Have you heard about the National Pension System, or the NPS scheme? To start with, it’s a scheme that can help you invest to build a strong retirement corpus.

Securing a comfortable retirement requires diligent and early planning. For many Indians looking for a stable financial future, the National Pension System can offer a structured path towards self-sufficiency after their working years.

Thus, it is crucial to understand the core aspects of the NPS scheme as a first step toward building a strong retirement corpus.

Let us look at the nitty-gritty details of the National Pension System:

The Basics - What is NPS, Exactly?

The National Pension System is a voluntary, long-term retirement savings scheme. It is an investment product designed to provide a steady income post-retirement.

It was launched by the Government of India (GOI) and is regulated by the Pension Fund Regulatory and Development Authority (PFRDA). The NPS scheme has adopted a defined contribution system. Here, your contributions can be invested in a mix of market-linked instruments to generate returns over the long term.

At its core, the NPS has two types of accounts, i.e. Tier I account and Tier II account. Here are their details:

- The Tier-I Account is the primary retirement account. It has mandatory contribution and conditional early withdrawal rules. The NPS tax benefits are associated exclusively with this account.

- The Tier-II Account is a voluntary savings account. You can only open a Tier-II account if you already have an active Tier-I account. With the Tier II NPS account you can get flexibility for deposits and withdrawals, functioning.

Thus, the NPS scheme can be a powerful tool, combining disciplined, long-term savings with an element of liquidity.

Let us now look at the top five questions about the NPS Scheme.

