You might have heard about Loan Against Securities. But did you know that you can access financial assistance against portions of your NPS corpus from regulated lenders? Yes, here’s another noteworthy benefit of NPS scheme investing.

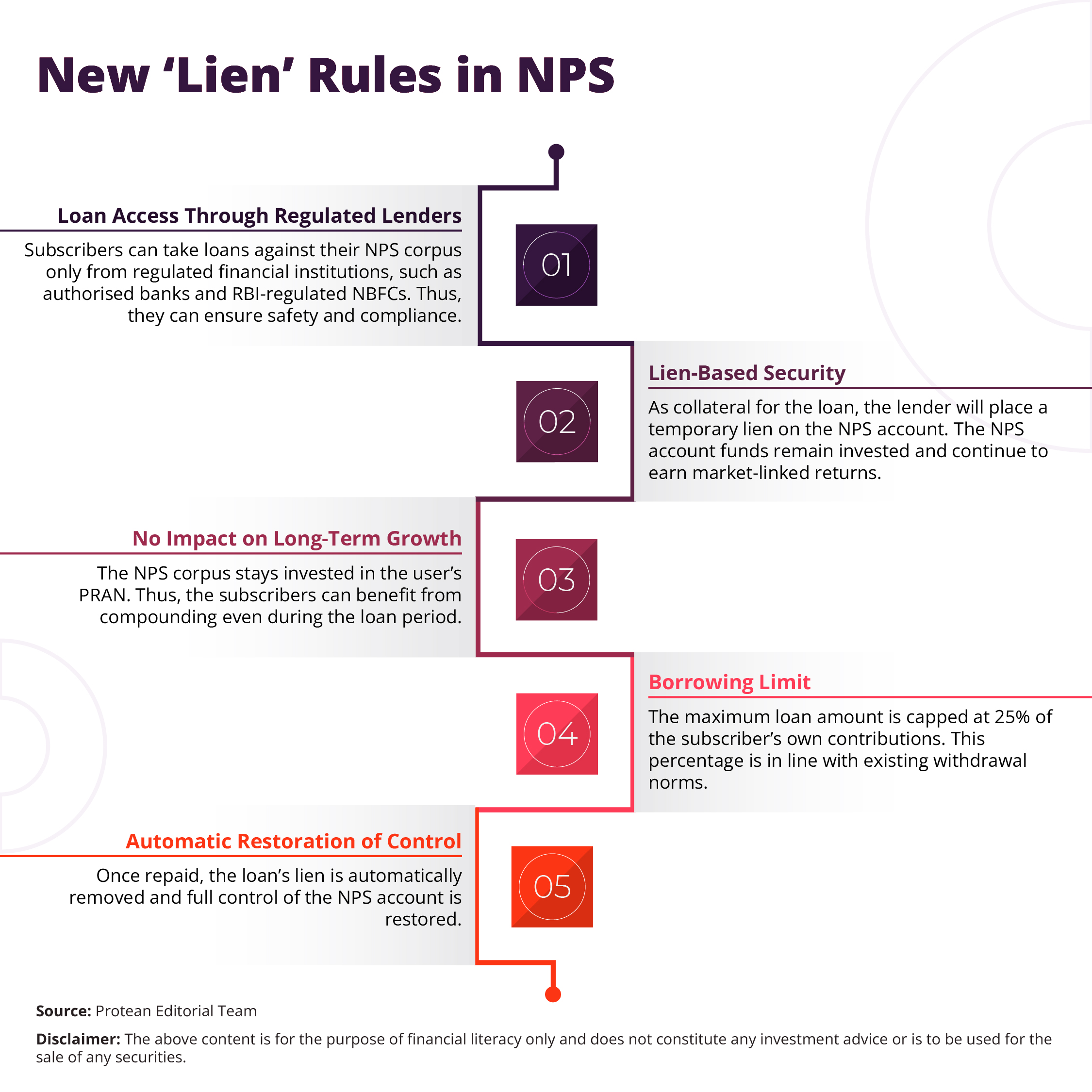

PFRDA has introduced a major enhancement in the NPS scheme. The latest (2025) reforms allow NPS account holders to access limited financial assistance against their retirement savings corpus (up to 25% of subscriber's own contributions).

