The National Pension System (NPS) is a government-sponsored pension scheme introduced in India to provide a retirement savings solution to all Indian citizens, including those in the public, private and unorganized sectors. It was launched on January 1, 2004 by the Government of India with the aim of providing financial security to individuals during their retirement years. It is regulated by Pension Fund Regulatory and Development Authority (PFRDA) and has emerged as a popular investment scheme aimed at saving for one’s retirement.

- NPS for Government Employees: NPS became mandatory for all Central Government employees who joined service on or after January 1, 2004. It has also been adopted by nearly all State Governments for their employees.

- NPS for Indian Citizens: Any Indian citizen, whether a resident, non-resident or overseas citizen between the ages of 18 and 70 years can voluntarily subscribe to NPS.

- NPS for Employers: Employers can voluntarily adopt NPS as a retirement benefit scheme for their employees.

Read and get answers to common questions on NPS here.

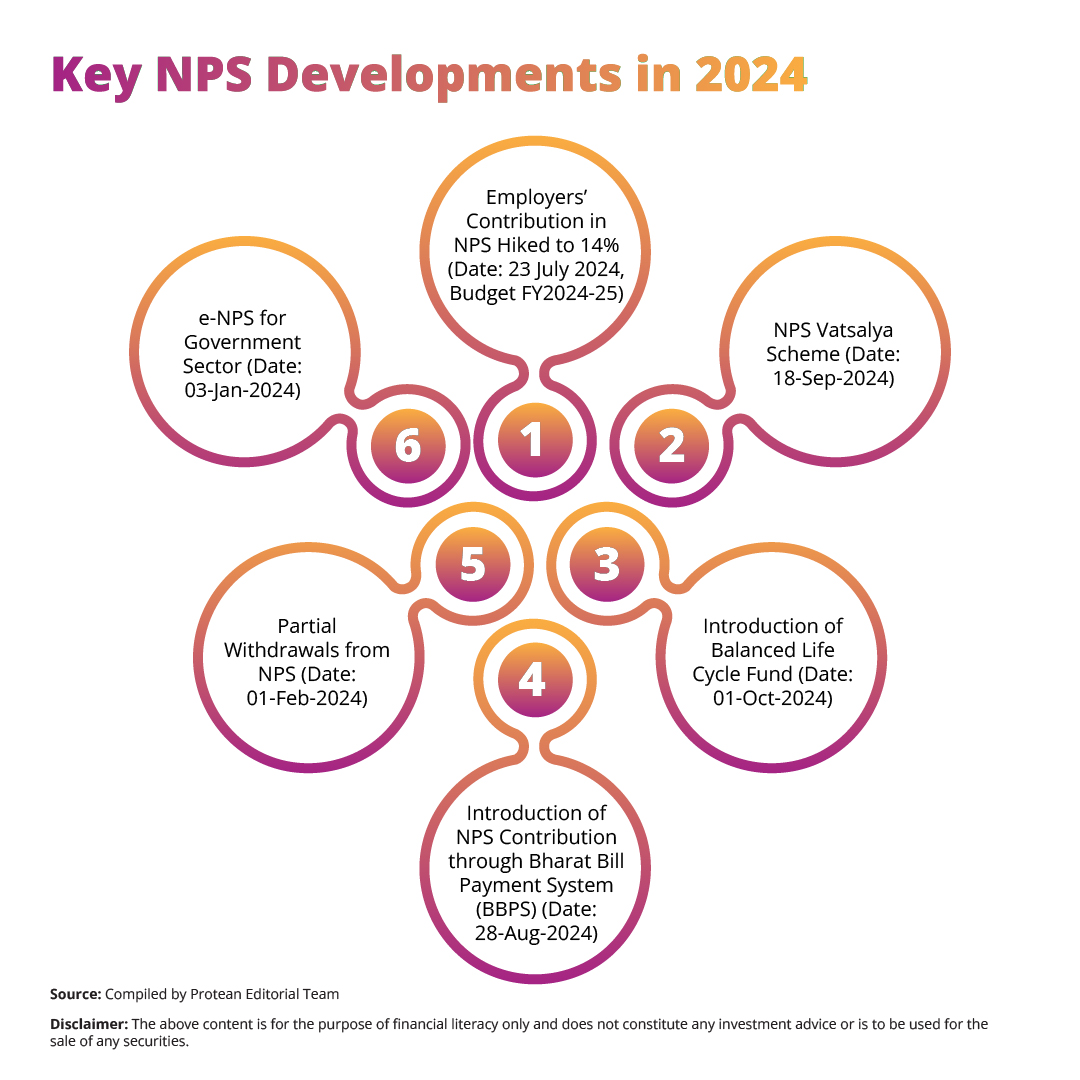

Key Developments in the National Pension System (NPS) in 2024

Employers’ Contribution in NPS Hiked to 14% (Date: 23 July 2024, Budget FY2024-25)

In the Union Budget for FY2024-25, Finance Minister Nirmala Sitharaman announced a hike in the non-government employer’s contribution to NPS from 10% to 14%. Earlier, this limit was only available to government employees.

- Impact: This increase ensures that all NPS subscribers, regardless of sector, enjoy equal benefits from the scheme, enhancing their retirement savings. Consequently, employees can now attain an added deduction equivalent to 4% of their basic salary regarding employer contributions to the NPS. To illustrate, an employee earning a basic monthly salary of ₹1 lakh can now avail an additional deduction of ₹4,000 each month, ultimately leading to an annual deduction totalling ₹48,000.

- Background: The NPS replaced the old pension scheme (OPS) after 2004, offering a more sustainable pension solution. The hike aligns with the government’s efforts to boost financial security for private sector employees.

NPS Vatsalya Scheme (Date: 18-Sep-2024)

The NPS Vatsalya Scheme was introduced as a plan for contribution by parents and guardians for minors to be converted into a normal NPS account on attainment of majority. It is a significant development in India’s pension landscape aimed at securing the financial future of children.

