The Multiple Scheme Framework (MSF) offers a customizable structure tailored to non-government subscribers' retirement planning needs. It is a new framework under the National Pension System (NPS) that enables subscribers to hold multiple schemes. The introduction of the Multiple Scheme Framework upgrades NPS investing for non-government subscribers with features like multiple schemes and flexible asset allocation.

Here is more on MSF in NPS and how it enables multiple schemes with flexible risk profiles.

What is the Multiple Scheme Framework (MSF)?

With MSF, the fundamental architecture of how the NPS operates is changed. Previously, a subscriber was identified by their Permanent Retirement Account Number (PRAN) and could link one active investment scheme to it. You could also change your strategy, by switching your entire corpus.

Under the new MSF guidelines, your Permanent Account Number (PAN) enables aggregation across CRAs, while PRAN remains the account identifier at each CRA.

PAN unifies holdings across CRAs for consolidated reporting, but schemes are held under PRAN per CRA identifier. With this, you can map multiple distinct investment schemes to a single PRAN.

This is similar to having a single bank account (PRAN) that can hold multiple distinct fixed deposits or mutual fund folios.

Therefore, now, you can split your retirement savings into different "buckets." Each of these buckets has its own Pension Fund Manager (PFM), asset allocation, and risk profile. With this flexibility, your NPS scheme can better align with your financial goals, thus offering a higher level of customisation.

Unlocking 100% Equity Investing for Wealth Creation

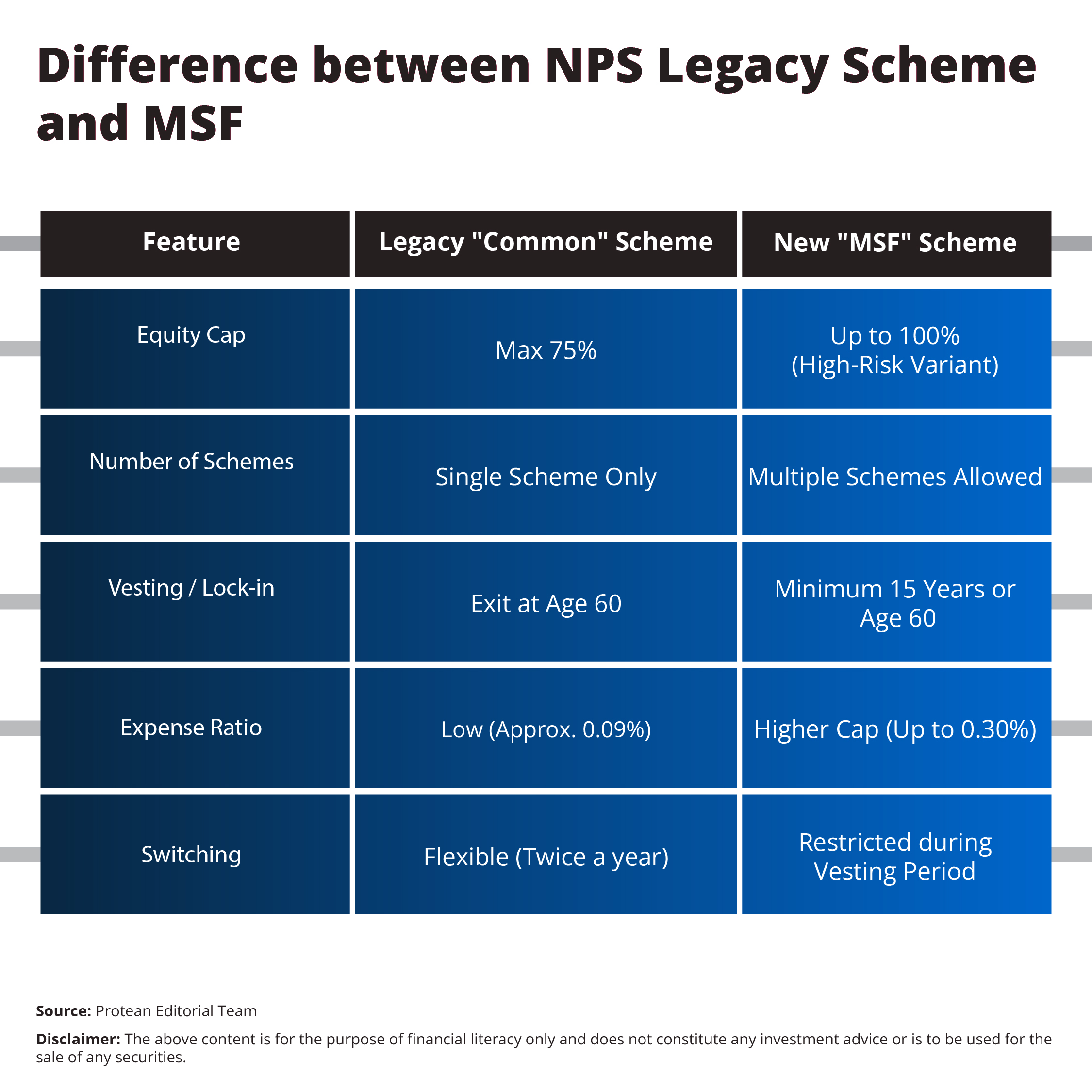

One of the most-important features of the Multiple Scheme Framework is the removal of the traditional safety brakes for aggressive investors, which was earlier capped at 75% equity exposure. With this risk-tolerant subscribers can maximise their wealth creation during the early years of their careers.

