As you navigate the rapidly evolving digital finance landscape in India, verifying customer bank account details accurately becomes central to safeguarding transactions and ensuring regulatory compliance. One method you may have increasingly come across is the Penny Drop Verification. In this process, a nominal amount of ₹1 is sent to a customer’s bank account, to help confirm whether the beneficiary name matches the bank records.

With digital onboarding, payouts, and automated financial workflows becoming the norm, you may wonder whether penny drop is optional or a mandatory requirement. This article helps you understand the regulatory position, the purpose behind its adoption, and how you can integrate penny drop effectively into your systems.

What is Penny Drop Verification & Its Regulatory Landscape?

With Penny Drop Verification, you can authenticate a customer’s bank account by initiating a tiny transfer into it (usually ₹1). When the amount transfer goes through, the bank shares the beneficiary’s name from its records, and you can compare it against the name shared by the customer.

If the match is successful, you will know that the account is active and ownership is validated. However, transfer failure indicates that the account is likely incorrect, dormant, frozen, or affected by other issues.

Penny drop is not mandated from the regulatory standpoint across the entire financial sector. However, it’s made compulsory in some segments.

For example, under the National Pension System (NPS), the Pension Fund Regulatory and Development Authority (PFRDA) penny drop verification is required for exit and withdrawal processing and bank account change requests.

So, if the penny drop fails or the name does not match, you are not permitted to process such requests.

However, in several other segments, penny drop is not mandatory, but it is highly recommended as a part of good KYC and risk-management practices. Therefore, the penny drop mandate depends on the industry you operate in and the applicable regulatory framework.