Key Features:

- Investment Option: Parents can invest as little as ₹1,000 annually in their child's name, making it accessible to families from various economic backgrounds.

- Account Details: The account is opened in the minor’s name and is operated by the guardian. The minor is the sole beneficiary.

- Age Transition: Upon the child turning 18, the account can be seamlessly transferred to a Tier I NPS account.

- Goal: NPS Vatsalya allows parents to build long-term wealth for their children, harnessing the power of compounding.

- Participating Banks: ICICI Bank, State Bank of India, Axis Bank, Canara Bank, Central Bank of India, Indian Overseas Bank, Bank of Maharashtra and Federal Bank.

Gift your child their future financial security. Learn more about NPS Vatsalya.

Introduction of Balanced Life Cycle Fund (Date: 01-Oct-2024)

The Balanced Life Cycle Fund was introduced to the NPS by the PFRDA for private sector subscribers - both corporate and individual.

Key features include the following:

- Objective: To provide automatic rebalancing of the asset classes between equity (E), government securities (G) and corporate bonds (C) based on the subscriber’s age and risk profile.

- Equity Allocation: The maximum equity allocation under this fund is 50%, tapering down after the age of 45 as compared to 35% in existing life cycle funds. Refer to the table below.

Source: PFRDA

- Additional Investment Option: The Balanced Life Cycle Fund is an additional option, alongside existing choices such as Active and Auto choices, with Moderate Life Cycle Fund (LC50) remaining the default choice for subscribers.

Sounds interesting? Read more about NPS and its contribution to financial independence.

Introduction of NPS Contribution through Bharat Bill Payment System (BBPS) (Date: 28-Aug-2024)

BBPS, conceptualised by the Reserve Bank of India (RBI) and driven by the National Payments Corporation of India (NPCI) was introduced as an additional payment channel for NPS contributions. It enhances accessibility and ease of contributing to the NPS.

Main features include the following:

- Payment Platforms: Subscribers can now make contributions through popular payment apps like BHIM, PhonePe, Google Pay, and others.

- Trail Commissions: Like eNPS, trail commissions will be applicable for contributions made through BBPS for subscribers associated with Points of Presence (POPs).

- Transaction Process: BBPS will initially support lump sum contributions with refunds for failed transactions processed within 5 working days.

