Wondering what benefits NPS can offer? The new National Pension System (NPS) withdrawal rules have evolved the financial independence journey for the Indian workforce.

Indian Millennials and Gen Z are increasingly seeking early retirement. For such financial goals, high-growth assets and flexible liquidity options can provide a strong foundation.

Recent updates to the NPS withdrawal framework has transformed NPS investing from a passive tax-saver into an active wealth-creation engine. Let us learn more about the effective management of NPS withdrawals to navigate retirement planning in 2026 with maximum financial efficiency.

How Can NPS Help You Retire at 45 in India?

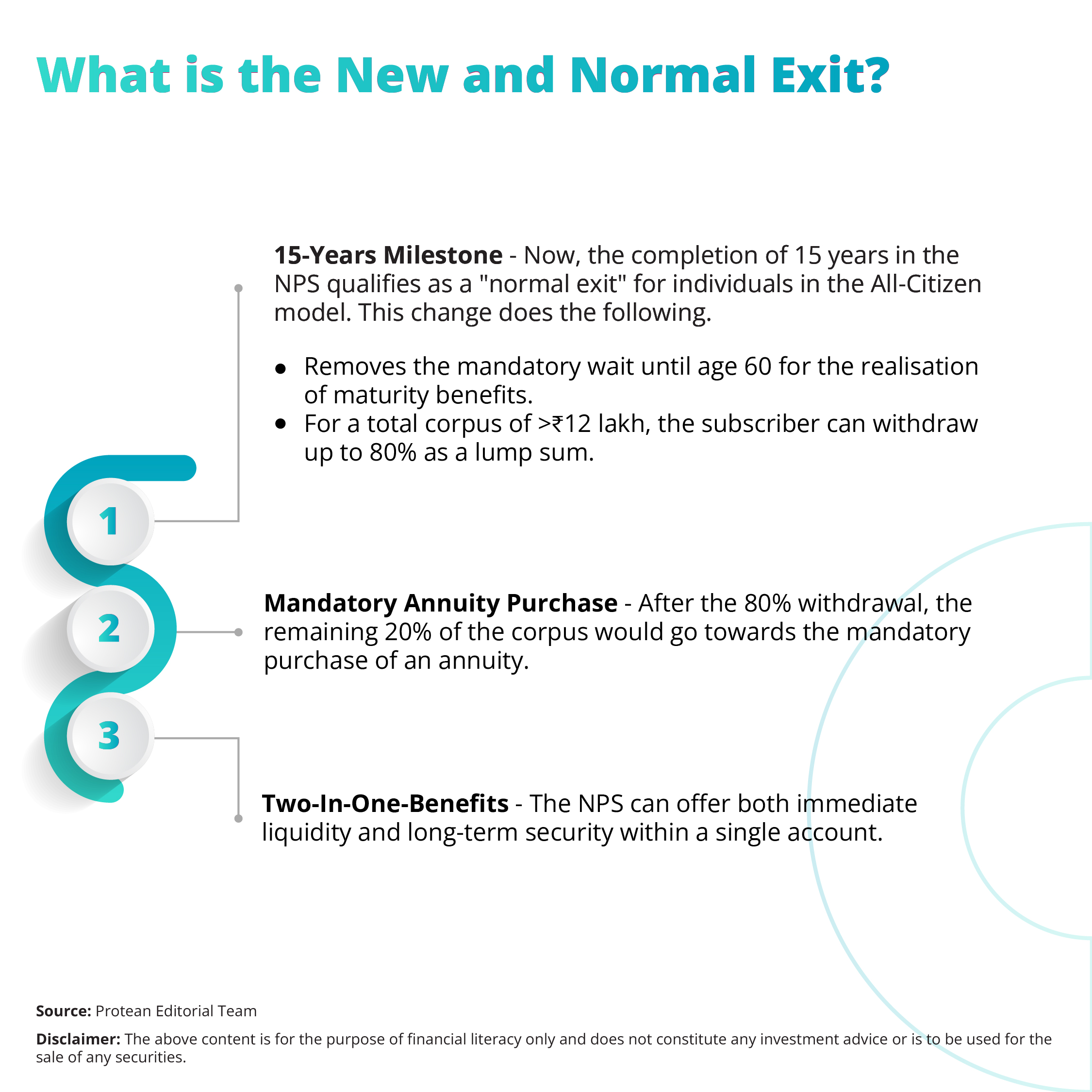

If you are a 30 year old, who is planning to retire at the age of 45, you have 15 years of consistent contributions with the new NPS withdrawal rules.