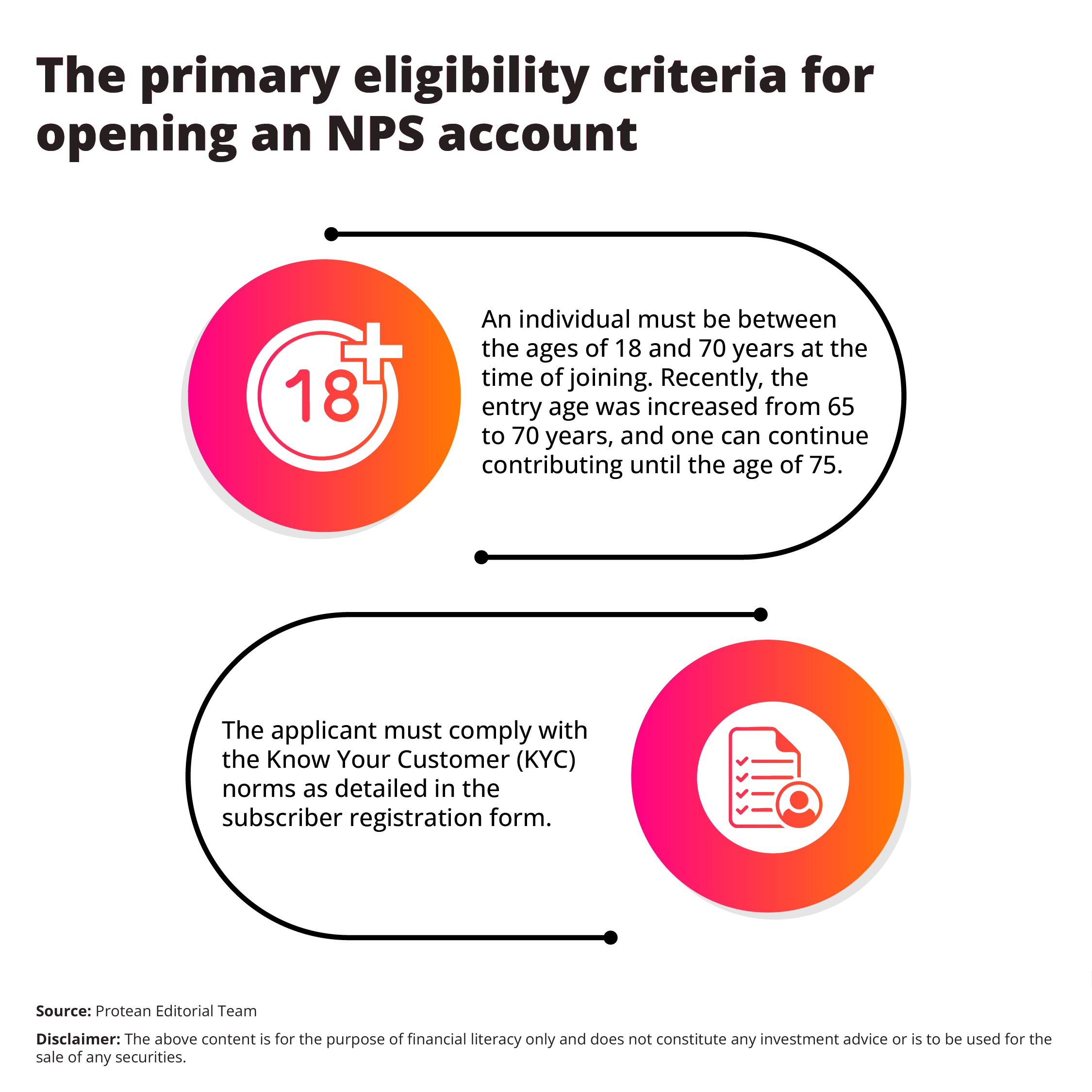

Question 1 - Who Can Open an NPS Account?

The accessibility of the National Pension System can be one of the noteworthy advantages. The eligibility criteria for the NPS scheme are broad.

It can accommodate a vast section of the population to plan for their retirement.

Any citizen of India, whether resident or non-resident (NRI), can open an NPS account.

The primary eligibility criteria are as follows:

This inclusive approach can mean that the NPS is available to everyone (from salaried employees in the private sector and government employees to self-employed professionals and business owners).

Question 2 - How Can the NPS Scheme Help Me Save on Taxes?

The NPS scheme can provide a unique three-tiered tax deduction structure. It can allow you to significantly lower your taxable income.

Let's break down these NPS benefits:

- Deduction under Section 80CCD(1): Your own contributions to the NPS Tier-I account are eligible for a tax deduction under Section 80CCD(1) of the Income Tax Act. This deduction is part of the overall limit of ₹1.5 lakh available under Section 80C. For a salaried individual, the deduction is capped at 10% of their salary (Basic + Dearness Allowance), and for self-employed individuals, it is capped at 20% of their gross annual income.

- Exclusive Deduction under Section 80CCD(1B): This is the game-changer. The National Pension System offers an exclusive, additional tax deduction of up to ₹50,000 for contributions made to the Tier-I account. This benefit is over and above the ₹1.5 lakh limit of Section 80C. This means you can claim a total deduction of up to ₹2 lakh (₹1.5 lakh under 80C/80CCD(1) + ₹50,000 under 80CCD(1B)), making it one of the most effective tax-saving instruments available.

- Deduction on Employer's Contribution under Section 80CCD(2): For salaried individuals, there is a further tax benefit. When an employer contributes to an employee's NPS account, that contribution is also eligible for a tax deduction. The employee can claim a deduction of up to 10% of their salary (Basic + DA) for contributions made by the employer. For central and state government employees, this limit is higher at 14%. This amount does not fall under the ₹1.5 lakh or the ₹50,000 limits, providing a substantial additional avenue for tax saving.

