Seedha: Guess what? I got a bonus! Thinking of putting it in a Fixed Deposit.

Sayaani: Fixed Deposit? Really? Are you also planning to store some of it in a piggy bank, or maybe under your mattress for good luck?

Seedha: Umm... no? But what's wrong with FD?

Sayaani: Nothing wrong, just old school! Have you heard about NPS (National Pension System)? It’s like a surprise combo deal—piggy bank, discount shopping, and a secret bargain hack, all in one!

Seedha: Whoa, all three in one? Now you’re speaking my language!

Sayaani: Exactly! If you don’t believe me, you can listen to this.

For us millennials, thinking about long-term financial security is important—yes, even more important than that latest phone upgrade you’ve been eyeing. NPS is like a financial ‘sixer’—it helps you save for retirement (Tier I), offers flexibility for other goals (Tier II), and gives you tax benefits. Plus, it lets you invest smartly, even grabbing discounts during market dips!

Seedha: So, you’re saying NPS could make me a Crorepati?

Sayaani: If you invest regularly, you should read the protean blog and get answers to your common questions on NPS.

And when you start investing, even your childhood piggy bank would be jealous. Speaking of which, do you remember using one?

Seedha: Of course! I had a cute one shaped like a tiger.

Sayaani: Nice! And you’d want your kids to have one too, right?

Seedha: Obviously!

Sayaani: Well, how about an upgrade with Portfolio Diversification?

You may Enter NPS Vatsalya! Just like you give a piggy bank to your child, you can set up a virtual one for their retirement, and while you’re at it, keep growing your own savings with NPS.

With products like these, traditionally viewed as a government-backed retirement scheme, NPS has evolved into a sophisticated investment vehicle with a focus on long-term wealth creation.

Thanks to its product evolution and diversity, it is no longer just about retirement. NPS can be strategically integrated into your overall financial plan.

Sounds interesting? Start your financial independence journey with NPS now. |

Here is how NPS can serve as a smarter and comprehensive financial planning tool:

Gone are the days of rigid investment options. Today, NPS offers a degree of flexibility, allowing you to choose between different investment options, such as equity, corporate bonds, and government securities, based on your risk appetite and investment horizon. This customisation allows you to tailor your NPS investments to align with your unique financial goals and risk tolerance. With this, I must say that NPS can be your financial ‘game-changer’.

NPS encourages diversification by mandating a minimum allocation to equity investments, especially in the early stages. This exposure to equities, historically known for their long-term growth potential, can significantly boost your retirement corpus over time.

Seedha: It sounds amazing! Can you tell me if it has any tax benefits?

Tax Benefits of NPS

Sayaani: Okay, quick quiz—how much tax can you save with NPS?

Seedha: Uhh… ₹10,000?

Sayani: Nope! It’s way more. An NPS calculator can help you efficiently calculate your NPS tax savings. Click here to learn more.

For employees the NPS tax saving works in the following manner:

Self-Contributions - under old tax regime

Deduction under Section 80C: Employees can claim a tax deduction of up to 10% of their salary (Basic + Dearness Allowance) on their own contributions to NPS under Section 80CCD(1) of the Income Tax Act. This deduction is within the overall limit of ₹1.50 lakh under Section 80CCE.

Additional Deduction: An additional deduction of up to ₹50,000 is available under Section 80CCD(1B) above the overall limit of ₹1.50 lakh under Section 80CCE.

Contributions by Employers

Employers can claim a tax deduction of up to 10% of the employee's salary (Basic + Dearness Allowance) on their contributions to the employee's NPS account under Section 80CCD(2). This deduction is available over and above the ₹1.50 lakh limit under Section 80CCE. For Central Government employees, the deduction limit is 14%.

For self-employed individuals NPS tax saving works in the following manner:

Self-Contributions

Deduction under Section 80C

Self-employed individuals can claim a tax deduction of up to 20% of their gross income on their own contributions to NPS under Section 80CCD(1) within the overall limit of ₹1.50 lakh under Section 80CCE.

Additional Deduction

An additional deduction of up to ₹50,000 is available under Section 80CCD(1B) above the overall limit of ₹1.50 lakh under Section 80CCE.

| You can invest in NPS, both Online and Offline. Check the NPS investing steps and process here. |

Seedha: Hold on—so I can save taxes, invest, and retire rich? That’s a triple win!

Sayaani: Exactly!

