Tax planning is an essential part of personal finance management, and every taxpayer seeks ways to minimise their tax liability while securing their financial future. Among the many tax-saving investment options available, the National Pension System (NPS) stands out as a lucrative choice, offering tax benefits under the Income Tax Act. Let us explore how retail investors can maximise their tax savings through NPS and why it is an indispensable component of a well-rounded financial plan.

| NPS reached millions and millions more in 2024! Know about all NPS achievements in 2024 here. |

What is the National Pension System (NPS)?

The National Pension System (NPS) is a voluntary, long-term retirement savings scheme designed to provide financial security to individuals post-retirement. It is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) and is open to all Indian citizens between 18 and 70 years of age. NPS contributions are invested in a mix of equities, corporate bonds, and government securities, offering the potential for capital appreciation over the long term.

You can think of NPS as your personalised retirement nest egg. It can also be thought of as a bit like building your own pension, but with more flexibility. With NPS you might not just be throwing money into a black box. NPS can help you to choose how your funds are allocated and what will be their associated risk profile.

So, if you want to be aggressive and aim for higher returns? You can tilt your portfolio heavily towards equities.

Similarly, if you prefer a more conservative approach? You can stick with government bonds and corporate debt.

Finally, it is your call. And, it is not an ultimate choice to your portfolio, you can adjust it as you get closer to retirement.

Furthermore, NPS investing is not just restricted to saving. It is more about saving efficiently. The tax benefits can be a real draw. You can claim deductions on top of the 80C limit, which can seriously lighten your tax load. We will discuss this in more detail below in the blog.

And when you finally retire, a portion of your corpus can be withdrawn tax-free. It is designed to encourage you to build a substantial retirement fund, and it can be very optimally combined with tax saving during every financial year. Essentially, it can be about taking control of your golden years, rather than leaving it to chance or relying solely on traditional pensions and/or investment products.

| Did you know that you can secure your child’s retirement with NPS Vatsalya? Read about it here. |

Tax Benefits of NPS: A Deep Dive

NPS provides tax benefits across multiple sections of the Income Tax Act, making it one of the most tax-efficient investment options available to retail investors. Let’s examine these benefits in detail:

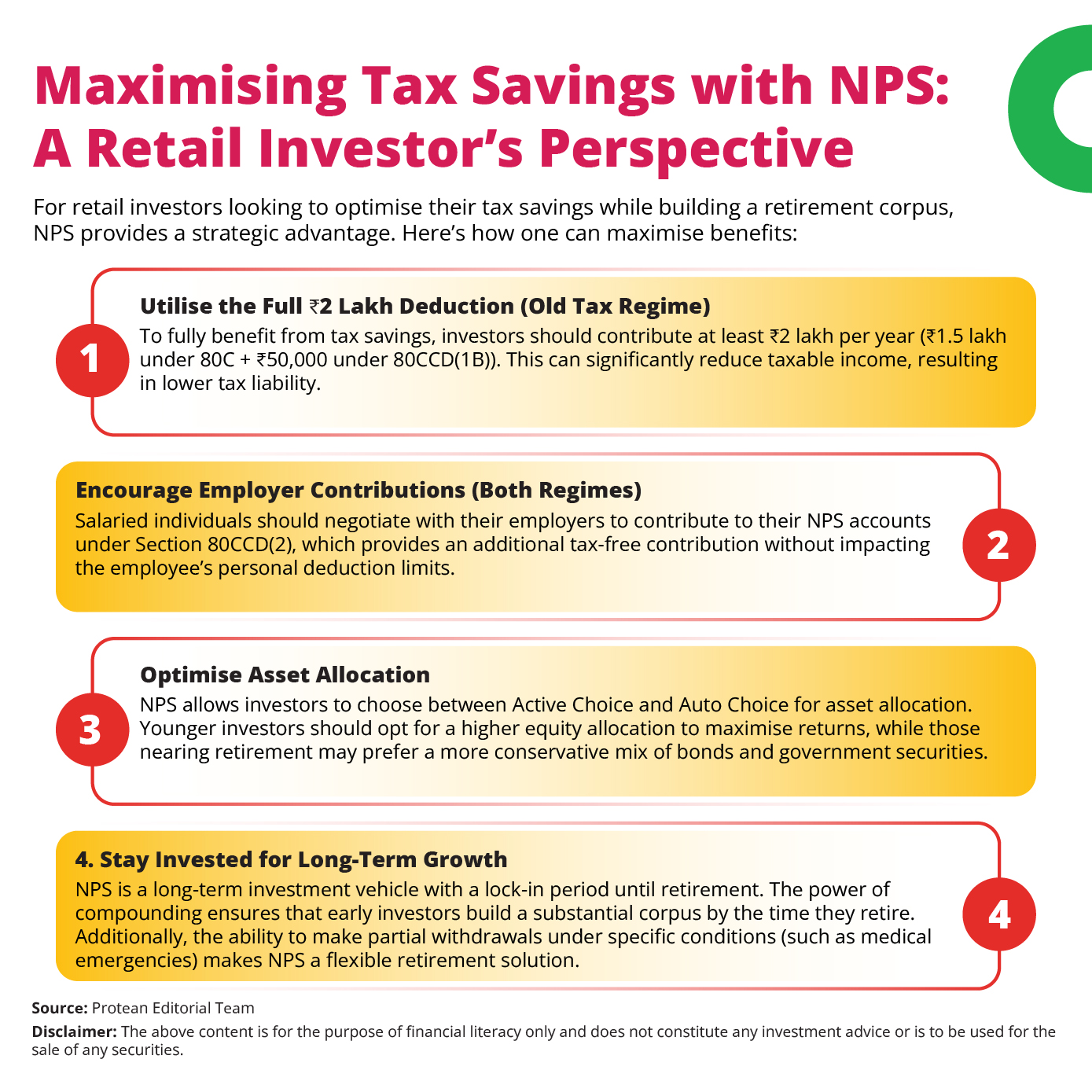

1. Tax Deduction Under Section 80CCD(1) (Old Tax Regime)

Under Section 80CCD(1), individual contributions to NPS qualify for a tax deduction of up to ₹1.5 lakh per financial year. This deduction falls within the overall limit of Section 80C, which includes other popular tax-saving instruments like Employees' Provident Fund (EPF), Public Provident Fund (PPF), and Life Insurance Premiums.

2. Additional Deduction Under Section 80CCD(1B) (Old Tax Regime)

To further incentivise NPS participation, the government provides an additional tax deduction of ₹50,000 per financial year under Section 80CCD(1B). This benefit is over and above the ₹1.5 lakh limit under Section 80C. By utilising this additional deduction, investors can reduce their taxable income by ₹2 lakh in total.

3. Employer Contribution Benefit Under Section 80CCD(2) (Old Tax Regime)

Salaried individuals whose employers contribute to their NPS accounts can avail of additional tax benefits under Section 80CCD(2). Employers can contribute up to 10% of the employee’s basic salary plus dearness allowance (DA), and this amount is deductible from the employee’s taxable income. Unlike the limits under Sections 80C and 80CCD(1B), this deduction has no absolute upper cap, making it especially beneficial for high-income earners.

| Become a corporate subscriber now! Learn about the documents and details here. |

4. Tax-Exempt Withdrawals Under the EEE Model (Both Regimes)

Although NPS was initially taxed under an Exempt-Exempt-Tax (EET) regime, Budget 2019 revised its tax structure, making it more attractive. Now, NPS withdrawals follow an Exempt-Exempt-Exempt (EEE) model, meaning:

- Up to 60% of the corpus can be withdrawn tax-free at retirement (age 60).

- The remaining 40% must be used to purchase an annuity, which provides a regular pension and is taxable as per the individual's income slab at the time of receipt.

| Learn about individual and company subscription documents and registration here. Register now! |

5. NPS Under the New Tax Regime

The new tax regime introduced in Budget 2020 provides lower tax rates but removes many exemptions and deductions, including those under Sections 80C, 80CCD(1), and 80CCD(1B). However, employer contributions under Section 80CCD(2) remain eligible for tax exemption, making NPS a viable option for salaried individuals even under the new tax regime.

Additionally, recently proposed changes to the new tax regime have introduced higher income thresholds for tax applicability, further influencing the choice between regimes for taxpayers.

| Can NPS Vatsalya be better than PPF or mutual funds? Find out here. |

| Do not wait until the last minute for NPS registration! Register now and start investing with NPS as you save taxes. |

Let us illustrate the tax savings potential of NPS with a few examples:

Case 1: Middle-Income Salaried Individual (Old Tax Regime)

- Annual Salary: ₹10 lakh

- NPS Contribution: ₹1.5 lakh (self) + ₹50,000 (additional under 80CCD(1B))

- Employer Contribution: ₹1 lakh (under 80CCD(2))

- Tax Calculation:

- ₹3,00,001 - ₹5,00,000 taxed at 5%

- ₹5,00,001 - ₹10,00,000 taxed at 10000+20%

- Effective tax savings from deductions are applied accordingly

Case 2: High-Income Professional (Old Tax Regime)

- Annual Salary: ₹30 lakh

- NPS Contribution: ₹1.5 lakh (self) + ₹50,000 (additional under 80CCD(1B))

- Employer Contribution: ₹3 lakh (under 80CCD(2))

- Tax Calculation:

- ₹3,00,001 - ₹5,00,000 taxed at 5%

- ₹5,00,001 - ₹10,00,000 taxed at 10000+20%

- ₹10,00,001 and above taxed at ₹ 1,12,500 + 30% above ₹ 10,00,000

- Tax savings from deductions are factored in for final liability

| Learned about the benefits? So, what are you waiting for? Open an NPS account with Protean now! |

Conclusion

The National Pension System is not just a retirement savings tool. It is more than that. It can be considered as a powerful instrument for tax saving. While deductions under Sections 80C and 80CCD(1B) apply only to the old tax regime, employer contributions under Section 80CCD(2) remain beneficial under both regimes. Additionally, with the revised income tax slabs under the new tax regime, taxpayers need to carefully evaluate whether NPS deductions provide them with maximum tax efficiency.

Retail investors can significantly lower their tax liability while securing their financial future by leveraging these benefits. You can start investing in NPS today and make the most of its tax-saving advantages while building a robust retirement corpus for a stress-free future!

- Story by Bruhadeeswaran R.

Bruhadeeswaran has 15+ years of experience as a content strategist, communication, and editorial professional. Currently, he is leading an innovative content development process, translating complex B2B products into engaging, user-friendly narratives.