Let’s discuss API! Starting with what is an API would be relevant.

The answer to this question might be more relevant than ever if you are a technology leader.

API or Application Programming Interface is a structured set of rules and protocols. These allow different software applications to communicate with each other.

APIs can enable different systems to exchange data and execute functions in a seamless and secure manner. They can work without disclosing their underlying code or internal architecture.

Why APIs are Indispensable for Modern Banking

APIs have emerged as a cornerstone technology to address the challenges digitise, innovate, and deliver better customer experiences, while remaining compliant and secure.

1. Digital Transformation

What is the value of an API if it doesn’t modernise legacy systems?

APIs can help them upgrade easily, integrate cloud, and deploy faster without a full system overhaul.

2. Enhanced Customer Experience

Banking APIs can make real-time transactions, personalise dashboards, and multi-channel support possible. Banking APIs can enable seamless user journeys.

3. Innovation and Fintech Collaboration

APIs are the foundation of Open Banking. Here, banks expose select data and services to trusted third-party providers. This collaborative ecosystem can foster innovation and allow fintech companies to develop automated solutions. These can be budgeting tools, robo-advisors, or alternative lending platforms.

4. Operational Efficiency

APIs can reduce manual interventions by automating back-end processes like reconciliations, loan underwriting, or KYC verifications. This can not only decrease turnaround time, but also curtail human errors, improve compliance, and reduce operational costs.

5. Competitive Edge

As customers now expect fast, seamless service like that of tech giants and fintechs, traditional banks need to stay flexible and adapt quickly. APIs can empower institutions to launch new products quickly, adapt to regulatory changes, and respond to evolving customer demands with speed and precision.

