Are you investing in mutual funds? It is great that you are already well-versed with the idea of systematic and disciplined investing. Did you know that you can complement your mutual fund investments with NPS scheme investing? Yes, NPS investing can add more power to your financial security goals.

As a mutual funds investor, you might understand:

- The power of compounding

- The importance of beating inflation

- The process of wealth creation

Both NPS and Mutual funds can help in wealth accumulation. You can add more power to your portfolio as you plan for retirement with NPS.

Adding an NPS account to your existing financial mix can upgrade your strategy. NPS introduces a layer of stability, tax efficiency, and disciplined saving to your portfolio.

You can integrate NPS scheme investing into your portfolio to transform a simple collection of investments into a comprehensive financial plan covering both growth today and security tomorrow.

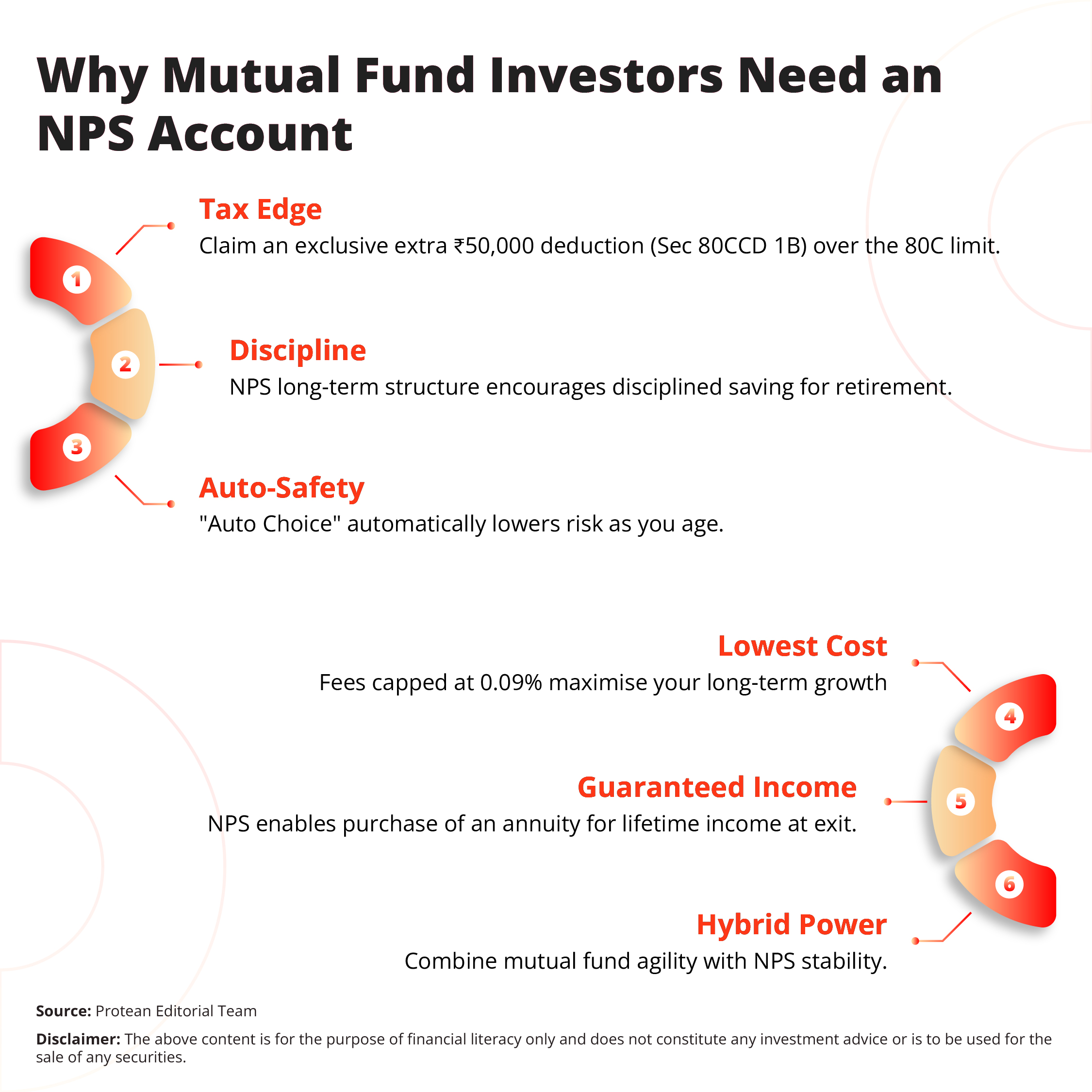

The Exclusive ₹50,000 Tax Edge You Cannot Get with Mutual Funds

ELSS mutual funds have a strict cap of ₹1.5 lakh per financial year. For most salaried professionals, this limit easily gets exhausted by mandatory EPF (Employee Provident Fund) contributions, life insurance premiums, and tuition fees.

