Starting a savings habit at an early age lays the foundation for financial stability later in life. The NPS Vatsalya Scheme has been designed precisely for this purpose. It allows parents or guardians to open a pension account on behalf of their child, ensuring that saving becomes part of the child’s journey from the very beginning.

This blog explains the NPS Vatsalya pension scheme in detail, covering its features, eligibility, contribution rules, investment choices, and the enrolment process. It also answers some common questions to give you a complete picture of how this scheme works.

What is the NPS Vatsalya Scheme?

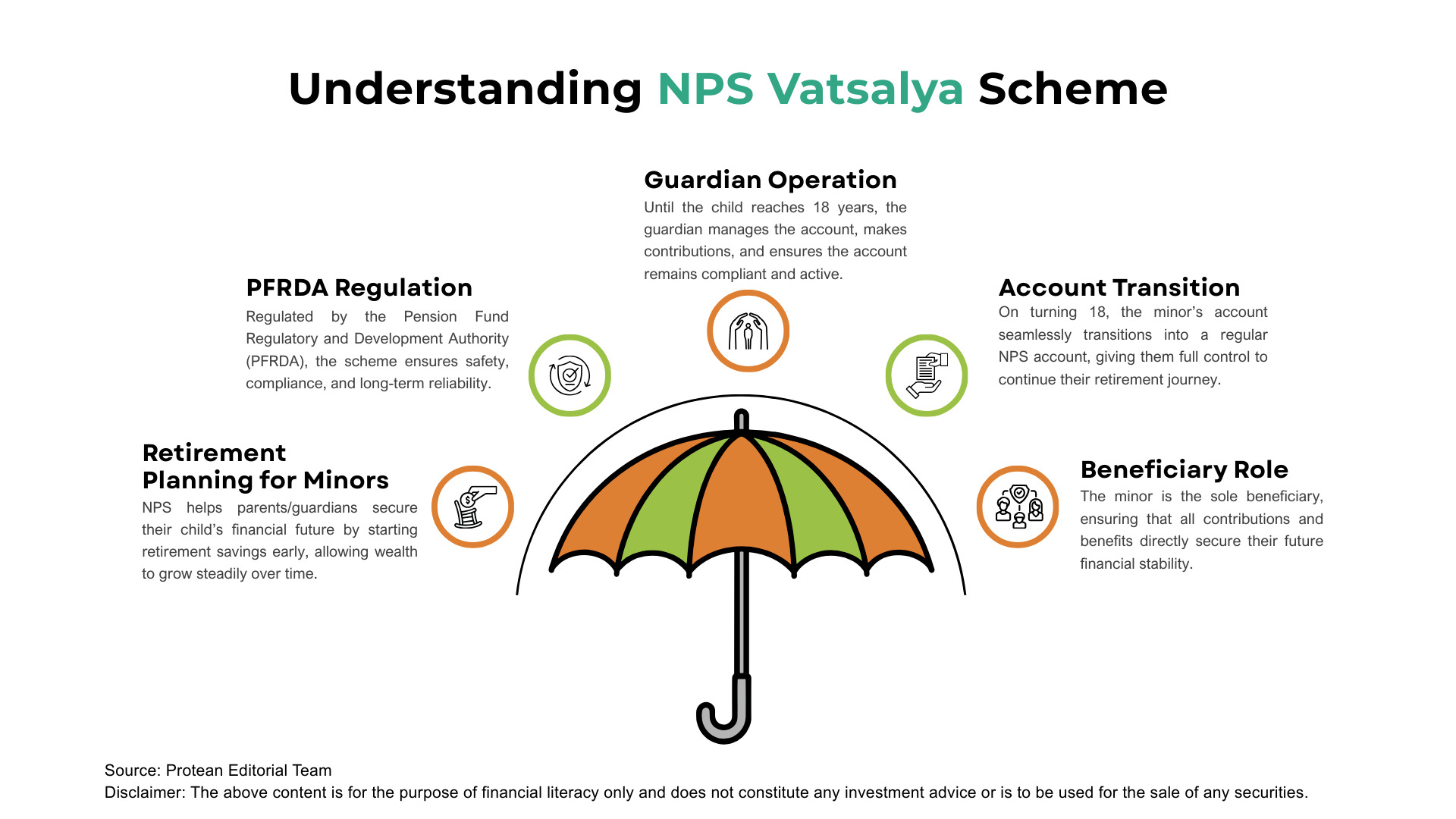

The NPS Vatsalya pension scheme is a saving-cum-pension plan regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Unlike traditional savings plans, it focuses on long-term retirement planning for minors.