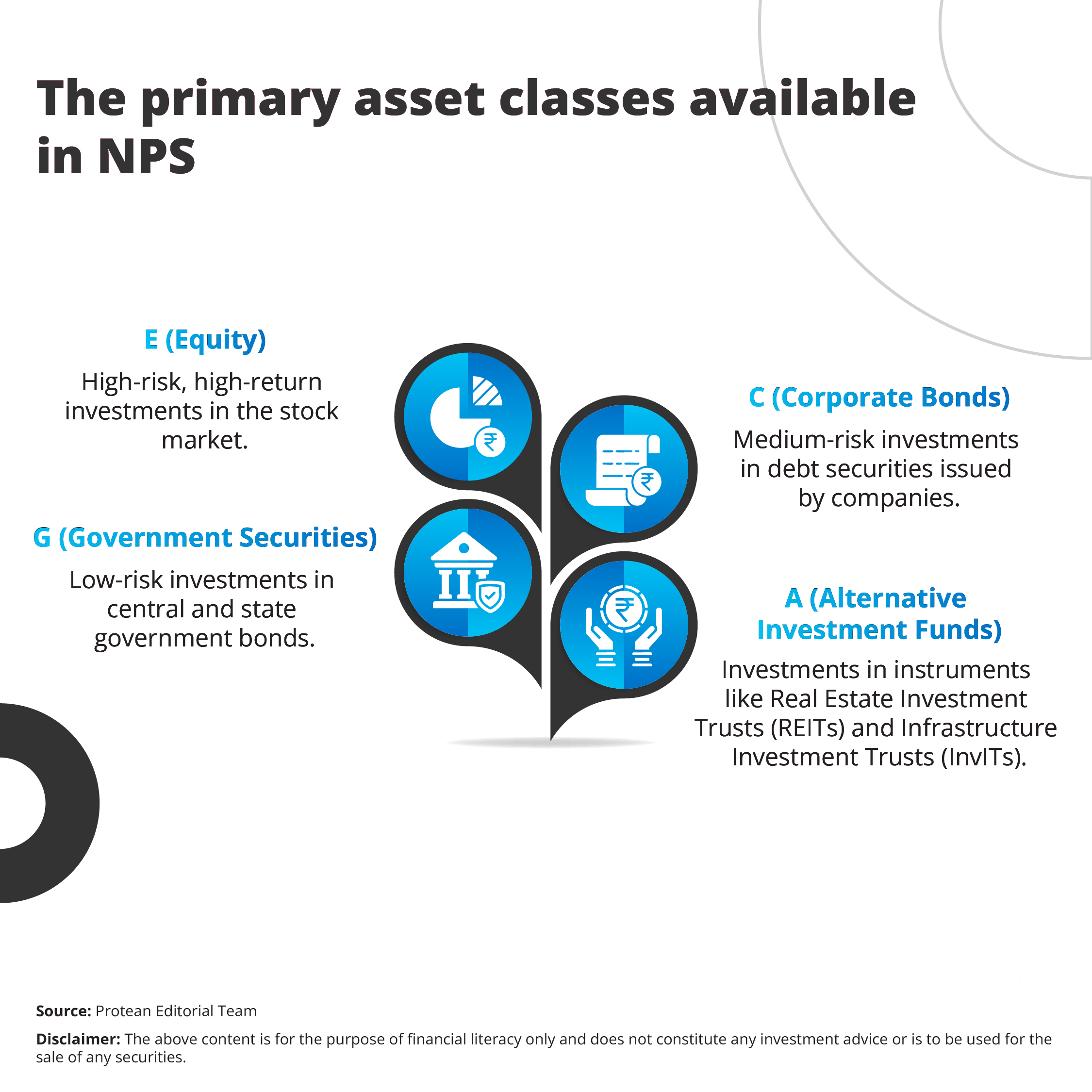

Question 3 - How Does the NPS Investment Work?

When you invest in NPS, your money is managed by professional Pension Fund Managers (PFMs) registered with the PFRDA.

You also have the choice to decide how your contributions are invested across different asset classes.

Furthermore, you can choose your investment strategy through two options. These are Active Choice and Auto Choice.

Question 4 - What Are the Rules for Withdrawal and Maturity?

The withdrawal rules for the NPS scheme are designed to ensure the primary objective of retirement planning is met.

Let’s learn more about them:

- With Partial Withdrawal a subscriber can make a partial withdrawal from their Tier-I account after completing three years in the system. These withdrawals are permitted only for specific purposes.

- With the Maturity at Age 60 (or Superannuation), you can withdraw up to 60% of your accumulated corpus as a lump sum, upon reaching the age of 60. This amount is completely tax-free. The remaining 40% of the corpus must be used to purchase an annuity plan from an IRDAI-regulated annuity service provider.

- With Premature Exit (Before Age 60), If you decide to exit the NPS before reaching the age of 60, you can withdraw a maximum of 20% of the corpus as a lump sum. The balance of 80% must be used to purchase an annuity. A full withdrawal is only permitted if the total accumulated corpus is less than or equal to ₹2.5 lakh.

