When can the NPS withdrawal happen? Though complete NPS withdrawal after retirement is possible, investors find themselves facing a key decision such as, should they withdraw their NPS funds right away or is there value in holding off?

NPS is one of India's most effective tools for building a retirement corpus through disciplined, market-linked investing.

Let us learn about NPS withdrawal, and what can happen if you don’t go for NPS withdrawal after retirement?

| You may click on this link for knowing more aspects related to NPS PRAN registration. |

Option 1: The Power of Continuation – Keeping Your NPS Account Active Beyond 60

Here is a surprise for NPS subscribers!

Your Tier I investment does not require immediate NPS withdrawal after retirement at 60. In fact, you can continue your NPS account up to the age of 75, with or without making further contributions.

To keep your account active and NPS account contribution post-60, you can submit a continuation request. You can do this using Form 302 to the Central Recordkeeping Agency (CRA) or through your NPS account login. You can file this request before reaching 60. However, PFRDA currently allows submission within a year post-retirement under certain circumstances.

| Learn more about NPS investment exit options here. |

Benefits of continuing your NPS account

The following are the benefits of keeping NPS invested in retirement:

- Continued Investment Growth

Your corpus can remain invested in your selected asset allocation (Equity, Corporate Bonds, and Government Securities). This can allow you to capitalise on post-retirement market returns, particularly if your retirement coincides with unfavourable market conditions.

- Tax Advantages

NPS account contribution post-60 can remain eligible for tax deductions under Section 80CCD(1B). This can be an additional deduction of ₹50,000 annually. Thus, it can be an important tool for those with taxable post-retirement income.

- NPS Withdrawal Flexibility

You can postpone deciding when to begin NPS withdrawal. Thus, you can align your NPS access with personal financial needs, lifestyle plans, or other retirement income sources.

Here are a few considerations for NPS withdrawal after retirement:

- While continuation is permitted until age 75, you can at least start phased withdrawal of NPS by then.

- While managing NPS after retirement age, and during phased withdrawals of NPS, it can benefit to potentially review and revisit investment allocation. This is because your risk appetite may change over time.

Option 2: The Strategic Pause – Deferring NPS Withdrawal Within the Existing Framework

If you do not wish to make further NPS contributions, but prefer keeping NPS invested in retirement, you have an option to do so. You can choose to defer your NPS withdrawal.

| To understand the ‘Deferment option’, click here. |

The implications of deferring NPS withdrawal are as follows:

- Growth Opportunity

Your corpus would stay invested.Thus your NPS investment value can potentially appreciate, although subject to market volatility.

- Control over Timing

You can decide when to initiate the annuity purchase or NPS withdrawal of your lump sum. You can do this within the stipulated three-year window.

- Mandatory Rules Apply

Even if you defer, you can eventually annuitise at least 40% of the corpus. You can withdraw the remaining 60% by the end of the deferment period.

This flexibility can enable retirees to optimise the NPS withdrawal timing based on interest rate cycles, annuity pricing, or personal financial events, such as large planned expenses or bridging a short-term income gap.