Key points include:

- The account is opened in the name of a minor but operated by a guardian.

- The minor is the sole beneficiary of the account.

- Once the child reaches adulthood, the account seamlessly shifts into the regular NPS Tier-I framework.

This structure not only ensures financial security but also instils the importance of disciplined investing at a young age.

What are the Eligibility Criteria of NPS Vatsalya?

- All Indian citizens below the age of 18 are eligible.

- A guardian must manage the account until the child becomes an adult.

- On turning 18, the account automatically transitions into a full-fledged NPS account.

For example, if a guardian opens the account when a child is 10 years old, the guardian will manage it for 8 years. After that, the child continues as the primary holder under NPS Tier-I.

Where to Open an NPS Vatsalya Account

Guardians can open an NPS Vatsalya scheme account in two ways:

- Offline option: Visit a Point of Presence (POP) such as a major bank, Pan India Post offices, or a pension fund centre.

- Online option: Use the e-NPS platform for a quick and paperless process.

This flexibility ensures the scheme is accessible to both urban families who prefer online processes and rural families who may rely on physical branches.

Documents Required

To keep the process transparent, a list of documents is mandatory. Guardians must submit:

- KYC documents of guardian: Aadhaar, passport, voter ID, driving licence, NREGA card, or National Population Register details.

- PAN of the guardian or a Form 60 declaration.

- Date of birth proof of minor: Birth certificate, school leaving certificate, matriculation certificate, PAN, or passport.

- NRE/NRO bank account details: Required if the guardian is an NRI.

This comprehensive list ensures that the account is legally sound and verified.

| Also Read: Minor NPS Plan |

Contribution Structure

Contributions form the backbone of this scheme.

- Initial contribution: Minimum of ₹1,000 with no upper limit.

- Subsequent contributions: A minimum of ₹1,000 annually, again with no cap.

The absence of an upper limit makes the scheme flexible for different income groups. Parents can contribute small amounts regularly or make larger contributions depending on their financial planning goals.

Pension Fund Selection

The guardian can select any one of the pension funds registered with the PFRDA. This ensures that the investments are professionally managed under strict regulations.

For instance, a guardian who prefers steady growth can opt for a moderate fund, while another who is comfortable with higher risk may opt for an aggressive option.

Investment Choices

The NPS Vatsalya scheme details allow three investment approaches:

- Default Choice: Moderate Life Cycle Fund LC-50 with 50% equity exposure.

- Auto Choice: Guardian chooses from Aggressive LC-75 (75% equity), Moderate LC-50, or Conservative LC-25 (25% equity).

- Active Choice: Guardian directly allocates funds across:

- Equity (up to 75%)

- Corporate debt (up to 100%)

- Government securities (up to 100%)

- Alternate assets (up to 5%)

This flexibility ensures that families can align the account with their personal risk appetite and investment philosophy.

What Happens at Age 18?

When the child reaches 18 years:

- The account shifts seamlessly to NPS Tier-I (All Citizen model).

- Fresh KYC is required within three months.

- The child becomes the primary account holder.

This smooth transition ensures continuity of retirement savings without any interruptions.

Conclusion

The NPS Vatsalya scheme is more than just a pension account for minors. It is a structured financial instrument that combines savings, investment, and long-term planning in one package. By introducing children to money management early, guardians not only secure their future but also pass on the values of discipline and foresight.

For families seeking a flexible, transparent, and regulated scheme, the NPS Vatsalya pension scheme provides a reliable path to long-term financial well-being.

Frequently Asked Questions

Q1: What is the purpose of the NPS Vatsalya pension scheme?

It aims to provide minors with a retirement-oriented savings plan and teach them financial discipline.

Q2: Can NRIs open an NPS Vatsalya account for their children?

Yes, provided the guardian has an NRE or NRO bank account and submits the required documents.

Q3: What is the minimum contribution required?

A minimum of ₹1,000 for both opening and annual contributions. There is no maximum limit.

Q4: Who manages the funds under the scheme?

The investments are managed by pension funds registered with the PFRDA.

Q5: What happens to the account when the child turns 18?

The account shifts to NPS Tier-I, and fresh KYC is completed to make the child the direct