- SIP Mandate: A facility for systematic contributions via BBPS will be introduced in the future.

- Charges: The following charges will apply for making payment through BBPS

Source: PFRDA

Partial Withdrawals from NPS (Date: 01-Feb-2024)

From February 1, 2024, PFRDA allows NPS subscribers to make partial withdrawals from their accumulated pension wealth for specific purposes. A subscriber can withdraw up to 25% of their own contributions (excluding employer's contributions) to their NPS account and is permitted up to 3 partial withdrawals during their entire NPS tenure. This provision provides subscribers with greater flexibility in utilizing their NPS corpus for essential personal and family needs, while still securing their retirement savings.

Eligible purposes for partial withdrawal are as follows:

- Higher Education/Marriage of the subscriber's children (including legally adopted children).

- Purchase/Construction of a residential house or flat (either solely or jointly with the legally wedded spouse). Withdrawal is not permitted if the subscriber already owns a residential property (excluding ancestral property).

- Medical Treatment for specified illnesses (e.g., cancer, kidney failure, stroke, Covid-19, etc.).

- Medical Expenses due to the subscriber's disability or incapacitation.

- Skill Development/Re-skilling or other self-development activities.

- Establishment of a Venture or start-up by the subscriber.

Eligibility Criteria for Partial Withdrawal:

- The subscriber must have been a member of NPS for at least three years.

- The withdrawal amount should not exceed 25% of the subscriber's total contributions (excluding employer’s contributions) as of the withdrawal date.

- No withdrawals are allowed from returns generated on contributions.

Conditions for Subsequent Withdrawals: Only incremental contributions made after the previous partial withdrawal are eligible for future withdrawals.

Read about the NPS calculator and benefits of opening an NPS account.

e-NPS for Government Sector (Date: 03-Jan-2024)

A new feature to facilitate easier registration for government sector employees was introduced under the e-NPS platform. This option enables government employees (Central/State and Autonomous Bodies) to easily open NPS accounts in a paperless and user-friendly manner, streamlining the registration process for seamless access to the scheme. The registration can be done via following modes:

- Aadhaar e-KYC: Enables online/offline Aadhaar-based verification.

- PAN-based Registration: Requires the submission of PAN and KYC documents.

Sounds interesting? Start your financial independence journey with NPS now.

Other Pension Schemes by Government – Atal Pension Yojna (APY)

It is a government-backed pension scheme aimed at providing financial security to individuals in the unorganized sector, especially those who have no formal pension plan. It was launched by the Government of India in 2015 to encourage people, particularly low-income workers to save for their retirement. NPS Lite was also designed to provide pension solutions to individuals in the unorganized sector but had different features and objectives. In 2017, NPS Lite was merged with APY to create a single unified pension scheme for the unorganised sector. This merger simplified pension access for low-income workers, combining the benefits of both schemes into one and APY became the primary tool for low-income pension savings.

Key Features of APY:

- Target Audience: Individuals in the unorganized sector such as domestic workers, construction workers, and small shopkeepers, who do not have access to formal pension schemes.

- Eligibility: Indian citizens between the ages of 18 to 40 years are eligible to join APY.

- Pension Amount: Subscribers can choose a monthly pension of ₹1,000 to ₹5,000 upon reaching the age of 60, based on their contribution and the age at which they start.

- Contribution: The contribution amount is based on the monthly pension chosen. The government co-contributes 50% of the subscriber's contribution (up to ₹1,000 per year) for the first 5 years for those who join before 31st December 2015.

- Fixed Monthly Pension: Upon reaching the age of 60, the subscriber receives a fixed monthly pension which is guaranteed for life.

- Government Support: The scheme is backed by the Government of India, ensuring that individuals from lower-income backgrounds can secure a pension without the risk of market fluctuations.

- Direct Deduction: Contributions are automatically deducted from the subscriber’s bank account via auto-debit.