But NPS scheme investing offers you unique tax benefits. Your NPS Tier 1 qualifies for an exclusive tax deduction under Section 80CCD(1B). With this specific provision you can claim an additional deduction of ₹50,000 over and above the ₹1.5 lakh limit of Section 80C. This NPS account benefit is unique among other tax saving instruments.

Here is an example.

If you fall into the 30% tax bracket, maximising this NPS scheme benefit can help you save you an additional ₹15,600 in taxes every financial year.

Therefore, these tax savings, over a span of around 20 years, when reinvested, can compound into a considerable amount. Here, your overall portfolio returns can be enhanced without any additional market risk.

Disciplined Retirement Architecture vs. The Temptation of Liquidity

One of the biggest strengths of mutual funds is liquidity. Here, you can sell your units and get money in your bank account within days. This temptation to liquidity might not be able to contain your financial impulses.

The NPS scheme can protect you from your own spending impulses. The Tier I NPS account has a mandatory lock-in period, up to 60 years of age.

This might seem restrictive, but it is an important long-term financial security feature. It enforces a discipline in terms of redemption. This lock-in can ensure that the money you set aside for your old age stays available for your old age. Thus, your retirement corpus stays untouched by mid-life consumption desires.

Furthermore, the NPS scheme offers an "Auto Choice" option. As you age, your risk appetite naturally decreases. In a mutual fund portfolio, you need to actively remember to sell equity funds and buy debt funds to reduce risk.

Failing to do this, can leave their corpus exposed to market crashes right before retirement. The NPS account can automate this process with the “Auto Choice” option. With this, the system automatically rebalances your portfolio every year. It effectively reduces equity exposure and increases debt allocation as you get older.

The Cost-Efficiency Factor

Management costs can heavily impact your mutual fund returns. In mutual funds, actively managed equity funds can charge TER (Total Expense Ratio) between 0.5% and 1.5% annually. Even passive index funds have charges from 0.10% to 0.50%.

The NPS scheme operates with one of the lowest cost structures in the global pension market. The fund management charges for an NPS account is limited to 0.09%. Because retirement investing occurs 20 years to 30 years, this cost efficiency can result in a much higher net corpus for the subscriber.

Thus, more of your money can remain invested and grow over time. Over a longer horizon, this differential can add lakhs to your final maturity value.

Structuring Your Post-Retirement Income

Managing a lump sum to last for 30 years of retirement can be complex. You might face the risk of "longevity," where you might outlive your savings, or poor withdrawal planning. You might also risk spending too much too soon.

The NPS scheme can solve this distribution challenge structurally with its revised Corporate Sector (CS) and MSF All Citizens model. In NPS, now you need to use at least 20% of your maturity corpus to purchase an annuity plan.

This annuity provides a regular, guaranteed monthly pension for the rest of your life. Mutual funds can provide the capital, but the NPS account can ensure the continuous cash flow.

Thus, you do not have to worry about uncertain income in your sunset years. You can thus get the best of both worlds. You get a considerable lump sum to enjoy (80% of the corpus is tax-free) and a steady, reliable pension to cover your basic living expenses.

Conclusion - The Hybrid Approach to Wealth

Rather than debating "Mutual Funds vs. NPS," investors can use both investments to complement each other. Investing in mutual funds and NPS together can help you form a strong retirement corpus while achieving short, medium and long-term financial goals.

Mutual funds can add agility, liquidity, and aggressive growth potential to your portfolio. The NPS scheme can complement this by providing the stability, tax efficiency, and disciplined "lock-in" required for a secure and stress-free retirement.

Investors can maintain both a mutual fund portfolio and an NPS account. Thus, they ensure that their financial life has both a "growth engine" and a "safety anchor."

This hybrid approach can optimise your wealth, lower your tax liability, and provide your financially secure retirement. Log in to the Protean eGov Technologies portal now and open your NPS account.