited withdrawal options. This ‘lock-in’ can work in favor of women who may be tempted to use funds for family expenses during breaks.

- NPS has one of the lower expense ratios among investment instruments in India. That means your money can stay invested, and compounding works better over time.

- You’re not on your own. Your funds are managed by experienced pension fund managers. So even if you don’t actively track the markets, your money is still growing in a diversified, risk-adjusted manner.

Thus, NPS for women can be a boon when it comes to retirement planning and tax benefits.

Check this blog to learn about maximising NPS investment benefits.

Strategies for Women to Maximise NPS Benefits

Now, let us dive into how women can make the most of NPS.

Start Early, Stay Consistent with NPS

The earlier you start, the better the compounding can be. A woman starting at 25 and investing ₹5,000 monthly can accumulate a significantly larger corpus than one who starts at 35 with the same amount.

But what about the career breaks impacting women?

Even if contributions pause for a year or two, the early years of investing continue to grow. You can resume once you are back and make up if you can.

Take your first step towards post-retirement financial security, with NPS for women now.

Harness All Available Tax Benefits

NPS benefits under old tax regime:

- Under Section 80CCD (1), contributions up to ₹1.5 lakh annually are deductible as part of the ₹1.5 lakh limit under Section 80C.

- An additional ₹50,000 is available exclusively under Section 80CCD (1B). This is over and above the 80C limit.

That makes a total of ₹2 lakh in deductions per year with an NPS scheme contribution!

For working women in higher tax brackets, this can mean real savings now, while building wealth for the future.

Already have an NPS account? Click here to make your contribution.

Smart Investment Choices Within NPS

Women can also choose their NPS asset allocation, between:

- Equity (E)

- Corporate debt ©

- Government securities (G).

If you are younger and can take a bit of risk, go for Active Choice and allocate up to 75% in equity.

As you approach 50, you can switch to Auto Choice, which gradually shifts to safer debt instruments.

As a government employee, you can change your asset allocation twice a year and switch fund managers once a year. This can be different for non-government employees, who can switch fund managers once in four years. This can ensure you are in control as your life and risk appetite evolve.

Leverage Partial Withdrawals Thoughtfully

Partial withdrawals are allowed in an NPS scheme under specific conditions, like:

- Child’s higher education or marriage

- Purchase/construction of a house

- Medical emergencies

You can withdraw up to 25% of your own contributions (not the entire corpus), after completing 3 years in NPS. And, you can do this up to 3 times in your subscription period.

Annuity Planning for Longevity

NPS for women can be a boon to increased life expectancy by building a planned retirement corpus.

Upon exit at age 60, at least 40% of the corpus must be used to buy an annuity, this can give you a regular pension.

If you are looking for even more liquidity, here’s something for you:

You can withdraw up to 60% lump sum tax-free at retirement, and only the annuity income is taxed.

Meera:

Thanks, Asha. I always saw NPS as just another tax-saving tool. But now I see how strategically powerful it can be, especially for women like me juggling family and career.

Asha:

That’s the beauty of the NPS scheme for women. It is disciplined, flexible, professionally managed, and incredibly tax-efficient. For women facing wage gaps, career pauses, and longer life spans, it is a reliable way to retirement planning.

Meera:

I’m going to set up my NPS account this weekend.

Click here to register for an NPS subscription now.

Conclusion

NPS can offer a structured, low-cost, and tax-efficient solution tailored to the unique financial needs of Indian women. The NPS scheme for women can help them start early, leverage tax benefits, invest smartly, and plan annuities wisely to get the most out of the NPS scheme. NPS is not just about retirement, it is about ensuring your financial independence for life.