Budget 2025 and NPS announcements can be better understood with the help of this anecdote between Ajit and Kiran.

Ajit and Kiran, a young couple from Mumbai, were busy balancing their careers and raising their newborn son, Nihaal. While planning their financial future, they attended a seminar on retirement planning, where they learnt about the National Pension System (NPS) and its newly introduced child-focused variant, NPS Vatsalya.

| Did you know that you can secure your child’s retirement with NPS Vatsalya? Read about it here. |

Discovering NPS and Its Benefits

The seminar’s financial expert explained that NPS is a government-backed voluntary retirement savings scheme designed to provide financial security post-retirement. She highlighted key features that caught Ajit and Kiran’s attention.

The following are the key or major features of NPS investing:

- Flexible Investments: They could choose between active and auto choice investment strategies, allocating funds across equity, corporate bonds, and government securities.

- Low-Cost Structure: Compared to mutual funds and insurance products, NPS had a lower fund management charge, ensuring higher savings.

- Tax Benefits: Contributions made to NPS were eligible for deductions under the Income Tax Act, which would reduce their tax liability.

- Portability: Even if they changed jobs or moved to a different city, their NPS account would remain unchanged.

- Systematic Withdrawal Post-Retirement: Upon turning 60, a portion of their corpus could be withdrawn as a lump sum, while the remainder would be used to provide a regular pension.

| Can NPS Vatsalya be better than PPF or mutual funds? Find out here. |

Introducing NPS Vatsalya – Planning for Nihaal’s Future

The couple was intrigued when they learnt about NPS Vatsalya, a scheme introduced in Budget 2024 aimed at securing financial stability for minors. The expert explained that parents could open an NPS account in their child’s name, allowing investments to grow with the power of compounding. Upon turning 18, the NPS Vatsalya account would seamlessly transition into a regular NPS account, ensuring continued financial discipline.

Key benefits of NPS Vatsalya:

- Start Early, Gain More: Investments made in childhood benefit from long-term compounding.

- Flexible Contributions: Parents could invest as little as ₹1,000 annually, with no upper limit.

- Tax-Free Growth: Contributions and withdrawals at maturity were largely tax-efficient.

- Partial Withdrawals for Education & Medical Needs: Some funds could be withdrawn before 18 for essential purposes.

| Before you subscribe for NPS, you can ensure that you have a PAN. For the application of e-PAN, follow these steps. If you wish to surrender a duplicate PAN, you may refer to this. |

Old Tax Regime vs. New Tax Regime – A Dilemma for Ajit and Kiran

Excited about the benefits, Ajit and Kiran decided to invest in NPS for themselves and Nihaal, but they faced a critical decision—whether to opt for the Old Tax Regime or the New Tax Regime while filing their taxes.

| Check this link for individual and corporate application for NPS. Start investing now! |

Old Tax Regime – More Deductions, More Savings?

Under the old tax regime, NPS contributions qualified for multiple deductions:

- Section 80CCD(1): Ajit could claim up to ₹1.5 lakh as part of the overall Section 80C limit for his contributions.

- Section 80CCD(1B): An additional ₹50,000 deduction was available for self-contributions beyond the 80C limit.

- Section 80CCD(2): If Ajit’s employer contributed up to 10% of his salary (14% for government employees) to his NPS account, it wouldn’t count towards the ₹1.5 lakh limit and would be fully deductible.

If Ajit opts to the Old Tax Regime, he could claim tax deductions of up to ₹2 lakh on his NPS contributions. However, he would have to forgo the lower tax slabs available under the New Tax Regime.

| Finding the NPS Vatsalya Scheme promising? Learn more about NPS Vatsalya benefits here. |

New Tax Regime – Simplicity Over Deductions?

The New Tax Regime (introduced in Budget 2020) offered lower tax slabs but no deductions under Sections 80C, 80D, and 80CCD (except for 80CCD(2), where employer’s contribution to NPS is higher i.e. 14% than 10% being offered under the old tax regime).

If Ajit and Kiran opted for the new regime, they would lose the ₹2 lakh NPS tax deduction but pay lower tax rates overall. The expert advised them to calculate their total tax outgo under both regimes before deciding.

| Parents of thousands of minors in India have made their choice to secure their child’s future with NPS Vatsalys. Why delay? Start now! |

Ajit and Kiran's Decision

After crunching numbers, Ajit realised that:

- In the Old Tax Regime, his total tax deductions (including NPS) helped reduce taxable income significantly.

- In the New Tax Regime, his tax slabs were lower but he missed out on key deductions.