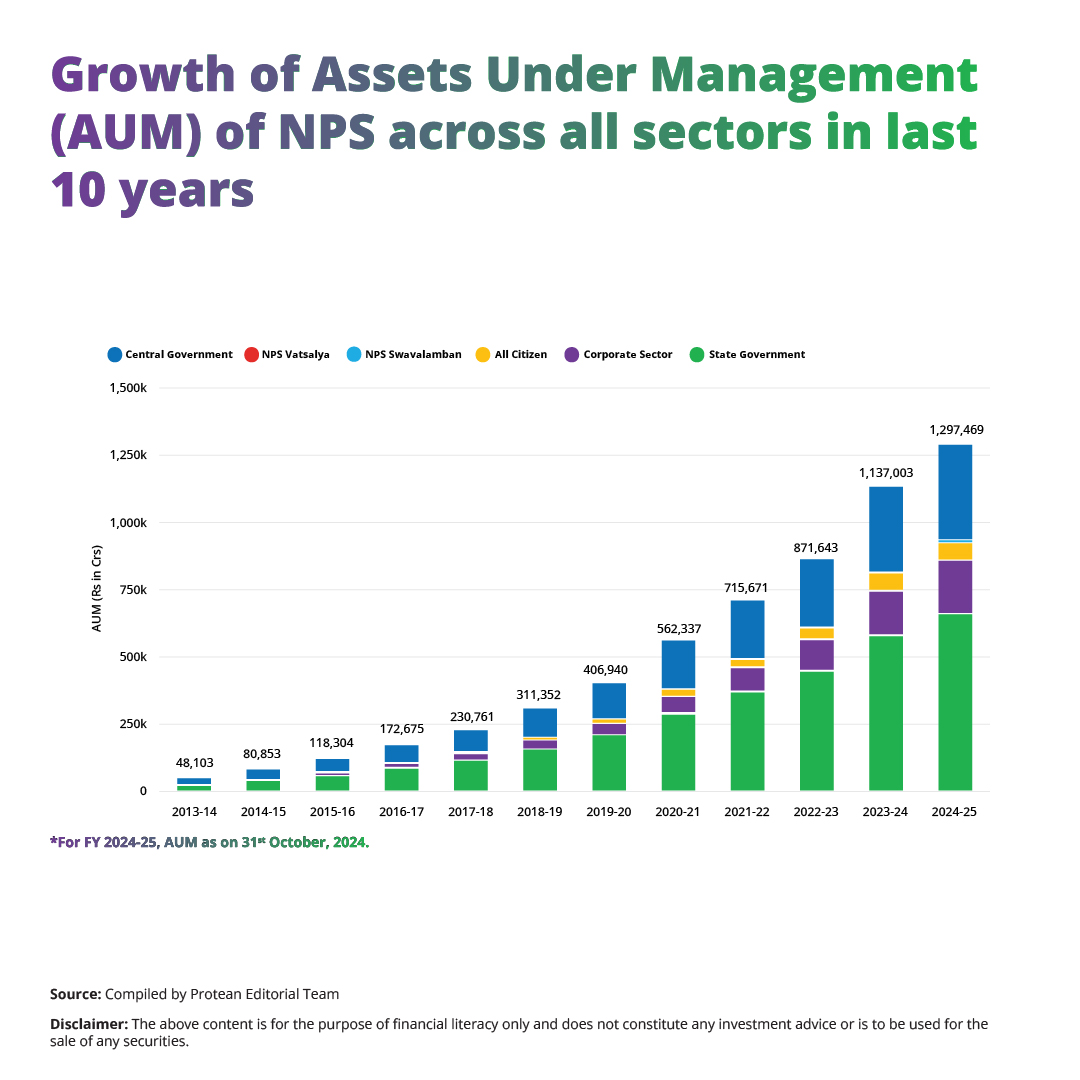

Growth of Assets Under Management (AUM) of NPS across all sectors in last 10 years