| Check this link for NPS withdrawal FAQs. |

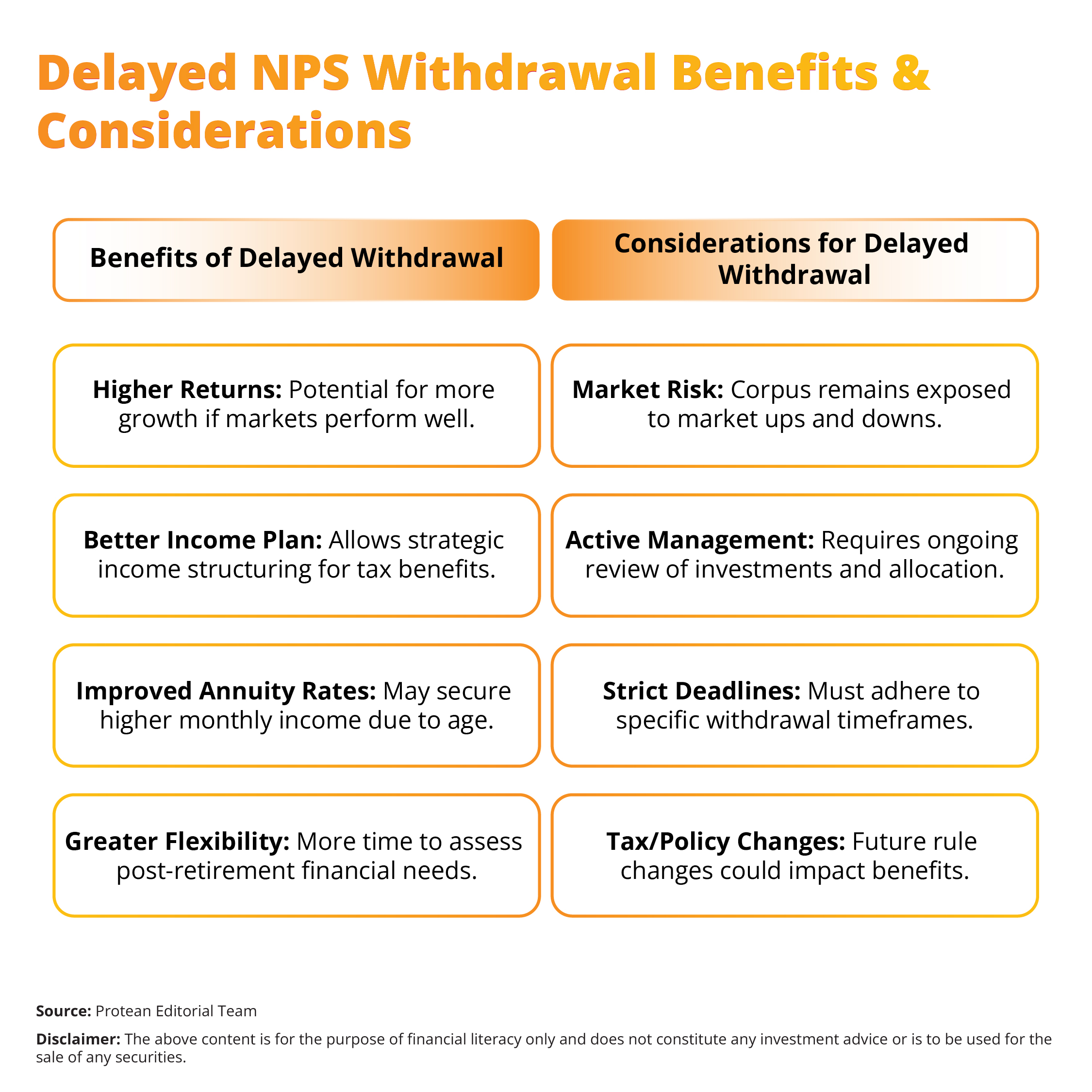

Navigating the Decision: Key Benefits and Crucial Considerations of Delayed Withdrawal

Here are a few potential benefits of delaying NPS withdrawal after retirement:

- Better Returns

If markets perform favourably during the deferment or continuation period, your retirement corpus might grow substantially beyond what was available at 60.

- Optimised Income Planning

Delaying withdrawals can help you structure retirement income more strategically. Perhaps you might choose drawing first from other savings to reduce tax liability, or delaying until you need the funds for health care or estate planning.

- Improved Annuity Rates

Annuity rates tend to be better for older retirees since insurers factor in shorter payout durations. Though not guaranteed, delaying annuity purchase could, in some cases, secure higher monthly income.

Here are a few crucial considerations to look for while delaying NPS withdrawal:

- Market Risks Remain

Your corpus continues to be exposed to market fluctuations, which could severely impact the value if the market performs poorly.

- Active Management Required

You must remain engaged with your NPS investments, reviewing fund performance and asset allocations in light of changing needs and economic conditions.

- Deferment Deadlines

Clear deadlines exist for initiating annuity and lump sum withdrawals. Failure to act within the prescribed timeframes could lead to default actions or potential regulatory issues.

- Policy and Tax Changes

There is always the possibility of changes in tax laws or PFRDA regulations that could affect the benefits of a delayed NPS withdrawal strategy.

Whether you aim to grow your corpus, align withdrawals with expenses, or wait for better annuity rates, you can assess your situation holistically.

| Already have an NPS account? Click here to make your contribution. |

Conclusion

The National Pension System can offer valuable post-retirement flexibility, enabling subscribers to delay accessing their corpus for potentially better financial outcomes. You can make informed choices to ensure your retirement years are financially secure and aligned with your long-term goals. Take steps towards your post-retirement financial security now with NPS investing.

| Click here to register for an NPS subscription now |