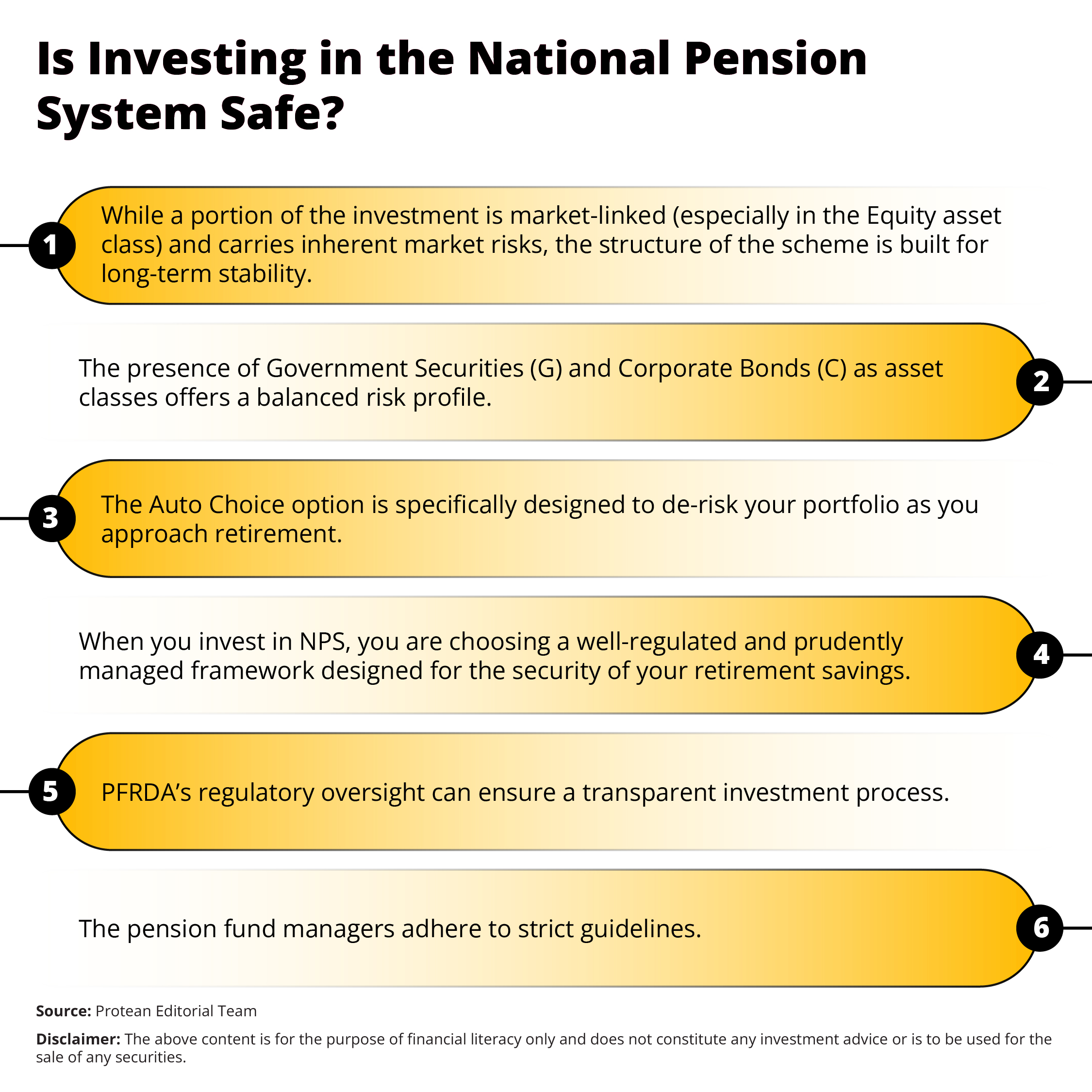

Question 5 - Is Investing in the National Pension System Safe?

Here are a few details that might confirm the safety component in NPS scheme:

Conclusion

The NPS scheme can be a robust and secure platform for building a substantial retirement corpus. It can empower individuals from all walks of life to take control of their financial future and work towards a financially independent and dignified retired life.