The Indian economy has transformed considerably over the past decade. Identity verification is no longer just a regulatory barrier for individuals.

Forward-thinking institutions now perceive verification as a symbol of trust and competitive advantage. The Central KYC (CKYC) registry operates as a centralised repository. It is managed by the Central Registry of Securitisation Asset Reconstruction and Security Interest of India (CERSAI).

Traditional, fragmented KYC methods might result in high customer drop-off rates and excessive operational costs. Such outdated systems can frustrate users and delay financial investments from growing.

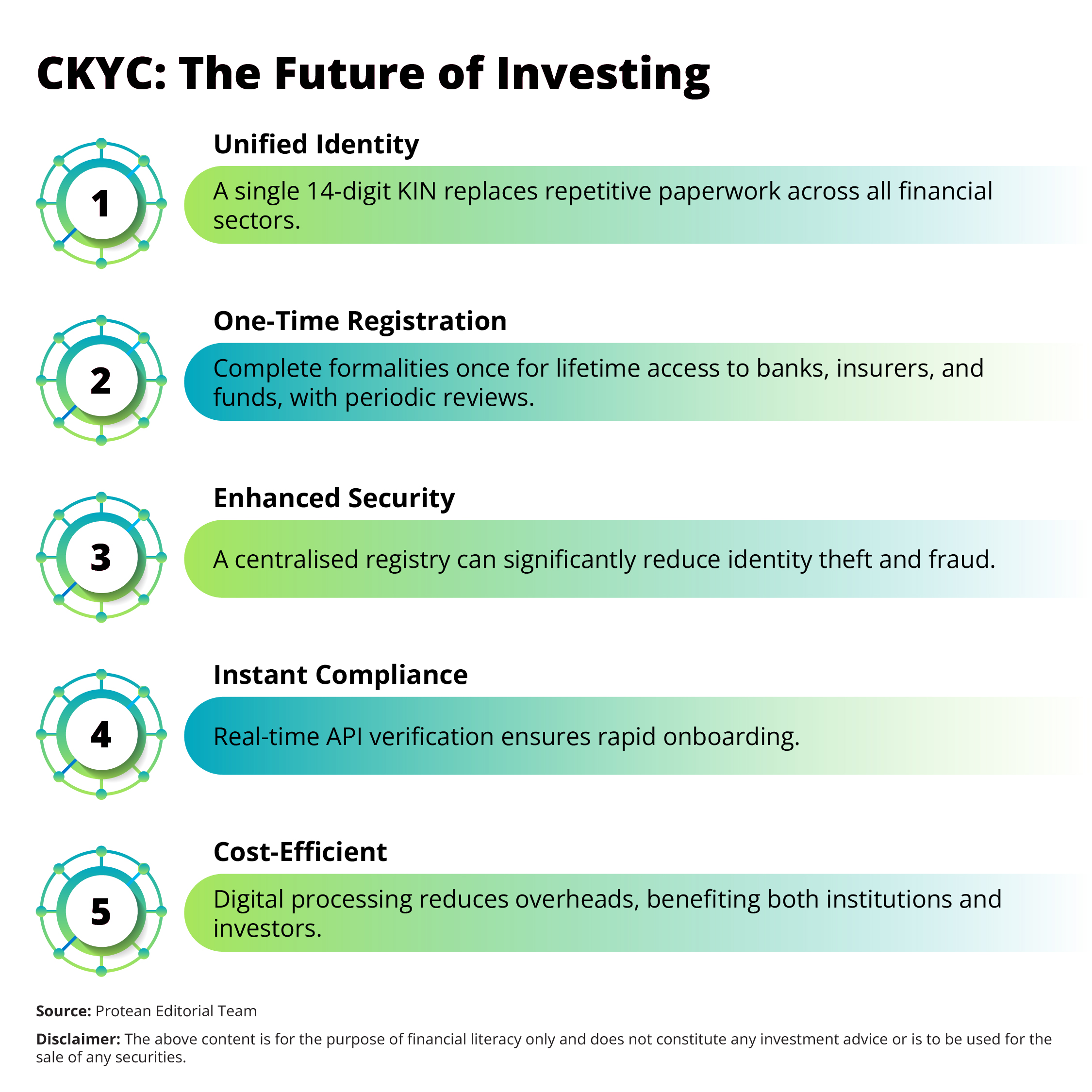

Today, CKYC online has developed a unified platform. Here, an investor can complete all the formalities once. They do not have to repeat the KYC activity separately for various entities.

This centralised approach has made CKYC an important requirement for institutions aiming to capture the next wave of digital-savvy investors.

Streamlining the Onboarding Lifecycle

Suppose an individual has registered with the CKYC registry for the first time. The reporting entity would upload the verified data to the central server.

Next, CERSAI would assign a unique 14-digit KYC Identification Number (KIN) to the user. This number is a permanent digital identity for the entire financial sector.