Since Ajit was a salaried employee and his NPS contributions were significant, he chose to stay in the Old Tax Regime to maximise tax benefits. Kiran, who had a business, opted for the New Tax Regime as she didn’t claim many deductions and preferred simpler tax compliance.

| Invest in NPS Vatsalya now! Check this step-by-step guide to get started with investing in NPS Vatsalya. NPS Vatsalya application steps and link here! |

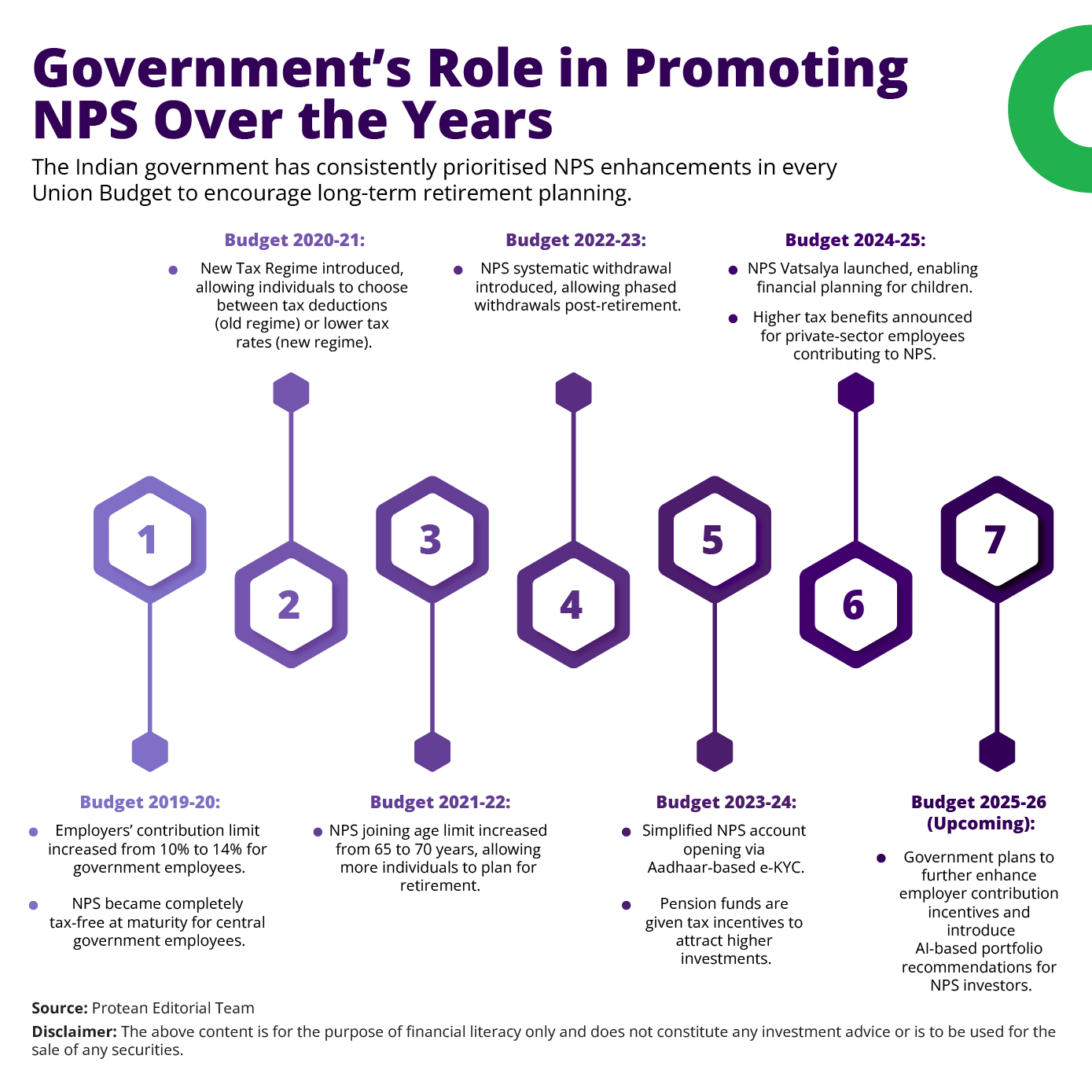

Recently, the Union Budget 2025-26 has introduced a notable change concerning the National Pension System (NPS). The tax exemption under Section 80CCD(1B), which allows for an additional deduction of ₹50,000 for NPS contributions, has been extended to include the NPS Vatsalya scheme. This extension enables parents or guardians to claim this deduction under the old tax regime when contributing to NPS accounts for their children.

This move is anticipated to encourage greater participation in the NPS, promoting long-term savings for children's future financial security.

The year 2024 was a milestone year for NPS. Learn about all that happened in NPS in 2024 here.

Conclusion

By investing in NPS for themselves and NPS Vatsalya for Nihaal, Ajit and Kiran ensured a financially secure future for their family. With tax benefits under the Old Regime and the flexibility of NPS, they made informed choices aligned with their financial goals.

This story highlights how NPS remains a powerful tool for retirement planning and how the Indian government continues to strengthen it to encourage long-term savings. Whether opting for NPS under the Old or New Tax Regime, the key takeaway is that starting early and staying committed to retirement savings can lead to a stress-free financial future.

Don’t wait longer! Start investing with NPS now! NPS registration and document details for individuals and corporates here.

- Story by Bruhadeeswaran R.

Bruhadeeswaran has 15+ years of experience as a content strategist, communication, and editorial professional. Currently, he is leading an innovative content development process, translating complex B2B products into engaging, user-friendly narratives.