Seedha: Do we have any tax-benefit on withdrawal?

Sayaani: Yes, let me explain that to you.

And withdrawals have tax benefits too. You get tax-free partial withdrawals, tax-exempt annuity purchases, and even tax exemptions on a lump sum withdrawal at retirement. Basically, NPS is the gift that keeps on giving! Let me elaborate on this:

Partial Withdrawal

Tax exemption is available on withdrawals for up to 25% of the self-contribution from the NPS account under certain conditions specified by the Pension Fund Regulatory and Development Authority (PFRDA) under Section 10(12B) of the Income Tax Act.

Annuity Purchase

Tax exemption is available on the purchase of an annuity upon reaching the age of 60 or superannuation under Section 80CCD(5). However, the subsequent income received from the annuity is taxable under Section 80CCD(3).

Lump Sum Withdrawal

Tax exemption is available on the lump sum withdrawal of 60% of the accumulated pension wealth upon attaining the age of 60 or superannuation under Section 10(12A) of the Income Tax Act.

Tax benefits for corporates and employers work in the following manner:

Employer Contributions

Corporates or employers are eligible for a tax deduction on the amount contributed as their share towards the NPS accounts of their employees. This deduction is allowed up to 10% of the employee's salary (Basic + Dearness Allowance) as a 'Business Expense' from the Profit and Loss Account under Section 36(1)(iv)(a) of the Income Tax Act.

Seedha: Sounds like a dream investment! But is it flexible? You know how I am—I change plans faster than my weekend movie picks.

Sayaani: Haha, no worries! NPS is super flexible. Let me elaborate on this. Let us lean more on NPS’s high degree of flexibility:

· Online Access and Easy Contributions: You can easily manage your NPS account online through the official NPS website or through designated points of presence (POPs).

· Portability Across Jobs: Your NPS account remains with you even if you change jobs. This ensures continuity in your retirement savings journey, regardless of your employment status.

· Early Withdrawal Options: While early withdrawals are generally discouraged, limited withdrawals are allowed in certain circumstances, such as for higher education or marriage of children.