Now, with CKYC, future interactions with other banks, mutual fund houses, or insurance companies become simple. Here, the user can simply quote the KIN instead of physical document submission.

The process of CKYC online registration can reduce the need for repeated paper-based checks. Generally, this efficiency can also reduce the hassles associated with the onboarding lifecycle.

Modern financial platforms integrate CKYC online APIs to fetch pre-verified data in real-time. With this capability businesses can move from account opening to transaction readiness within a few minutes.

Investors would also appreciate the lack of paperwork. Thus, the CKYC online process can directly lead to higher conversion rates for the service provider. With a smooth digital experience, users can remain engaged with their chosen financial investments, reducing the drop-off rates.

Strengthening Institutional Compliance and Risk Mitigation

For compliance management it is important to have a strong attention to detail and standardised data protocols. The CKYC framework can ensure that every record in the central registry is meeting a uniform, high-quality standard for data accuracy.

Every reporting entity can verify the documents before the initial upload. This creates a foundation of trust for all other institutions.

CKYC online systems can also help in the mitigation of risks associated with identity theft and forged documents. With centralisation, the registry can flag and prevent fraudulent activities across multiple platforms. For example, it can be much harder for a single individual to use different identities to secure multiple loans on the same asset.

Regulatory bodies such as the RBI, SEBI, IRDAI, and PFRDA have mandated the use of centralised records for maintaining a clear audit trail. This standardisation also aligns with Anti-Money Laundering (AML) and Customer Due Diligence (CDD) requirements.

Many institutions can utilise Aadhaar authorisation to further strengthen the identity verification layer during the initial setup. It is an advanced method to confirm the physical existence and biometric or OTP-based consent of the user.

Protean eGov Technologies can provide SMART systems that use machine learning and image recognition to synchronise these records with CERSAI effectively.

These intelligent engines can minimise manual intervention and reduce the probability of human error in high-volume processing.

Stronger compliance can result in a more stable financial ecosystem for all participants.

Cost-Efficiency for Businesses

Operational expenses can consume a large portion of a company's budget by handling physical documentation. Traditional KYC requires heavy investments in manual data entry, physical storage, and courier services for document movement.

Adopting a CKYC online mechanism can help businesses considerably lower these overhead costs. Institutions can pay for API-based search and download functions rather than maintaining an army of verification agents.

Protean's automated bulk upload solutions further optimise the frequency of database queries. This results in tangible financial savings.

The digital nature of the registry can also remove the risks of document loss or damage over time. With savings from reduced paperwork, companies can reinvest capital into core business activities or customer-centric innovations.

Moreover, CKYC online can also lead to the mutualisation of costs across the entire financial sector. With this system, companies can have a lean and cost-effective retrieval process. Efficiency in data management can translate directly to a healthier bottom line for any company facilitating financial investments.

Future-Proofing Financial Portfolios in 2026

In 2026, there is an increased demand for instant access to diversified financial investments. Now, investors can hold portfolios spanning across various asset classes like equity, debt, insurance, and pension funds.

CKYC acts as an important bridge between these diverse sectors. With a single KYC record, an individual can switch between different financial products without the burden of fresh documentation.

These developments aim to keep the verification process secure against growing cyber threats. Businesses adopting CKYC online today can position themselves at the forefront of this digital evolution.

Therefore, the adoption of centralised records becomes a strategic necessity for any institution that handles financial investments.

The system creates a more inclusive environment where even residents in remote areas access formal financial services with ease.

Conclusion

The strategic value of a centralised KYC system cannot be overstated in today's fast-paced market.

The CKYC online process represents a shift towards a more transparent, efficient, and secure financial environment. It can empower both the investor and the institution by removing redundant steps and lowering operational barriers.

The support of agencies like Protean can make financial investments safer for everyone involved. Individuals completing their CKYC registration can gain swift access to a world of financial opportunities.

Frequently Asked Questions (FAQs)

Q1: What exactly is the 14-digit KIN in CKYC?

The KIN or KYC Identification Number is a unique 14-digit identifier assigned to a user after successful registration. With this, any financial institution can pull your verified data from the CERSAI database.

Q2: Is CKYC online mandatory for all new financial investments?

Yes. Regulators like RBI, SEBI, IRDAI, and PFRDA mandate that reporting entities (REs) upload KYC data of new customers to the CKYC registry for specified financial products. This is to ensure a uniform standard across the sector.

Q3: How does Aadhaar authorisation help in the CKYC process?

Aadhaar authorisation is a secure method for eKYC during the initial registration phase. It can help the reporting entity verify the identity of the person in real-time through OTP or biometrics.

Q4: Can an individual update their details in the CKYC registry?

An individual can update their information through any CKYC-compliant financial institution. Once updated, the changes reflect across all institutions linked to that KIN.