Recent National Pension System (NPS) updates have marked the 2026 calendar as an important window for the silver economy.

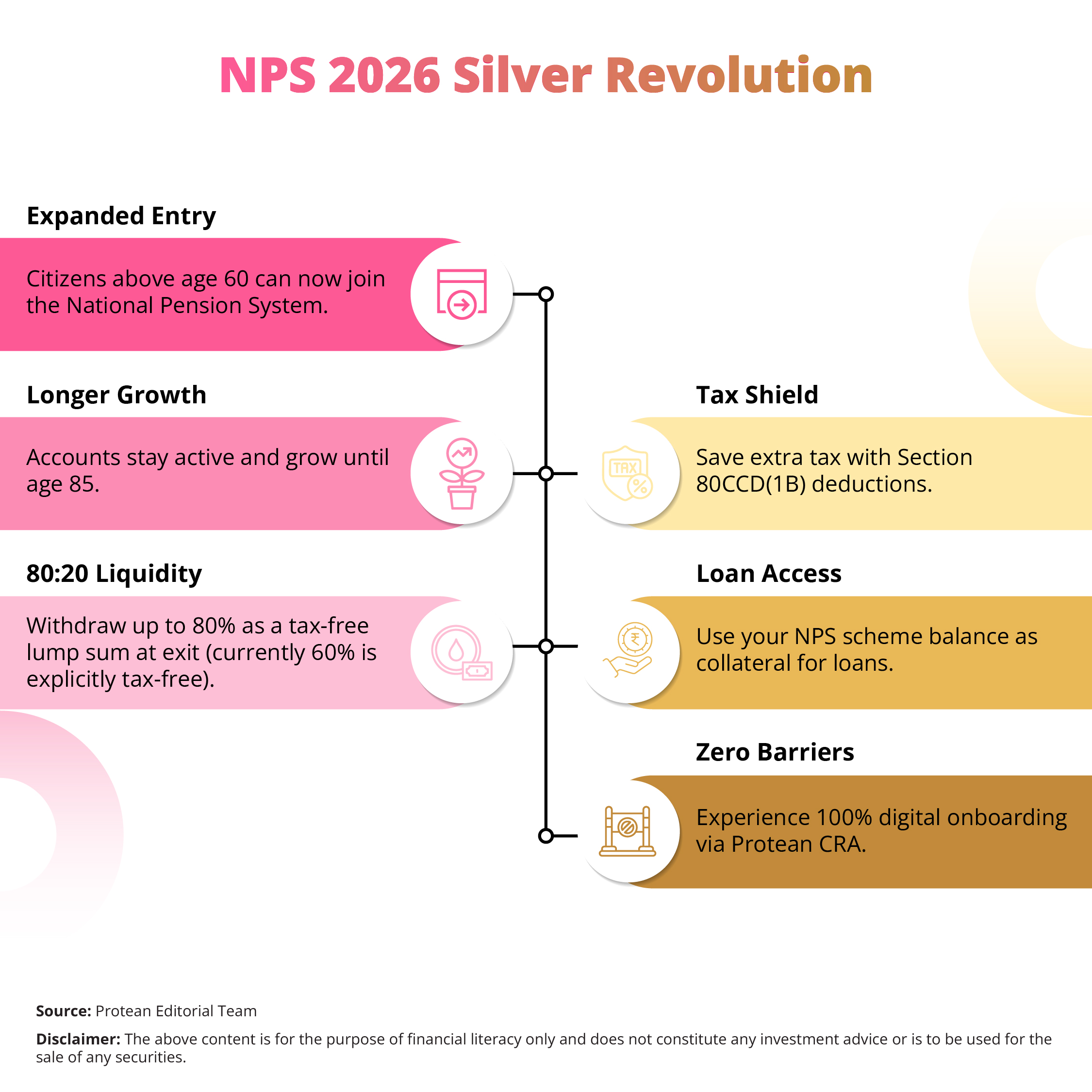

In December 2025, PFRDA increased the maximum entry and continuation ages for NPS schemes. Individuals, earlier, faced rigid barriers at age 70 or 75 (for government or non-government subscribers, respectively).

However, the age limit for account continuation has now been extended to 85 years. This is an important change, positioning the NPS as a powerful tool for wealth preservation.

Now, investors in their late 60s or 70s can find a viable home for their accumulated capital, and invest flexibly and easily.

Therefore, 2026 is a critical window as the NPS scheme now bridges the gap between retirement and legacy planning.