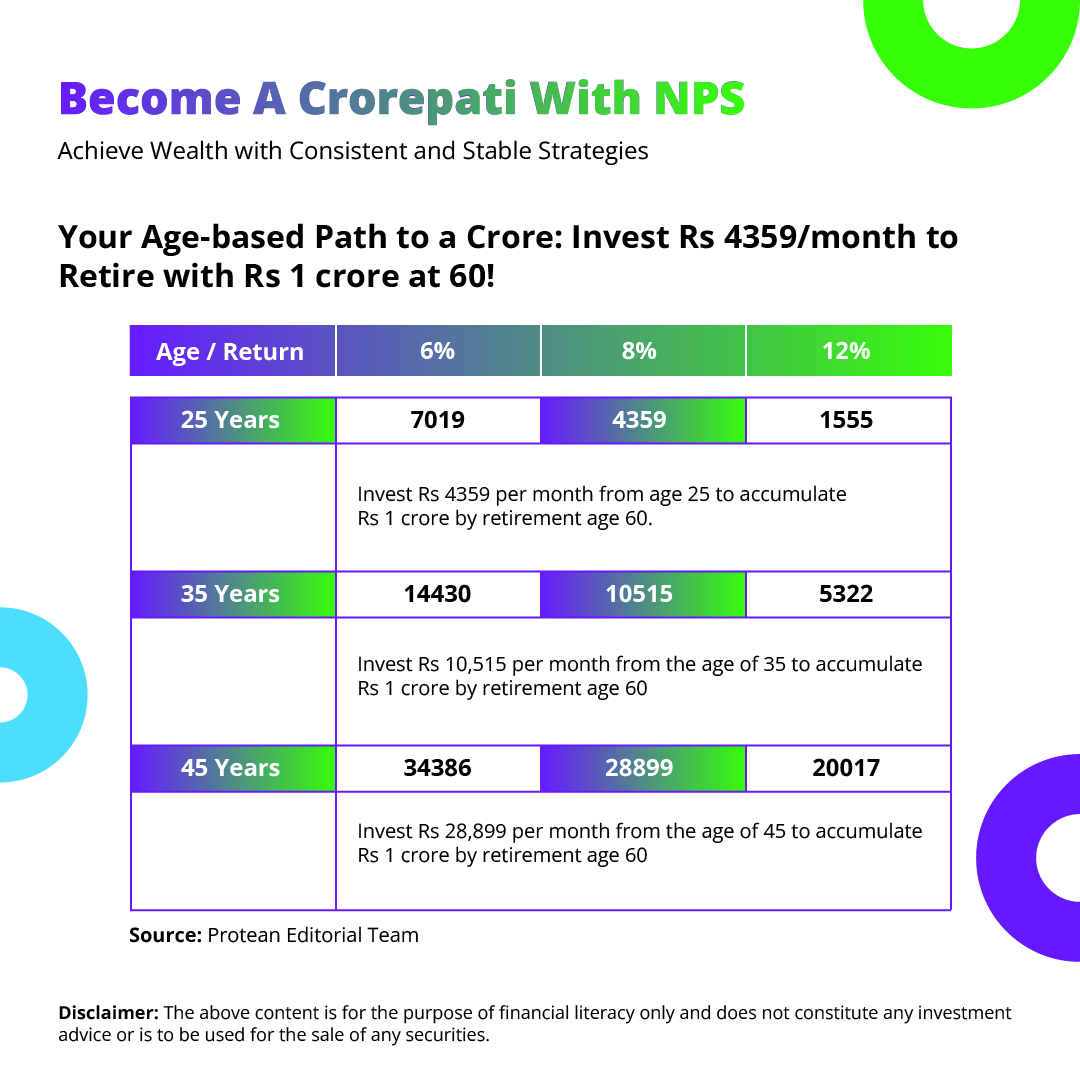

Seedha: That’s a relief! But tell me, how much can I actually make with NPS?

Sayaani: With the Power of Compounding. Here is a hypothetical example to explain this:

Suppose you are a 30-year-old individual who starts investing ₹10,000 per month in NPS. Assuming an average annual return of 10% and considering the power of compounding, you could accumulate a substantial retirement corpus, maybe in crores, by the time you reach retirement age.

Look at this image below to learn more on becoming a ‘Crorepati’ with NPS investing!

This highlights the long-term benefits of consistent contributions to NPS. Early investments allow your money to grow exponentially over time, leveraging the power of compounding.

Don’t just save taxes. Amplify your retirement planning with NPS Tier II investing. Subscribe and make your contribution now!

Seedha: Hold on—did you just say crores?!

Sayaani: Yep! That’s the Power of Compounding. Small, regular investments now can grow into a massive fund later.

Seedha: Okay, I’m sold. How do I start?

Sayaani: If you find NPS investing better, you may read this to learn how to register and make your contribution now!

And don’t forget—if you want to save taxes before the financial year ends, make your Tier I contribution now.

Seedha: Done! Now, where’s my Crorepati badge?

Sayaani: Haha, patience, my friend. Just stay consistent, and soon enough, you’ll be thanking me!

A Snapshot of NPS Investing Benefits

Here are the major benefits of NPS as discussed through the above points:

NPS Tax Benefits

As discussed earlier, NPS offers significant tax benefits under 80CCD (1B) of the Income Tax Act, allowing you to reduce your taxable income and save on taxes. This is over and above the deduction of Rs. 1.5 lakh available under section 80C of Income Tax Act.

- Flexibility: NPS can offer flexibility in terms of investment options, contribution amounts, and withdrawal options. This can help you to customise your retirement savings plan to your specific needs and risk tolerance.

- Power of compounding: The power of compounding is a key driver of long-term wealth creation in NPS. By consistently investing over time, your returns can grow exponentially, leading to significant wealth accumulation.

- Portfolio diversification within NPS: NPS investing can offer a diversified investment portfolio, including equity, corporate bonds, and government securities. This diversification helps to mitigate investment risks and enhance the potential for long-term returns.

| Hurry! Don’t miss out on saving taxes for the Financial Year. Make your Tier I contribution now! |

Conclusion

NPS is not simply a retirement savings scheme, but a ‘Smarter Way To Save’. It is much more than that, a strategic investment tool that can considerably impact your financial future. Therefore, you can build a strong financial foundation for a comfortable and secure retirement, just as you leverage the NPS tax benefits, flexibility, and the power of compounding.

Story by Bruhadeeswaran R.

Bruhadeeswaran has 15+ years of experience as a content strategist, communication, and editorial professional. Currently, he is leading an innovative content development process, translating complex B2B products into engaging, user-friendly narratives.