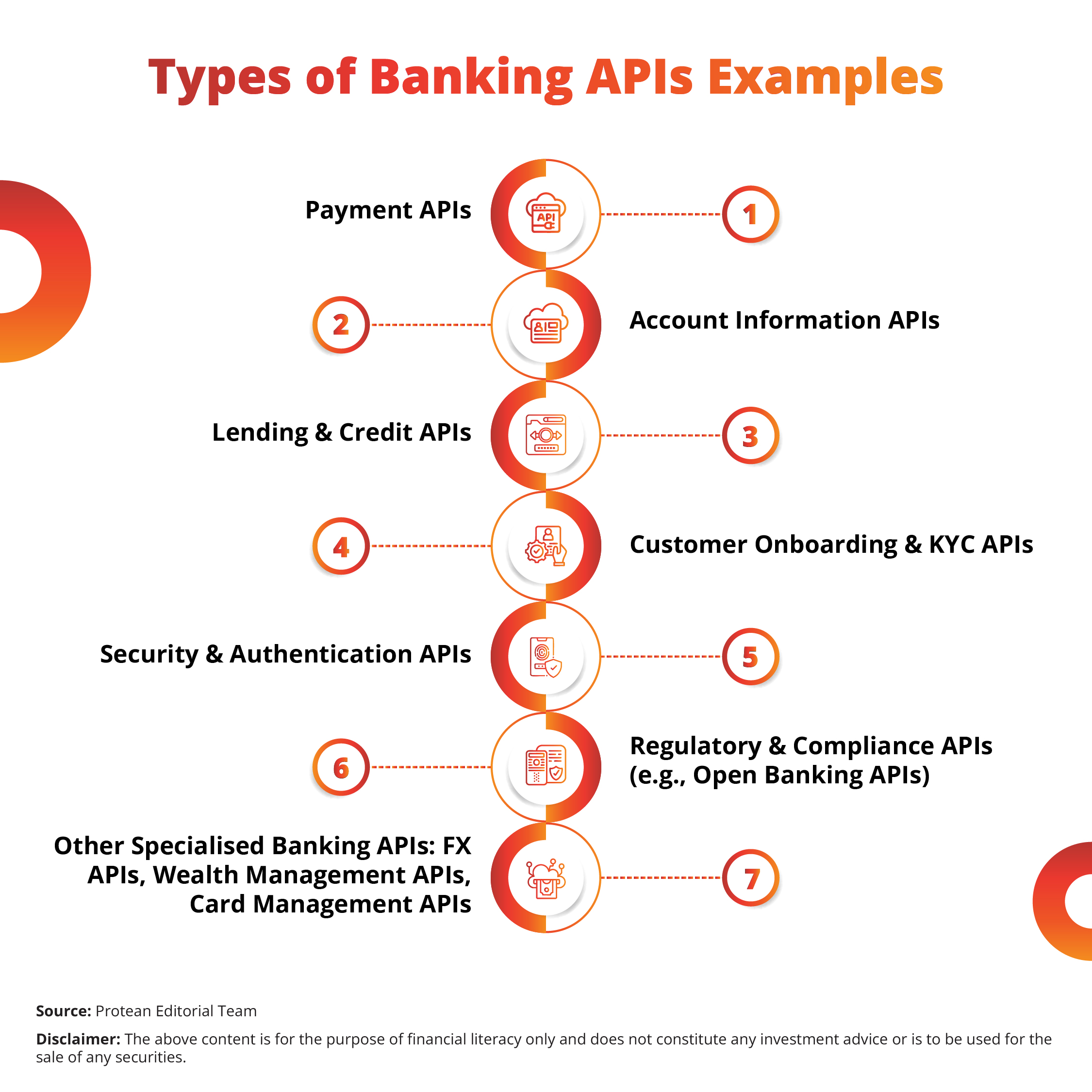

Exploring the Different Types of Banking APIs

Now that we understand what is an API and its role in banking, let us explore the different types of Banking APIs and their specific functions.

1. Payment APIs

These APIs can enable digital payments across channels. These can be related to:

- Initiating a UPI transaction,

- Integrating with a payment gateway

- Executing bulk disbursements.

Payment APIs can ensure money to move swiftly, securely, and in real-time.

Example: A fintech app using a Payment API can allow users to pay utility bills directly from their bank accounts.

2. Account Information APIs

These can allow secure access to user account details. These can be details such as balances, transaction history, account status shared typically with the user’s consent. These APIs are often part of open banking frameworks. They can support financial planning, budgeting apps, and credit scoring models.

Example: A wealth advisory platform can fetch a user’s bank transaction data to offer tailored investment advice.

3. Lending and Credit APIs

What is API usage in the lending and credit ecosystem?

It is widely used by lenders and credit platforms to:

- Assess eligibility

- Verify income

- Automate loan approval workflows.

These APIs can integrate with credit bureaus, bank accounts, and alternative data sources to power faster, more accurate lending decisions.

Example: A digital lender can use APIs to fetch salary credits from bank statements and offer pre-approved loans instantly.

4. Customer Onboarding and KYC APIs

These APIs can facilitate paperless onboarding.

They can do this by:

- Pulling data from government sources (like Aadhaar, PAN)

- Verifying customer identities.

With this, banks and NBFCs can drastically reduce:

- Turnaround times

- Enhance customer acquisition

Example: A neobank can help customers open an account in under 5-minutes by using Aadhaar-based eKYC APIs.

5. Security and Authentication APIs

These APIs can manage the following:

- Multi-factor authentication (OTP, biometric)

- Session control

- Token-based access to protect sensitive data

- Prevent unauthorised transactions.

Example: A mobile banking app can use biometric authentication APIs to allow secure login and transaction approval.

6. Regulatory and Compliance APIs

In the Indian context, these APIs support compliance with regulatory frameworks such as RBI’s Account Aggregator system and the Central KYC (CKYC) registry. These API types can help financial institutions efficiently:

- Report

- Monitor

- Audit transactions

Example: An NBFC can use regulatory APIs to submit real-time data to central repositories as per RBI guidelines.

7. Other Specialised Banking APIs

These can be:

- Foreign Exchange (FX) APIs

- Wealth Management APIs

- Card Management APIs

They can create opportunities for banks to embed financial services into broader platforms. They can be used in travel booking apps that offer embedded insurance to e-commerce sites that provide instant credit options.

Get an API for your banking needs, choose RISE with Protean.

Conclusion

So, what is an API? APIs are strategic assets that can enable banks and financial institutions to innovate, scale, and thrive in a digital economy.

APIs are evolving as an invisible engine that can power agility, security, and innovation. For banks, fintechs, and developers alike, embracing the API economy is not just a competitive advantage, it is a business imperative. Get in touch with us now; know more about RISE with Protean.