Can a single NPS contribution transform your retirement planning?

Yes, NPS investment this Diwali, can be a strategic step toward your future financial security..

As Diwali draws near, many Indians plan festive purchases, gifts, and rituals. Yet, Diwali can also mark a turning point in your financial life if you make a deliberate move toward retirement security. A National Pension System (NPS) contribution made during the festival season can serve as a motivating point to secure lasting financial benefits. In this article, we explain how a one-time Diwali NPS contribution can become a keystone in your retirement planning, while also touching on recent policy shifts and regulatory updates in the NPS landscape.

Why Diwali Is the Perfect Time for an NPS Contribution

Diwali is more than a festival of lights; it is often a time of optimism, renewal, and intention setting. Many people plan new beginnings during this period, which makes it psychologically apt to commit to long-term financial goals.

From a practical angle, end-of-year tax planning is a preferred horizon. However, by making an NPS contribution around Diwali, you can get an early start on your annual savings target and potentially get the benefit of compounding.

In addition, many employers and financial services see higher activity in quarter ends and fiscal year ends, so planning early gives you breathing room.

Moreover, with recent changes in NPS, such as the introduction of a Multiple Scheme Framework (MSF) for non-government subscribers effective October 1, 2025, the time is appropriate to check your NPS strategy.

The Power of One-Time Investment

A single lump-sum investment in NPS, especially early in your investment horizon, can have outsized impact. Through the forces of compounding, even a modest amount can grow significantly over decades, especially when equity and debt allocations perform well. Since NPS is designed as a long-term instrument, timing matters less than consistency and longevity.

In the NPS architecture, your contributions get invested in a mixture of assets such as government securities, corporate bonds, and equities (depending on your chosen allocation). With the recent liberalisation allowing up to 100% equity allocation under the MSF for non-government subscribers, the potential upside has grown further, albeit with higher volatility risk.

Thus, your Diwali contribution may benefit more if markets recover in ensuing years, and your corpus can compound with reinvestment of returns.

Further, since NPS is portable across jobs and locations, your contribution stays in play even if your employment situation changes.

Tax Benefits of Your NPS Contribution

Tax benefits remain one of the strongest draws of NPS. Under the Income Tax Act, contributions to NPS Tier I accounts are eligible for deductions under:

- Section 80C, within the overall Rs.1,50,000 limit

- Section 80CCD(1B), an exclusive extra deduction of up to Rs. 50,000 over and above 80C

This gives an effective total deduction of up to Rs.2,00,000 in a fiscal year.

Additionally, at withdrawal, up to 60% of the accumulated corpus can be withdrawn as a lump-sum tax-free, the amount used to purchase an annuity is exempt from tax at the time of annuity purchase, though annuity payouts are taxable. Over time, these benefits can compound to meaningfully reduce your tax burden.

However, keep in mind that changes in tax rules could happen. Also, NPS now allows new options (like MSF) that may affect the tax treatment of switches or partial withdrawals, though core deduction benefits remain intact under current regulation.