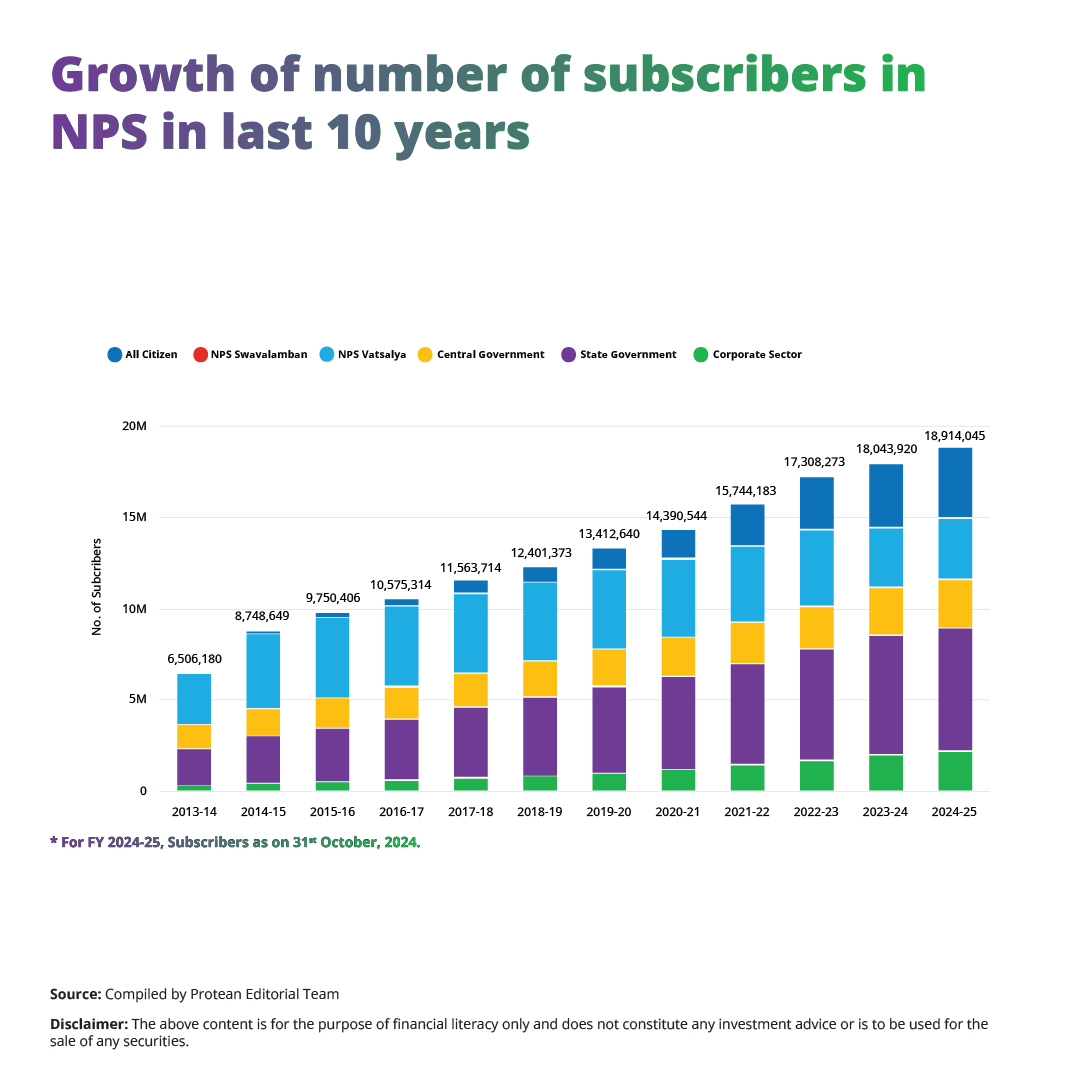

Growth of number of subscribers in NPS in last 10 years

Conclusion

NPS is a powerful tool for individuals looking to secure their financial future through disciplined, long-term savings. With its flexibility, transparency, and government-backed security, NPS offers a robust solution for retirement planning. Whether you're a salaried employee, a self-employed individual, or someone in the unorganized sector, NPS provides various options like NPS Lite and Atal Pension Yojana (APY) to cater to diverse needs.

Also Read:

Growing Your NPS Savings: Contributions and Account Management

NPS Vatsalya: Data-Driven Insights on Securing Your Child's Financial Future

Visual Guide: Step-by-Step Enrollment in NPS Vatsalya

How to Use an NPS Calculator for Retirement Planning?

NPS Vatsalya vs PPF & Mutual Funds: Which is Best for Child Savings in 2024?

Written by Bruhadeeswaran R.