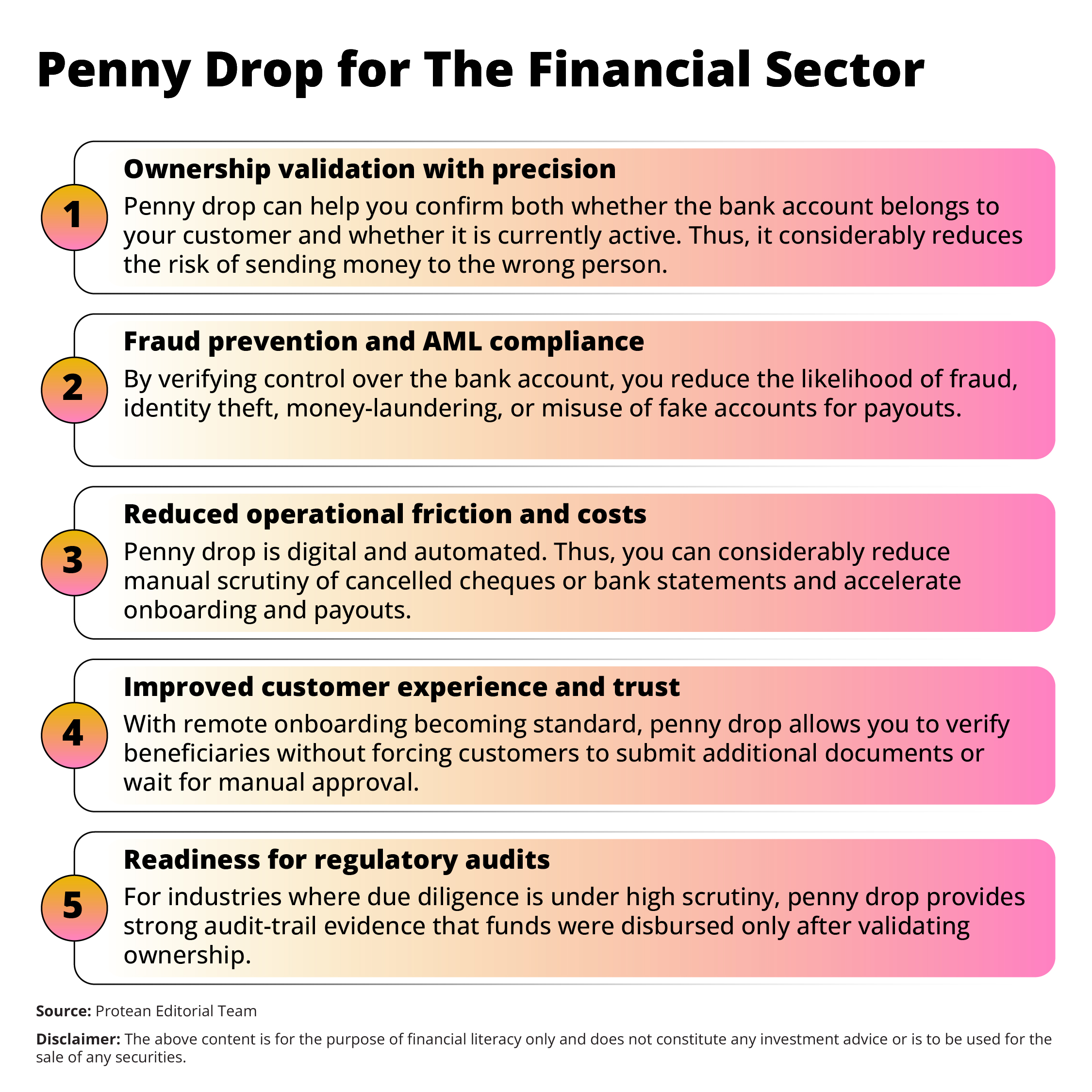

Why the Financial Sector Adopted Penny Drop

There are strong reasons you might rely on penny drop verification, even when it is not mandatory. This applies to various sectors and businesses (whether you are running a fintech, mutual fund distribution platform, payment gateway, insurance business, NBFC, or gig-worker payout platform).

Simply put, penny drop has become a preferred practice because it gives you accuracy, security, and compliance without friction.

Integrating Penny Drop Verification into Your System

You can implement penny drop verification by using this simple flow.

- Collect customer bank details - You can enter account number, IFSC, and the declared account holder name.

- Trigger a penny drop API call - Send a nominal amount (preferably ₹1 ) through your verification service provider.

- Retrieve and analyse the bank response - When the transfer succeeds, the bank returns the account holder’s name. You can compare it with the user-submitted name to check ownership.

- Configure automated handling of failures - If the transfer fails or the name does not match, prompt the user to correct bank details or provide alternate proof.

- Store verification proof securely - You can keep the verification response as compliance evidence for future audits or regulatory inspections.

If your organisation is already using Aadhaar-based or PAN-based digital KYC solutions (for example, through providers like Protean eGov Technologies Ltd.), penny drop can complement those solutions and create a stronger, multi-layer identity-and-ownership verification system.

Conclusion

Penny Drop Verification has evolved into a widely used bank account validation and due-diligence tool within India’s financial ecosystem. While it is not universally mandated for every business, regulators such as PFRDA have made it compulsory for major processes like NPS withdrawals and bank account change requests.

In many sectors where it is not mandated, penny drop is widely adopted as a standard practice because of the additional security and reliability it offers.

If you are responsible for managing disbursements, customer onboarding, or KYC compliance, adopting penny drop can help you prevent financial errors, curb fraud, and foster trust.

Thus, offering a penny drop facility reflects a stronger approach to verification and can be viewed as a marker of more responsible financial operations.

Frequently Asked Questions

Q1: Is the amount used in penny drop verification refundable?

Yes. The ₹1/- transferred during the verification process is only a test amount and is usually reversed automatically, so your customer does not lose any money.

Q2: How is penny drop different from simple account number validation?

Simple validation checks whether the account number and IFSC exist, whereas penny drop additionally verifies ownership and confirms that the account is active, preventing payouts to incorrect or fraudulent accounts.

Q3: Which financial institutions are required to use penny drop?

Penny drop is mandatory for certain processes such as withdrawals under NPS regulations enforced by PFRDA. Other institutions, including banks, NBFCs, insurers, brokers, fintechs, and payout platforms commonly use it voluntarily as a risk-mitigation and trust-building practice.

Q4: Is penny drop relevant for international bank accounts?

No. Penny drop works only within India’s domestic banking network. For foreign accounts, you must rely on alternative mechanisms such as SWIFT-based verification or document-based account confirmation.