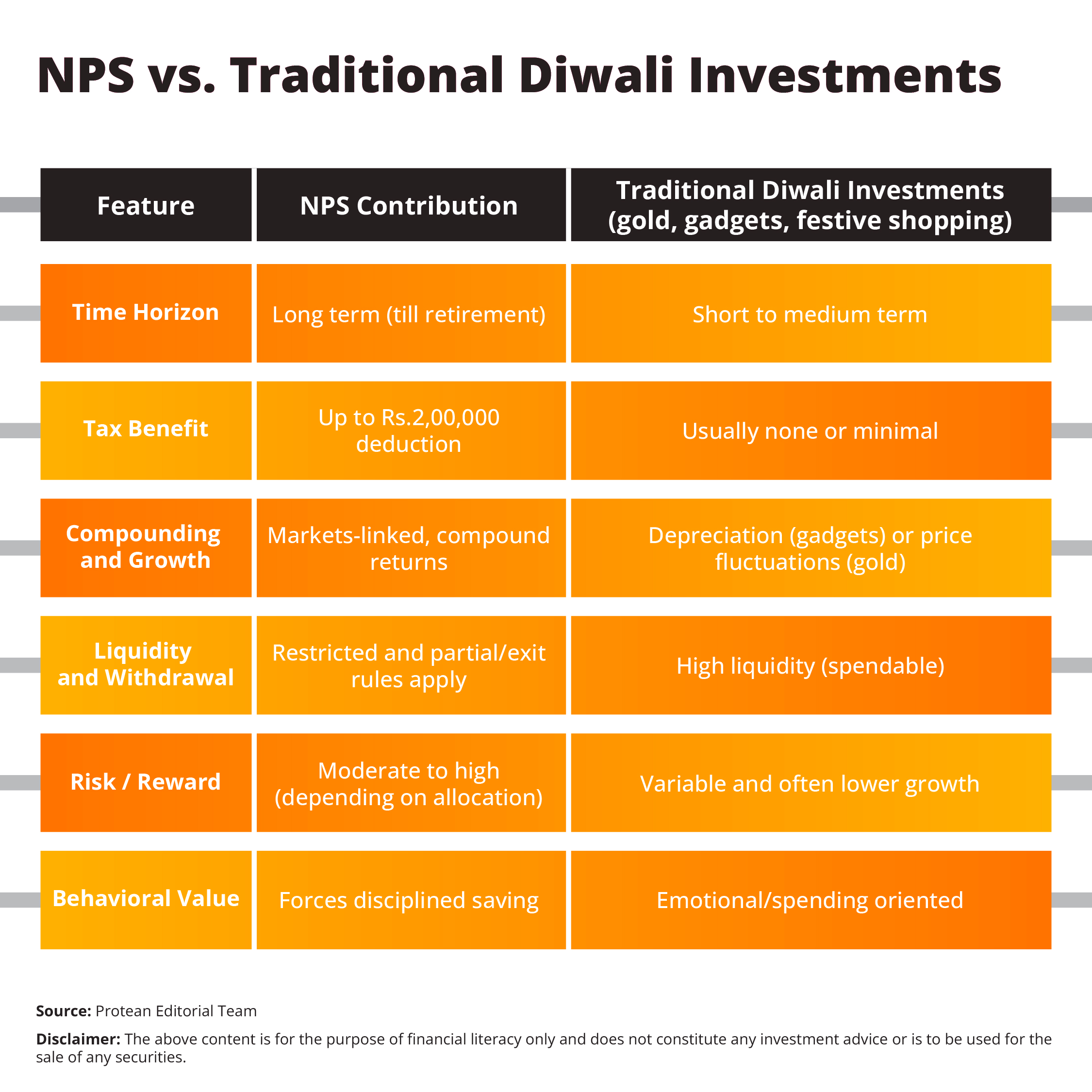

NPS vs. Traditional Diwali Investments

Below is a comparative infographics-style summary (you may convert this into a visual later):

You shift the balance from ephemeral consumption toward long-term wealth creation by placing at least part of your Diwali outlay into NPS.

Conclusion

A single NPS contribution made during Diwali is more than a symbolic act, it is a strategic decision. With compounding, tax savings, and new flexibility under MSF, your Diwali contribution can brighten your retirement prospects. As change sweeps through India’s pension policies from extension of UPS deadlines to new equity norms, staying proactive and informed is key.

So, let us use the festive momentum to secure your financial future.

Frequently Asked Questions

Q1: Can I make only one NPS contribution and still benefit?

Yes. Even one meaningful contribution can harness compounding over years. But combining it with regular contributions strengthens your retirement corpus.

Q2: What if stocks perform poorly after I invest?

Equity exposure brings risk, which is why diversification matters. With MSF, you may balance equity and debt funds to moderate volatility. Over long periods, markets often recover.

Q3: Who regulates NPS and ensures transparency?

NPS is regulated by PFRDA, which defines investment norms, operational guidelines, and safeguards subscriber rights.

Q4: Can non-government participants use the new 100% equity option?

Yes. From October 1, 2025, non-government NPS subscribers can allocate up to 100% into equities under a single scheme, under the MSF.

Q5: How does NPS differ from UPS (Unified Pension Scheme)?

UPS is a new option for central government employees offering assured pension features, unlike the market-linked NPS. Eligible employees were given time (recently extended) to opt into UPS or stay in NPS.