Redefining Liquidity for Late Entrants

Here is how NPS entry at 85 years can redefine liquidity for late entrants.

Annuity Purchase

Earlier, a minimum 40% annuity purchase on exit was mandatory in NPS. Investors above 60 years of age require higher cash flows for medical or lifestyle needs.

Now, with the revised NPS norms, retirees require only a 20% annuity (for non-government subscribers). Thus, subscribers can pull out 80% as a lump sum though currently only 60% is explicitly tax-free under the Income Tax Act. This high liquidity ratio can be better for wealth reallocation after the age of 60.

Higher Lump Sum Payout

With a higher lump sum payout, investors can have the freedom to invest in other debt or equity instruments. They have the remaining 20% annuity as a reliable safety net.

The remaining annuity, can provide a steady monthly income stream. With this 80:20 split, an NPS scheme can provide both flexibility and security for silver-age investors. The late entrants can also benefit from this high-speed liquidity window.

Strategic Tax Planning in the Post-Retirement Phase

In 2026, the NPS scheme can enable strategic tax planning. Here is how the new NPS norms can help late entrants.

Section 80CCD(1B)

Late entrants (i.e., subscribers starting NPS post-age 60) can utilise Section 80CCD(1B) of the Income Tax (IT) Act to claim an additional tax deduction of ₹50,000 for Tier- 1 investments under the old tax regime (non-government employees). This benefit would apply over and above the standard Section 80C limit of ₹1.5 lakh.

Tax-free Capital Gains During Accumulation Phase

With NPS, individuals can avail tax-free capital gains during the entire accumulation phase. So, when an individual stays invested until age 85, they can defer taxes on these gains for an extra decade. This long-term deferral can have a powerful compounding effect for the retirement corpus.

Thus, the NPS scheme can serve as a strategic tax shelter for retirees trying to minimise their annual tax outgo.

The Operational Leap: Vesting & Collateral

The operational framework of the National Pension System also improves for post-60 entrants this year. However, the new rules simplify the exit process for those who join later in life.

Use NPS as Collateral

In 2026, with the new provision, subscribers can use their NPS balance as collateral for loans. Senior citizen investors can get an emergency liquidity buffer without the need to close their accounts.

Meeting Goals & Managing Emergencies

Now, NPS investors do not need to sacrifice long-term growth for accessing funds for urgent medical requirements or family obligations. Thus, the NPS scheme adds a layer of financial security that was earlier unavailable to late entrants.

Here’s how the National Pension System has evolved into a multi-purpose financial instrument.

- Late entrants (investors joining post age 60) do not have a minimum lock-in period.

- Subscribers can choose between ‘Active Choice’ and ‘Auto Choice’ for asset allocation.

- The Tier II account can provide even greater liquidity without any lock-in.

Conclusion: NPS Evolution From Pension to Wealth Optimisation

In 2026, the entry-exit barriers for NPS schemes have finally relaxed. The focus of the national pension system has now moved towards holistic "wealth optimisation."

These relaxed 80:20 liquidity norms have made the platform effective for non-government senior citizens seeking greater control over their retirement corpus. With an immediate entry later in life, investors can benefit from current market cycles and expert fund management. Evaluate this window to optimise your post-retirement portfolio through Protean eGov Technologies now.

Frequently Asked Questions (FAQs)

Q1: Can a 75-year-old individual open a new NPS account in 2026?

Yes. In 2026, any Indian citizen up to age 70 can open a new account. Then, they can continue to invest until they reach 85 years of age with the National Pension System.

Q2: Is there a lock-in period for those joining the NPS scheme after 60?

No. Earlier there was a minimum lock-in period (vesting period) of three years for late entrants. Now, under the new rules, the vesting period is removed for those joining post age 60.

Q3: How much can a post-60 entrant withdraw as a lump sum?

Under the ‘All Citizens’ model non-government investors can can withdraw up to 80% of the corpus as a tax-free lump sum. The remaining 20% needs to go towards a mandatory annuity to provide a regular pension stream.

Q4: Does the 80:20 rule apply to Central Government employees as well?

No. The 80:20 liquidity rule is currently applicable only to the ‘All Citizen Model’ and the ‘Corporate Model.’ Government employees still follow the traditional 60:40 structure for the NPS scheme.

Q5: What are the asset classes available in the national pension system?

Subscribers can choose between four asset classes i.e., Equity (E), Corporate Bonds (C), Government Securities (G), and Alternate Assets (A). Generally, late entrants can balance these classes to achieve stable growth with moderate risk.