With this new facility subscribers can meet short-term liquidity requirements as they remain invested in the NPS scheme through their PRAN (Permanent Retirement Account Number). It has permitted lenders to place a ‘lein’ on NPS accounts. With this, the system now offers an additional layer of financial flexibility without compromising long-term retirement planning.

Here’s how the new provision of the NPS account works and what it means for Tier-1 and Tier-2 account holders in 2026.

Understanding the New ‘Lien’ Rule on Your NPS Account

The updated PFRDA regulations allow subscribers to raise loans from regulated financial institutions by placing a lien on (keeping collateral) a portion of their NPS corpus. Meaning, the lender can hold a temporary charge on a specified part of the subscriber’s contributions as loan security or collateral.

Can You Use Your PRAN as Collateral?

Every NPS subscriber is assigned a PRAN. when you seek a loan against your NPS account, your PRAN itself isn’t pledged. But it acts as the unique identifier for marking the lien on the account.

As a subscriber, when you apply for a loan, the lender would coordinate with the CRA (Central Recordkeeping Agency) through the PRAN. It would then place the lien on the eligible portion of the NPS corpus. Thus, you can transparently and accurately track the pledged amount.

Through the loan tenure, the subscriber has the continuous NPS account ownership. Also, the subscriber would be the one getting the market return benefits.

Meaning, your retirement savings can keep growing even when you use them to support short-term financial needs.

Loan Against NPS vs. Partial Withdrawal

Now, with the NPS scheme reforms, the subscribers have two structured ways to access their funds:

- Partial withdrawal

- Loan against the account

Both allow access up to 25% of the subscriber's own contributions. Subscribers can choose based on their financial needs.

- With partial withdrawal subscribers can withdraw a portion of their contributions for specified purposes such as higher education, medical treatment, marriage or house purchase. The withdrawn amount would permanently reduce the retirement corpus.

- Loan against NPS allows borrowing from regulated institutions, secured by a lien on the account (up to 25% of own contributions). Investments remain intact, and full control restores upon repayment.

Important Considerations and Limitations

The lien facility adds flexibility for short-term liquidity. However, it is also important to follow certain conditions. Failing to plan the NPS lien facility can lead to mis-alignment of NPS investing to your financial goals.

- Loans can only be taken from regulated financial institutions.

- The maximum loan amount is capped at 25 per cent of your own contributions.

- Interest rates and repayment terms are decided by the lender.

- Your NPS investments continue to earn returns during the loan period.

- Defaulting on repayment may impact your financial standing and future borrowing ability.

Subscribers also need to remain vigilant against fraudulent schemes or unsolicited promises of loans against NPS outside the regulatory framework. PFRDA regularly cautions the public about scams targeting pension schemes. It is important to always deal with credible institutions and verify offers against official guidelines.

Conclusion

The introduction of loans against NPS is a progressive step in strengthening the scheme’s relevance for modern investors. With this, subscribers can address short-term financial requirements without disturbing their long-term retirement goals.

NPS account holders can combine disciplined investing with flexible access options. Thus, NPS continues to be a comprehensive retirement solution. Responsible usage of this facility can help subscribers manage life’s financial milestones while staying committed to their future security.

Frequently Asked Questions

Q1: Can I get a loan against my NPS PRAN before age 60?

Yes. The lien facility under the 2025 amendment does not require you to be at retirement age. You can approach a regulated lender during your working life to secure a loan against your eligible contributions.

Q2: Does a loan against NPS reduce my pension corpus?

No. A loan secured through a lien does not withdraw funds from your NPS account. It only allows credit against part of your contributions while your remaining corpus continues to earn returns.

Q3: What is the maximum loan amount I can secure?

Regulations cap the lien (and hence the loan) at 25% of your own contributions to NPS, not on the total accumulated corpus.

Q4: Can I use the loan for any purpose?

There is no strict regulatory limit on use, but lenders may set their own terms. Ensure you understand the lender’s conditions before borrowing.

Q5: Does this replace partial withdrawal?

No. Partial withdrawal and loans are separate mechanisms. Partial withdrawal permanently removes money from your NPS, while a loan is a temporary credit secured by a lien.