With the MSF, PFRDA has introduced "High-Risk" scheme variants. With these specific schemes investors can allocate up to 100% in equity. So, if you are in your 20s or 30s, you can now designate a portion of your monthly contribution to a pure equity NPS scheme. Thus, you can capture the full upside of the market without any dilution from debt instruments.

The multiple scheme framework supports the well-known 'Core and Satellite' investment strategy, allowing you to balance stable core investments with aggressive satellite schemes. Here, you can use a dual approach:

- Keep your primary retirement corpus (the Core) in a balanced, safe scheme

- Allocating a smaller portion of your funds (the Satellite) to a 100% equity scheme for aggressive growth.

Thus, you can aim for higher returns while maintaining a safety net, making the new pension scheme a comprehensive wealth-management tool.

Strategic Flexibility in Investment and Switching

The Multiple Scheme Framework is about strategic freedom. It acknowledges that your financial personality is complex. With MSF, you can invest in multiple schemes simultaneously under the same PRAN.

However, the new schemes opened under the MSF come with a mandatory "vesting period," typically set at 15 years or until the age of 60. You cannot switch funds between two MSF schemes during this lock-in period. With this rule, you can prevent impulsive trading and ensure that the NPS remains a long-term retirement product rather than a short-term speculative tool.

You will retain the flexibility to switch from a new MSF scheme back to the traditional "Common Scheme" (legacy NPS schemes) if you feel the risk is too high. This one-way street ensures that while you can experiment with aggressive strategies, you always have a retreat path to safety. This thoughtful design makes NPS investing both adventurous and secure.

Cost, Transparency, and Making the Right Choice

The new schemes under the MSF operate with a higher expense ratio cap compared to the ultra-low-cost legacy schemes. This is the price of active management and higher equity potential.

It is vital to weigh these costs against the potential for higher alpha (returns) that a 100% equity NPS scheme can generate.

Here is a quick comparison to help you decide:

Your CRA portal (like Protean eGov Technologies Ltd.) will now provide a consolidated dashboard. You can track the performance of each NPS scheme individually, viewing separate Net Asset Values (NAVs) and returns. This granular data empowers you to make informed decisions about where to direct your future contributions.

Conclusion

The Multiple Scheme Framework has effectively redefined NPS for the modern Indian investor. It is breaking the shackles of the "average" strategy, allowing you to build a portfolio that is as unique as your fingerprint.

So, whether you want the thrill of 100% equity or the precision of multiple fund managers, the MSF can deliver it all under one roof.

This evolution can bridge the gap between the safety of a pension plan and the agility of a mutual fund. Thus, you can ensure that your NPS investing strategy works as hard as you do, securing a wealthier and more comfortable tomorrow by taking advantage of this flexible savings option.

Frequently Asked Questions

1. Can I have two PRAN cards if I opt for the Multiple Scheme Framework?

No, you cannot have two PRAN cards. The Multiple Scheme Framework works on the principle of "One PAN, One PRAN, Multiple Schemes." You will continue to use your existing PRAN to manage all your different portfolios. The multiple schemes are internal subdivisions within your single account.

2. Is the 100% equity option available to government employees?

Currently, the MSF and its 100% equity option are primarily available to the "Non-Government Sector," which includes the All Citizen Model and Corporate Model subscribers. Government employees generally follow a different set of investment guidelines and cannot access MSF or 100% equity options.

3. What happens if I want to exit an MSF scheme before 15 years?

New schemes under the multiple scheme framework have a mandatory vesting period of 15 years. You typically cannot fully exit or withdraw from these specific schemes before this period ends, unless you are exiting the NPS entirely due to specific circumstances like death or terminal illness. However, you can stop contributing to the MSF scheme and direct new funds to your Common Scheme.

4. Does the higher expense ratio of MSF schemes affect my returns significantly?

While the expense ratio for MSF schemes is higher (up to 0.30%) than the traditional schemes (0.09%), it is still significantly lower than active mutual funds, which can charge 1.5% to 2.0%. If the 100% equity NPS scheme delivers superior market-linked returns over 15 years, the slightly higher cost is often negligible compared to the gains.