- When you (the subscriber) hit the age of 45, the 80% NPS withdrawal would become the cornerstone of your "active retirement" years.

- Here, your retirement period can involve travel, career pivots, or the pursuit of long-held passions without the pressure of a monthly salary.

- With the NPS capital, you can have the financial cushion required to transition away from a full-time job safely.

- For corpus over ₹12 lakh, the mandatory 20% annuity can provide a baseline for post-retirement expenses.

How to Minimise the Tax Bite on NPS Exit?

Tax treatment is an important factor when a subscriber decides between a lumpsum payout and a regular annuity income.

- Under the recent PFRDA updates, a tax-free Tier 1 NPS withdrawal of up to 80% of the total corpus upon maturity is allowed for non-government subscribers.

- The remaining portion of up to the allowed 20% (annuity income received in subsequent years) would remain taxable under the current income tax slab for non-government subscribers.

- High-income earners often look for strategies to defer tax by choosing a deferred annuity start date.

A premature exit significantly alters the total tax liability for the investor.

- If a person leaves the scheme before the completion of the 15-year period, the rules mandate a different withdrawal ratio.

- The NPS withdrawal rules emphasise the importance of timing to minimise unnecessary tax drains.

Every decision regarding the timing of an NPS withdrawal has a direct impact on the net returns.

Navigate the Exit Process with Ease

NPS investors balance liquidity and optimise tax savings by .

- Failure to update bank account details before the initiation of an NPS withdrawal request.

- Selection of an inappropriate annuity service provider without a comparison of current yield rates.

- Miscalculation of the taxable portion of the lump sum that exceeds the 60% threshold.

- Delay in the submission of the digital withdrawal forms to the Central Recordkeeping Agency.

- Disregard for the mandatory lock-in periods for partial withdrawals under the NPS withdrawal rules.

Conclusion

You can benefit from the combination of the 15-year rule and 100% equity exposure to create a powerful early retirement engine for the Indian workforce.

The new NPS withdrawal norms offer a flexible primary retirement instrument for your early retirement dreams. The Multiple Scheme Framework provides the necessary agility to navigate changing market conditions.

Subscribers can leverage the NPS withdrawal rules to build a secure and free future on their own terms. Early retirement becomes a reality when you use the system to its full potential today.

Frequently Asked Questions (FAQs)

Q1: Is the 100% NPS withdrawal allowed for small corpuses?

Yes. The rules allow for a full lumpsum NPS withdrawal if the total corpus amount is less than ₹8 lakh at the time of a normal exit. This provision ensures that the investor receives their entire wealth without the need for an annuity.

Q2: Are partial withdrawals from NPS taxable?

Partial withdrawals made for specific reasons as per the NPS withdrawal rules currently enjoy tax-exempt status. This applies to 25% of the subscriber's own contributions. The rules permit up to four such withdrawals during the entire tenure.

Q3: Can I continue to invest in NPS after age 60?

Both government and non-government subscribers can extend their investment tenure up to the age of 85. Thus, investors can avail continued growth and tax-deferred compounding even after formal retirement.

Q4: Do corporate subscribers qualify for the 15-year normal exit?

The 15-year normal exit rule covers all non-government sectors, including both the ‘Corporate’ and ‘All-Citizen’ models. Thus, with the new NPS withdrawal rules, the corporate professionals can plan for an early retirement with complete confidence.

Q5: What is the benefit of the Systematic Lump sum Withdrawal (SLW) facility?

With the Systematic Lump sum Withdrawal (SLW) investors gain a structured way to access the lump sum portion of the NPS. Here, investors can choose a one-time NPS withdrawal, for periodic payouts on a monthly, quarterly, or half-yearly basis. With this feature, subscribers can let the unpaid portion of the corpus remain in the NPS. Thus, they can benefit from market growth until the age of 85. It transforms a one-time payout into a steady stream and maintains liquidity for the retiree.